When it comes to the HDB BTO application, being a first-timer applicant gives you a lot of benefits. Not only can you qualify for a higher grant amount, but you get more priority too (read: better chance of securing a queue number).

First-timer applicant benefits for HDB BTO

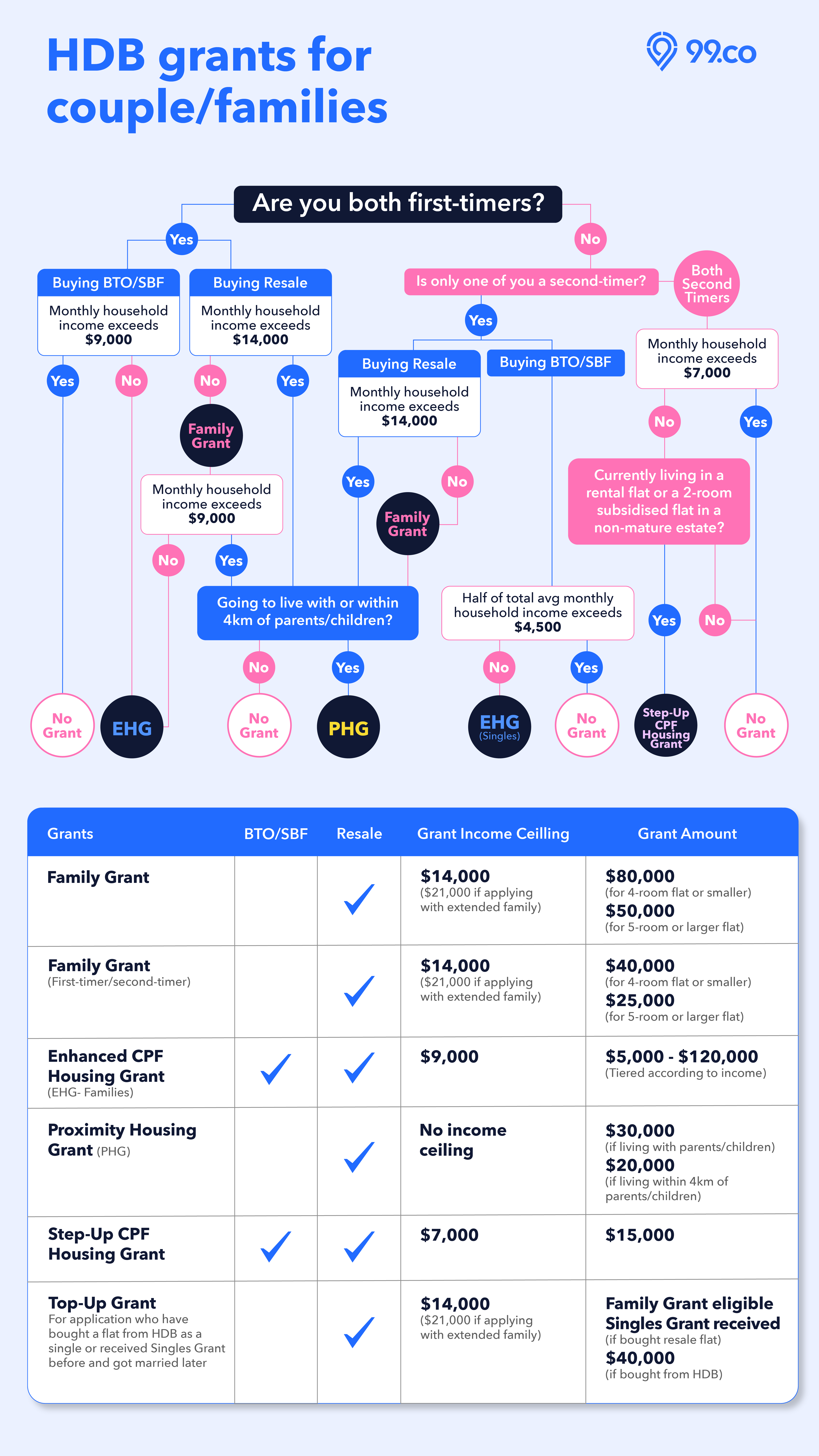

Enhanced CPF Housing Grant of up to S$120k

As a first-timer, you can qualify for the Enhanced CPF Housing Grant (EHG) of up to S$120,000. How much you can get depends on your income.

To qualify, your average gross monthly household income for 12 months must not exceed the income ceiling of S$9,000.

First-timer applicant priority

As a first-timer, you also get more priority compared to second-timers and singles, which means you have a better chance of securing a queue number. These include:

- Higher flat allocation

- Two ballot chances (compared to one for second-timers and singles)

- Additional ballot chances if you were unsuccessful in previous attempts to ballot in non-mature estates

(Plus, from the August 2023 BTO exercise onwards, there will be a new priority category called First-Timers (Parents and Married Couples) or FT (PMC). They are

- families with children aged 18 and below, or

- married couples aged 40 and below

who have never owned or sold a residential property before and did not book a BTO or SBF flat in the last five years before their flat application.

These applications will get three ballot chances.)

Here’s the BTO flat distribution if you are applying for a flat in a non-mature estate:

| Flat type | First-timer | Second-timer | |||||

| Families (PPS) | Families (MCPS) | Other families | Singles | Families (ASSIST) | Families (MCPS) | Other families | |

| 2-room Flexi | 5% | 5% | 10% | 65% | 5% | 5% | 5% |

| 3-room | 30% | 30% | 25% | – | 5% | 5% | 5% |

| 4- and 5-room | 30% | 30% | 35% | – | – | 3% | 2% |

PPS = Parenthood Priority Scheme, MCPS = Married Child Priority Scheme, ASSIST = Assistance Scheme for Second-Timers. For more info, check out our article on HDB’s different schemes.

And here’s the BTO flat distribution if you are applying for a flat in a mature estate:

| Flat type | First-timer | Second-timer | |||

| 2-room Flexi to 5-room | Families (PPS) | Families (MCPS) | Other families | Families (MCPS) | Other families |

| 30% | 30% | 35% | 3% | 2% |

There are also more flats set aside for first-timers applying for flats with a shorter waiting time:

| Flat type | First-timer | Second-timer | |||

| Families (PPS) | Families (MCPS) | Other families | Families (MCPS) | Other families | |

| 4-room and bigger flats | 30% | 30% | 35% | 3% | 2% |

(Starting from the August 2023 BTO exercise, the PPS will be expanded and renamed Family and Parenthood Priority Scheme (FPPS). Under this scheme, up to 40% of the BTO flats and 60% of the SBF flats will be set aside for FT (PMC). They will also get priority when they apply for a 4-room or smaller flat in a non-mature estate.)

You can also get additional ballot chances when applying in a non-mature estate, after two failed applications in non-mature estates.

| No. of previous failed applications | Additional chances (+1 per application after 2 failed applications) | Total (additional chance + 2 first-timer chances) |

| 0 to 1 | 0 | 2 |

| 2 | 1 | 3 |

| 3 | 2 | 4 |

| 4 | 3 | 5 |

Deferred Income Assessment

As a young couple (with at least one of you a first-timer), you can apply first and defer the income assessment for the grant and HDB housing loan. Your income will only be assessed around three months before the flat completion.

The eligibility criteria is that both of you must also be full-time students or NSF, and/or have completed studies or NS within 12 months before applying for a flat.

Staggered Down Payment Scheme

First-timers are also eligible for the Staggered Down Payment Scheme if you are applying as a married couple or applying under the Fiance/Fiancee Scheme. Through the scheme, instead of paying the down payment during the signing of the Agreement for Lease, you can pay it in two instalments: during the agreement signing and key collection.

So if you are taking an HDB loan, the remaining down payment to be paid during key collection will be 25%. This is because of the change in loan-to-value (LTV) ratio limit for HDB loans, which has since decreased from 80% to 75%, as announced in the National Day Rally in August 2024.

So who is considered a first-timer HDB BTO applicant?

You are considered a first-timer applicant if you have received none housing subsidies before. This means you have never bought:

- A flat directly from the HDB

- A resale flat with CPF housing grant

- A DBSS flat from a developer

- An EC from a developer

- Or enjoyed other forms of housing subsidy, e.g. Selective En bloc Redevelopment Scheme (SERS), privatisation of HUDC estate, etc.

So you are considered a second-timer if you have bought any of these. From 9 May 2023 onwards, if you are listed as an essential occupier and received the housing grant, you will also be considered a second-timer for your next HDB flat purchase. As a second-timer, pay the resale levy when you buy a flat from HDB.

(While HDB regards couples comprising a first-timer and a second-timer as a first-timer family, take note that there are schemes, such as the Parenthood Priority Scheme that require both applicants to be first-timers.)

With that, we break down a few situations that disqualify you from enjoying first-timer applicant benefits.

Why you may not enjoy first-timer applicant benefits for HDB BTO

1. You have bought a subsidised flat with a family member before

For instance, you have bought a flat directly from HDB or a resale flat using a CPF grant with your parents under the Public Scheme or with your siblings under the Orphans Scheme. You may have bought it with a family member to pay the mortgage.

Doing so also means you will lose your first-timer applicant status when you buy a flat later on with your spouse (or on your own as a single when you turn 35). So you will be considered a second-timer when you buy a BTO flat.

Also, deal with the admin issue of removing your name from the flat and having the other family members buy your share. This is because you cannot own more than one HDB flat at a time.

And that is why we do not recommend people to buy a flat together with a family member.

Additionally, essential occupiers will now be considered second-timers the next time they buy an HDB flat. The only exception to this rule is parent-child households, whereby the child is listed as an essential occupier.

2. Your parents have transferred the ownership of a subsidised flat to you

This includes inheriting the flat.

We are not saying this is a bad thing since it means you already have a home to your name. And if it is fully paid up already, you will just need to pay the legal fees and other costs like property tax and conservancy fees.

But if you are planning to get a BTO flat, owning a subsidised flat can disrupt your plans. First, there is the five-year MOP that you have to fulfil after taking over the flat. This should also satisfy the five-year time bar before you can apply to buy another subsidised flat.

On top of that, since you are planning to buy another subsidised flat, pay the resale levy and be considered a second-timer.

And since you can only own one HDB flat at a time, you will also have to dispose of this inherited flat within six months of completing the flat purchase.

3. You have rejected a chance to select a flat twice

There are various reasons you may have rejected an invitation to book a flat. This can be because the flats left for selection are not desirable, or you may have financial difficulties.

But if you have been invited to book a flat twice and rejected both chances, you will have your first-timer priority suspended for a year. So during this one-year period, you can still apply for a BTO flat, but you will be balloted together with the second-timers. This means having a lower chance of securing a queue number because of the lower flat allocation for second-timers.

And if you still decide not to book a flat when invited twice, you will have the first-timer priority suspended for another year. So you will have to wait one more year before you will be considered a first-timer and enjoy the first-timer priority again.

If you look at the flat allocation and application rates for second-timers, you will know how hard it is to get a queue number as a second-timer.

4. You have cancelled your BTO application after booking a flat

The penalty is more severe than cancelling your application before the flat booking.

Suppose you cancel your BTO application before the key collection. In that case, the next time you apply for a BTO flat, you will not get any additional ballot chances that would have been accumulated from the previous unsuccessful applications in the non-mature estates.

Besides this first-timer benefit, you will also have to wait for one year before you can apply or be an essential occupier for:

- A new flat

- A resale flat bought with a CPF housing grant

- A DBSS flat from a developer

- An EC bought from a developer

- A resale flat that is been chosen for SERS

Plus, forfeit the option fee if you have paid for it (before signing the lease) and 5% of the purchase price (after signing the lease).

5. You broke up after the key collection

Unfortunately, sometimes things happen. One of the most common cases we hear is couples breaking up after the BTO key collection.

In such a case, since you have applied as a couple, should you break up later after getting your flat, give the flat back to HDB. HDB will then compensate you at the prevailing compensation price.

(If you have listed either of your parents in the application instead, HDB will allow you to keep the flat.)

On top of that, there is a penalty. You will likely be barred from applying for a new flat for several years.

Do you know any other reasons that can disqualify you from enjoying first-timer HDB BTO applicant benefits? Let us know in the comments section below.

If you found this article helpful, 99.co recommends HFE (HDB Flat Eligibility) letter: What is it and how to apply and Sale of Balance Flats 2023, What you need to know about HDB’s Sale of Balance Flats (SBF) in 2023.

About Ananda Bayu

Ananda has been wrangling Singapore's complex real estate trends into readable bites since 2020. She writes like she's explaining it to a friend over kopi — because who has time for jargon? When off the clock, she’s probably doom-scrolling through cat memes on X, convincing herself it's the highest tier of "creative inspiration".

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

If i married a divorcee who har a BTO with the EX wife. The flat was sold 18 years ago. If i apply BTO withbhim, is it considered first timer?

Hi Shermein, yes, HDB will still consider you and your partner as a first-timer family and can enjoy first-timer priority, even though your partner is actually a second-timer. https://www.hdb.gov.sg/cs/infoweb/residential/buying-a-flat/buying-procedure-for-new-flats/application/priority-schemes?anchor=privileges

We bought a resale flat before granting citizenship. We want to apply for BTO. Are we considered first timer?

Hi Wallace, yes you’ll be considered first timers since you previously didn’t receive subsidy in the form of grants.

Hi, my parent in law transferred ownership to me & my husband dated 2007. The HDB was fully paid. We wanted to sell the current flat and apply bro or resale flat. Can we consider 1st time applicants to enjoy HDB subsidies?

Hi Joyce, this depends on whether the current flat was subsidised (bought directly from HDB or bought from the open market with resale grants).

Hi 99co,

I currently have a flat with my parent, but I’ll be applying for a new bto with my wife who is a first timer, while transferring/removing my name from the flat, are we still considered a first-timer family?

Hi Aaron, this depends on the flat you have with your parent, if it is bought directly from HDB or bought with resale grants if it’s bought from the open market.

It was acquired as part of enbloc back then.

In that case, you’re considered to have enjoyed housing subsidy before. Hence, you’ll be considered be considered a second-timer. At the same time, since you’re applying with your wife who’s a first-timer, you’ll be considered as a first-timer family. https://www.hdb.gov.sg/cs/infoweb/residential/buying-a-flat/buying-procedure-for-new-flats/application/priority-schemes?anchor=privileges

If forfeit my ballot queue ticket for an EC will it affect my chances of getting a BTO as a first timer?

Hi Branden, no it doesn’t seem like that will affect your chances of getting a BTO queue number.

I bought an EC directly from developer but I never get any grant. Do I consider first or second timer?

Hi Elaine, if you bought an EC directly from a developer but you never applied for any grants, you will be considered a first-timer.

You will be considered a 2nd-timer if you have bought a flat from HDB before, took a CPF Housing Grant to purchase public housing (such as DBSS, resale HDB, EC), enjoyed other subsidies (eg. SERS), or transferred a HDB flat bought directly from HDB or a HDB resale flat bought with a CPF Housing Grant before.

Hi 99co,

I have booked a BTO unit with my wife , is it possible for my parents to transfer their current HDB ownership to me months before key collection so that I can sell and pay the HDB loans for the BTO unit

Hi Gin,

As you already have booked a BTO unit with you wife, you need to first serve the mandatory MOP (5 years or 10 years if it’s PLH) before you can sell your unit and own another HDB flat. In this case, your parents cannot transfer their current HDB to you as that would mean you will own both a BTO unit (which isn’t ready yet but is already booked) and a resale HDB flat.