As the world continues to reel from the economic effects of Covid-19, the Singapore Ministry of Trade and Industry (MTI) on 26 May downgraded the official outlook for the country’s Gross Domestic Product (GDP) in 2020 yet again (from -1 to -4% to -4 to 7%), signalling the deepest recession the country has ever faced since independence.

On 14 July, the MTI announced that, based on advance estimates, the economy contracted 12.6% year-on-year in Q2 2020. On a quarter-on-quarter seasonally-adjusted annualised basis, the figure translates to a 41.2% in GDP.

The GDP is the total value of goods and services produced by a country’s economy during a specified period of time (i.e. one calendar year). A negative GDP figure indicates an economic recession.

To put things in context, Singapore has never had it’s GDP shrink by more than -3.1% in the span of a year. That was way back in 1964.

The last time Singapore recorded a full-year contraction was during the dot-com bust in 2001, when growth fell by 1.1%. The country’s worst post-independence recession occured during the Asian financial crisis in 1997-98, when GDP fell by 2.2%.

Asia will also experience zero economic growth in 2020, according to the International Monetary Fund. This will be the continent’s worst GDP performance in 60 years.

How will a -7% GDP contraction affect the property market?

The bad news is that the Covid-19 recession could cause lasting damage to our economy. The good news is that the Singapore government appears determined not to let that happen.

On the same day that the Ministry of Trade and Industry (MTI) issued the revised GDP outlook, the Singapore government took another step to protect jobs and shore up the economy with the $33 billion Fortitude Budget—the fourth budget of 2020.

In total, the government will draw on past reserves and spend an unprecedented $92.9 billion dollars on the economy, amounting to nearly 20% of a year’s GDP.

In addition, a couple of policy measures, which we’ll talk about in a later part of this article, could also help dampen the impact of a GDP contraction on the Singapore property market.

At the announcement of the supplementary budget, Deputy Prime Minister Heng Swee Keat warned that Singapore “must be prepared for tough times ahead”, and that it may take up to 18 months for a Covid-19 vaccine to materialise.

In the meantime, the country will have to adjust to a new normal.

But how will the Singapore property market fare amid an unprecented recession? Let’s start with the basics:

I’m a property buyer. What will a deep recession mean for me?

The good news first. In the current situation, buyers who are in very secure jobs (e.g. civil service, healthcare) are actually in relatively better position because the overall market is showing some signs of weakness. Buyers also get to enjoy bargain basement home loan interest rates right now.

[Recommended article: How to Hunt for Fire Sale Properties in a Recession (other than auctions)]

Simple economics state that lower demand means lower prices, given that supply doesn’t also decrease. Covid-19 will certainly take out a group of buyers: those adopting a wait-and-see approach or who are simply unable to buy due to reduced income. The lack of competing buyers will put you in pole position to negotiate, even when it comes to units and developments with superior attributes.

Don’t wait too long, however, if you’ve already shortlisted some potential properties. Take newly launched condos as an example, collectively there’s definitely a supply glut, but there are still a finite number of choice units that will be quickly taken up by opportunistic buyers in a similar position as you.

If you’re somewhat impacted (e.g. income slightly reduced) but still need a home, consider reducing your budget proportionately and keep the following tips in mind:

- Consider keeping the cost of the home to five times (5x) the combined annual household income (e.g. you and your spouse)

- For the above, use a conservative version of your income (i.e your pay before your latest promotion) to calculate

- Avoid maxing out your Total Debt Servicing Ratio (TDSR), which could be the case if you are also servicing a car loan

- Make sure you have six months worth of emergency savings after making the downpayment

In any case, always seek a financial consultant’s advice before committing to the option fee/downpayment for a new home, and a property agent’s advice for more affordable options that still fit your needs and preferences. 99.co’s comprehensive search filters will also help.

I’m a property seller. What will a deep recession mean for me?

Honestly, even if in-person viewings resume, you’re going to find that it takes longer to sell a property. The typical three months to find a buyer will likely turn into six months, for instance.

So, factor the extended timeline into consideration and set realistic asking prices, even if you have holding power. For example, if you have an offer that’s 5% lower than your intended price but still nets you a profit, consider accepting it rather than holding out for a better offer, which may not materialise since there’s a good chance the market might soften further in the next few quarters.

If you’re facing temporary financial constraints, you may also want to considering deferring your mortgage, or renting out part of your property (i.e. the master bedroom), instead of selling and downgrading. Speak to your financial advisor to explore the feasibility of each option.

Do be very careful when selling your property, to avoid making a negative sale that could further worsen your financial situation.

I’m a property investor. What will a deep recession mean for me?

If you’re dependant on rental yields, you’ll need to tread carefully. Considering that the government’s supplementary budgets benefit mostly Singaporeans, it’s likely that we’re going to see a fair number of expats with pay cuts during this recession, with some even getting retrenched. Rental demand, especially for more expensive Core Central Region properties, will fall along with rents. (Expats are already asking for rent cuts, by the way.)

Comparatively, properties outside of the city may start to look more attractive to the property investor, as do leasehold developments with a low entry price. The recession may also prompt some HDB owners to upgrade, moving to a low-priced condo while unlocking the rental potential of their existing HDB flats (especially if the flats are in a highly rentable location).

Perhaps more than at any point in time, it’s looking more attractive to own and rent out properties to workers in essential industries and sectors, rather than office-bound expats, and these are homes that are typically further out from the CBD and near to catchment areas such as major industrial estates, hospitals and universities.

But that’s not to say that it’s game over for prime district homes. In April, we saw a Chinese billionaire splash $28 million on a penthouse near Orchard. The volume of such high-value purchases are going to fall in a recession, but they’ll still happen as long as these homes continue to be viewed as safe haven assets among “buy-and-hold” investors.

[Recommended article: Will rent go down in a recession?]

Just how much will property prices fall?

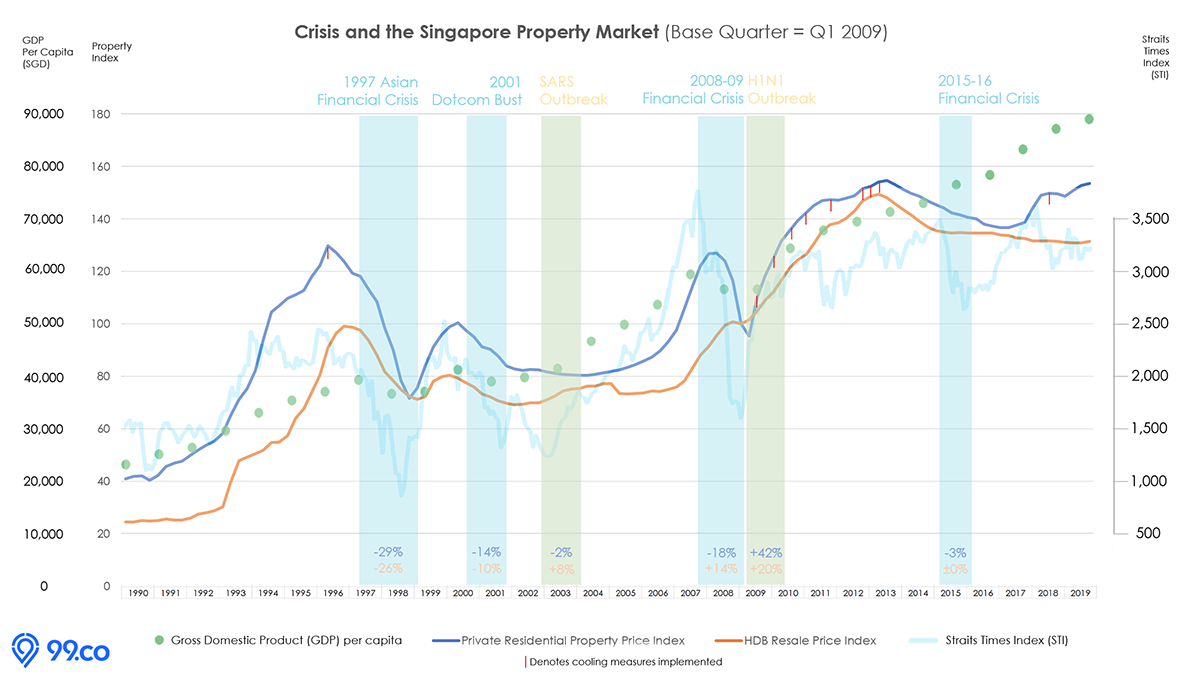

To get an idea of just how much property prices might fall in this recession, let’s look at this chart:

From the 30-year chart above, we can see that the indicator that correlates the most with falling private property prices is the Gross Domestic Product (GDP) per capita, which is essentially GDP divided by the population of an economy.

HDB resale prices, on the other hand, do not seem to have a clear correlation with any particular indicator. However, it’s noteworthy that in the worst crisis the chart illustrates (the 1997-98 Asian Financial Crisis), HDB and private home prices plunged in tandem.

In a recession, the GDP per capita typically falls by more than the GDP. That’s because the population of an economy/country tends to increase year-on-year, resulting in a lower GDP per capita in a situation where GDP is unchanged (i.e. 0% change).

And the chart shows that, whenever GDP per capita fell, prices of private property in Singapore fell as well.

In the past 30 years, there were three dips in GDP per capita: in 1998, 2001 and 2008-2009. In all three instances, the URA Private Residential Price Index fell. The Index (i.e. private home prices) fell a staggering -29% during the 1997-98 Asian Financial Crisis.

In the dot-com bust of 2001, private home prices fell by 14%. During the 2008-09 Global Financial Crisis, private home prices fell by 18%.

With GDP per capita again expected to drop this year with the GDP, will we again see a double-digit drop in private home prices?

Yes and no. Yes because that’s what history has told us will happen, but no because of the following three reasons:

Firstly, successive cooling measures over the years have prevented the private property market from runaway price growth, so the magnitude of any fall will likely be lower than 1997-98, 2001 and 2008-09.

Secondly, the crisis of 1997-98 and 2008-09 were crises driven largely by real estate bubbles, whereas the current crisis is driven by a pandemic. Property watchers will take comfort in knowing that both private and HDB property prices performed robustly during the SARS and H1N1 outbreak, as the chart above shows. (Then again, none of these outbreaks had led to a full-blown global recession.)

Thirdly, the Singapore government has introduced a slew of policies and legislation that appears specifically intended to avert a plunge in property prices (in addition to wider policies that benefit households and secure jobs):

- Allowing homeowners to defer their home loan repayments for the full year

- Protecting deposits paid by property buyers to developers

- Extending the ABSD remission timeline from six to twelve months, benefitting both homebuyers and developers

If deemed necessary, we believe that the government will come up with further interventions to cushion the fall of property prices during this seriously-deep recession.

So, here’s our take on the effect of a -4 to -7% recession on the property market in Singapore:

- Private property market: Following a 1.2% price fall in Q1 2020, a further 5 to 11% decrease in home prices in 2020. High-end, luxury residential properties will likely experience greater downward price pressure.

- HDB resale market: A fall, but by a lower magnitude compared to the private property market. (HDB prices were unchanged in the first quarter of 2020.)

What’s your take on the recession’s impact on Singapore’s property market? Let us know in the comments below!

If you found this article helpful, 99.co recommends Is pent-up demand for property a myth? and 5 real estate scams that could run rampant during Covid-19

Looking for a property? Find your dream

About Kyle Leung

Content Marketing Manager @ 99.co

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Hi, I would like to know if EC that has yet to fulfill MOP, does the price follow the trend of private condo or HDB?

Hi Daniel, great question. I assume you’re referring to ECs between 5 to 10 years of age. We did a quick check on our data and found that the price trend for ECs of this age loosely correlates to the price movements of private condos. This is expected, as resale EC buyers are not eligible for any grants.

The Covid 19 pandemic has caused the worst global economic crisis since the Great Depression of a hundred years ago. It is not comparable to any past financial crisis or pandemic that has happened in our living memory. Since countries are so intertwined and interdependent globally, the effect of this current pandemic is bigger than anything we have experienced before.

The effect on the local property market will be the worst that we have ever seen. I predict that despite all the measures the government has put in to stabilize it, property prices will decline more than 30% over the next 2-3 years

This is a really well balanced analysis! Great work!

Do you think fully furnished options will fare better than partially furnished condos, outside the CBD in particular Serangoon area?