Here’s a bombshell for anyone who might be selling their property: Even if you sell for a profit, under certain circumstances you could still end up with a loss or even land yourself in debt instantly. When you owe money after selling your property, you’ve made what’s called a negative sale.

That’s a scary situation to find yourself in, so you need to know what could cause a negative sale. In a recession (like right now), we’re likely to see more cases of negative sales happening, since some sellers may lower their prices (e.g. to below market value) to find a buyer.

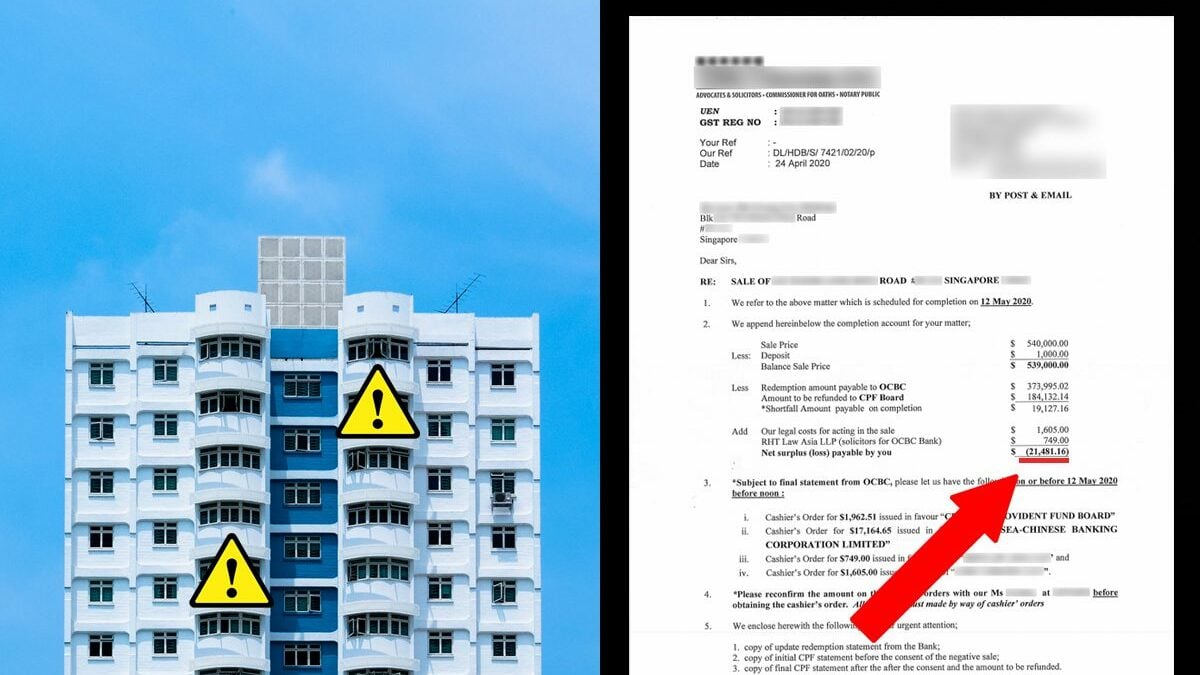

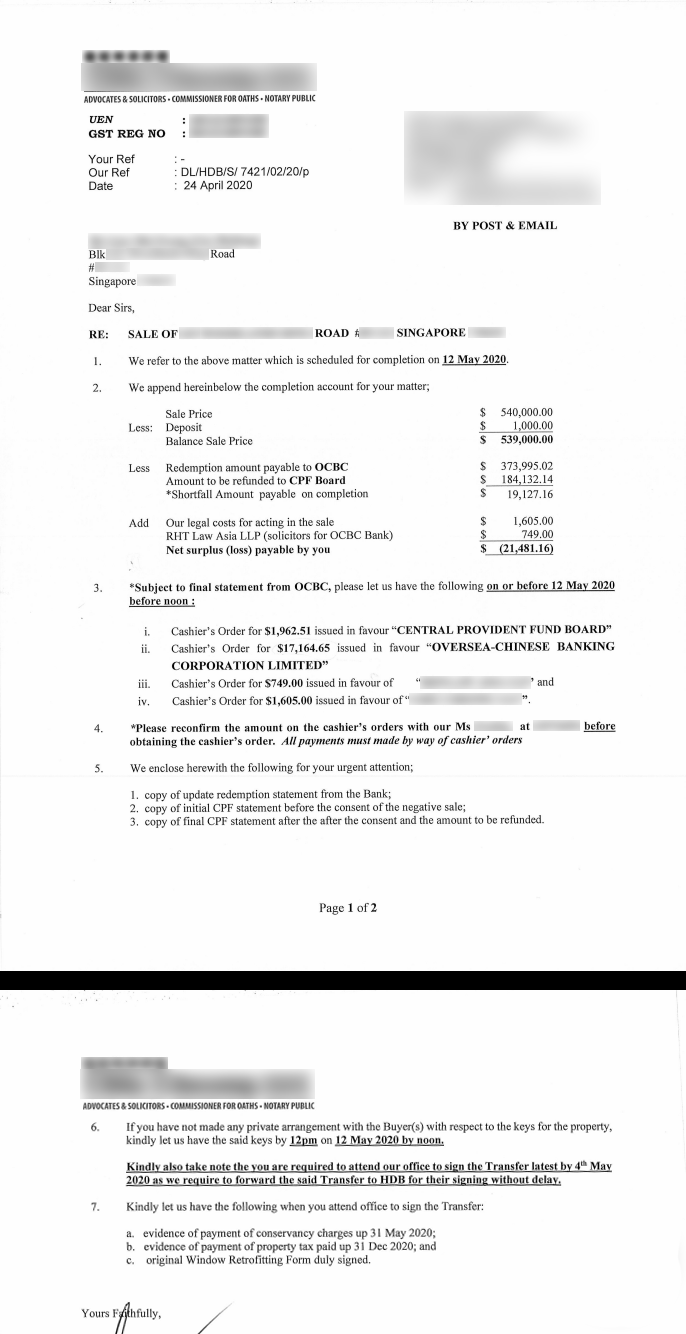

Imagine that a seller urgently needs the cash and thinks he/she has managed to sell at a profit, but then get a rude shock when the conveyancing lawyer comes back with a list of debtors (e.g. the bank) that must be repaid by completion date of the sale, failing which he/she could be sued by the buyer for not being able to handover.

It gets even worse if the seller had already committed to another property purchase and has to forfeit deposits and/or downpayment paid.

How do you avoid falling into this dark abyss?

First, you’ll have to understand the different ways you can end up with a negative sale:

- Outstanding loan amount after interest

- Sellers Stamp Duty and other fees

- Having to pay accrued interest back into your CPF account (though you can use this amount for your next home purchase, subject to certain terms and conditions)

- You’re in arrears to the same bank

1. Outstanding home loan amount after interest

Your home loan isn’t free—it’s subject to compounding interest. The interest is computed at the start of your mortgage and, together with the principal (i.e. the amount that actually pays off your property), forms the total outstanding amount you need to pay over the course of your tenure.

If your sale price can’t beat the amount still outstanding at the time of your sale, then boom, you’ve made a negative sale.

Here’s an example: You borrow $1 million for your property. The loan interest is 2% per annum with a 30 year tenure. Factoring the interest, the total amount you need to pay back is roughly $1.33 million. A total of $330,000+ consists of interest payments alone.

After four years, you decide to sell the property. Your outstanding loan amount will be $898,668.

If you sell your property at anything below that amount, you’ve made a negative sale and will owe the bank the difference between the outstanding and sale amount. (And that’s not counting any early repayment penalty fees you might have to incur.)

If you’re not sure of the numbers, consult your bank before you set a sale price. At the very least, your sales proceeds should at least pay off the entire mortgage with the interest.

This is why it’s important to keep home loan interest rates as low as possible, and refinance when the rates climb too high. Private bank loans fluctuate all the time, from as low as 1.3% (at the time of writing) to as high as 3%; although the average is about 1.8%.

For HDB loans, the interest rate is always 0.1% above the prevailing CPF rate. It has been set at 2.6% for nearly two decades and counting; and seldom changes.

2. Seller’s Stamp Duty (SSD) and other fees

If you sell a property within three years of buying it, you will incur the Seller’s Stamp Duty (SSD). This is a percentage of the sales proceeds that will incur SSD:

- 12% if sold within the first year of purchase

- 8% on the second year of purchase

- 4% on the third year of purchase

Having to pay the SSD, plus the home loan interest and other fees can result in a negative sale, especially for a seller who has little choice but to sell soon after he/she bought the property.

Furthermore, it’s highly unlikely for any property to appreciate so fast in three years that you can still see profits after paying the SSD. (Since 2005, the annualised return on most condo properties in Singapore is about 3.44%, excluding rental gains).

The SSD is still payable in the event of an en-bloc sale (so it’s sometimes out of your control). But you can at least appeal to the Strata Titles Board (STB) if the SSD would cause you a financial loss in the case of a collective sale.

Besides the SSD and outstanding home loan amount, again bear in mind other fees such as:

- Prepayment penalties from the bank (if this clause applies, you need to pay 1.5% of the amount you’re prepaying to end the home loan early)

- Agent service fees (most property agents take 2% of the transaction amount as their commission or fee)

- Conveyancing and processing fees (varies)

The total impact of all the smaller fees, coupled with interest rates or SSD, can result in a painful negative sale.

3. Having to pay accrued interest back into your CPF account

When you sell your property, not only must the funds you used from your CPF Ordinary Account (CPF-OA) be returned to it, you’ll still need to pay 2.5% accrued interest. The interest kicks in once you use that sum of money. For example, a housing grant of $50,000 given to purchase a HDB flat will be $56,570 you have to put back to your CPF-OA five years later. That interest called the accrued interest, which is the interest amount that you would have earned if your CPF savings had not been withdrawn for housing. (We’ve covered accrued interest in detail in this article.)

Why does this happen? According to the CPF Board, paying back accrued interest ensures you have sufficient funds for retirement.

The good news is, if you sell your property at or above market value, you only have to pay back accrued interest in the case of positive cash proceeds. Once your cash proceeds hits zero, you’re exempt from actually topping up your CPF OA for the money for accrued interest.

However, sellers who have little choice but to sell below market value, or belatedly find out that their sale price is below market value, will have to pay back in full what is owed to CPF plus accrued interest. Sellers may even have to pay out of their own pocket, because they have no cash proceeds from their sale.

If you find that you’re in the latter situation, you may write in to the CPF Board to request for a waiver. According to the CPF Board, such requests will be assessed on a case-by-case basis.

Again, it’s important to plan ahead. You can find out the amount you owe to CPF plus accrued interest at any point in time, by logging onto your CPF account via the organisation’s website.

4. You’re in arrears to the same bank

If you have other loans to the same bank holding your mortgage, then the bank really can grab at the proceeds to cover your other debts. Most banks we called didn’t want to get into details, but we confirmed two things:

First, banks do actually have a right to take money this way (it’s often written right into the terms of the loan). If you’re in arrears and the money appears in your account with them, they can just reach out and grab it—it’s literally right there in their coffers.

Second, we were told this is only done if you’re seriously in arrears (e.g. you’ve owed the money for years and have repeated lawyer letters from them), or have a history of defaults plus outstanding debts. If you have a good history of repaying your credit card, personal loans, etc., on time, they will likely not resort to this even if you have outstanding debt.

Note that on selling a property, the money will be used to pay off any bad debts with the bank first, before the rest of it is used to repay the outstanding home loan. (Once that is settled, then you’d move on to refunds to CPF accounts.) If the seller owes the bank substantial sums, like tens of thousands of dollars in credit card debt, the bank can give the seller an ultimatum: repay all debt or we will block the sale of your property.

How do I avoid being in debt from a negative sale?

One way to avoid the potentially devastating effects of a negative sale is to service as much of your loan in cash as you’re financially comfortable with, instead of CPF funds. For example, some homebuyers use their CPF monies only for the downpayment of the property, but pay the loan in cash. This way, they only pay back the downpayment with accrued interest when they sell their property.

Some buyers also avoid using CPF grants, as they want to minimise the amount they need to pay back.

In addition, homeowners should keep a close eye on the interest rates they pay (something that happens by default if you pay in cash instead of CPF funds; when you need to fork out money every month or quarter, there’s no way you’ll forget how much you’re paying!) It’s also important to refinance when appropriate, or reprice your loan with the same bank. Always compare to find the cheapest loans.

For HDB flat owners in particular, lower interest rates are why some choose bank loans over HDB loans. The danger is that bank loans come with early repayment penalties (a HDB loan doesn’t) and banks may pursue a court order against you (to force you to sell your home) if you are unable to service your mortgage, or are in serious arrears with the same bank.

HDB, on the other hand, allows some leeway in late payment of home loan installments and are far less likely to foreclose your property and leave you without a home.

Finally, keep your debts under control. If you must have credit card or personal loan debts for some reason, be wary of having a home loan with the same bank you owe all that money to.

Always do a thorough financial assessment prior to selling your home to ascertain if you might make a negative sale. A financial consultant, which may be your property agent, can assist you in this.

Are you facing the prospect of a negative sale? Voice your thoughts in our comments section below.

If you found this article helpful, 99.co recommends What does Bala’s Curve tell us about leasehold property value? and 5 ways selling your property can go horribly wrong (and how to fix it)

Looking for a property? Find the home of your dreams today on Singapore’s largest property portal 99.co! You can also access a wide range of tools to calculate your down payments and loan repayments, to make an informed purchase.

About Ryan Ong

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

I don’t understand why there is a need to pay the shortfall.

As long as you paid off the bank loan completely as first charge, whatever remaining CPF and accuser interest that you cannot pay the CPF board for the full amount, CPF will not ask you for it.

Is the law firm doing it correctly.

Hi Daniel, I think the article did point out that the owner are in arrears of others loans beside the mortgage (which you correctly pointed out as first charge ranking). Therefore, CPF board requires the member to refund whatever balance purely after the mortgage outstanding.

The shortfall, if you see from the cashiers order needed, bulks of it goes to pay off Ocbc instead of CPF board

Hi Leon, what happens if the amount owed to CPF isn’t repaid by the due date? If the monies inside our CPF account is indeed ours, shouldn’t it not matter if it’s not repaid? Can CPF board sue CPF account holders for monies which are effectively not theirs?

This creates a dilemma for home buyers on whether they should be using their CPF monies for financing. Having to repay the grants taken with accrued interest doesn’t make sense too since the grants are technically not our CPF monies, I suppose CPF explanation is that the grants are added into our CPF accounts and then used immediately to offset the purchasing price of the property?

Nevertheless, accrued interest shouldn’t be a problem if people intend to stay in their flat for life, which begs the question whether that’s the govt’s intention or to encourage sale at MOP date before accrued interest snowballs, yet it contradicted with the govt’s narrative of downsizing flat at old age or for retirement because the accrued interest incurred on older flats is potentially much higher after one has resided in his/her flat for decades.