Home loan rates in Singapore are on the rise again.

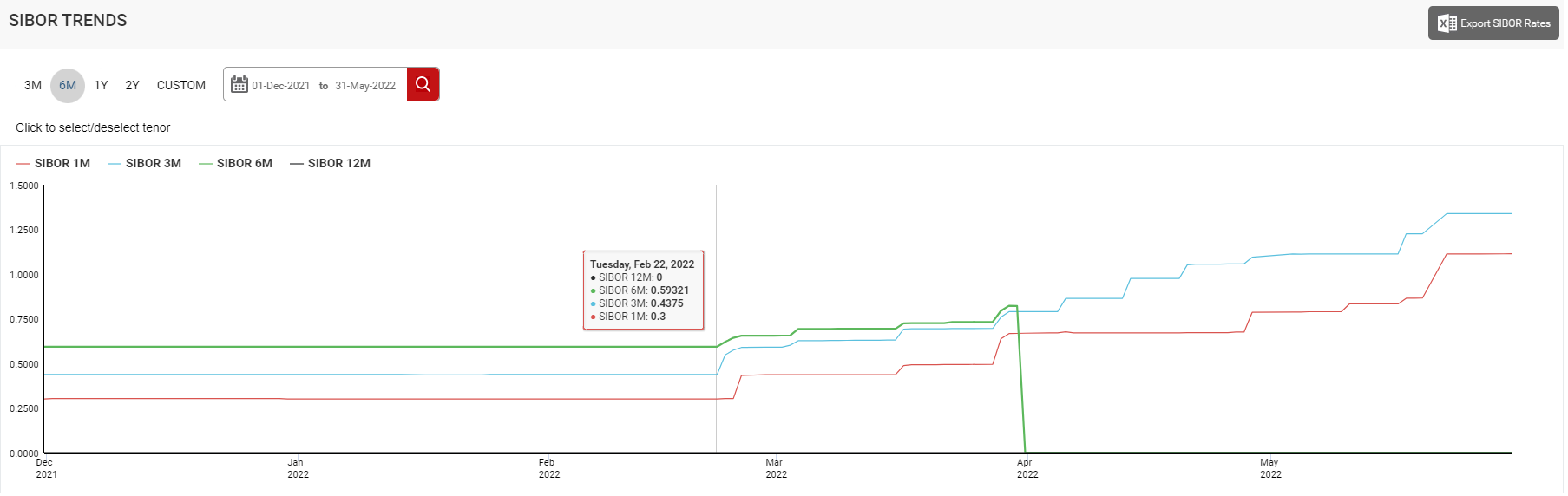

As of 30 June 2022, the three-month Singapore Interbank Offered Rate (SIBOR), to which many home loans are currently pegged to, was at 1.91%. Around four months ago, it was at 0.44%.

Similarly, the three-month Singapore Overnight Rate Average (SORA) was at 0.757% as of 30 June 2022, way higher than the 0.2% four months ago. (SORA is set to replace SIBOR and SOR.)

This has led banks here to increase their home loan rates for the past few weeks. At the same time, homeowners have been encouraged to refinance their mortgages to reduce their monthly repayments. Whether you’re a homeowner or an investor, it pays to understand how the process works.

What is mortgage refinancing?

Mortgage refinancing occurs when you switch one home loan package for another. This is often done when there are cheaper home loans available.

The process of switching your loan package is called refinancing if you are switching to a package from another bank. If you are switching to a package offered by your current bank, it is called repricing.

The main difference between refinancing and repricing is cost. Refinancing usually entails some kind of conveyancing fee to handle the legal paperwork. This is often between S$1,500 to S$3,000. Repricing will be cheaper (usually around S$800) as your loan is not transferred to another bank.

The cost of mortgage refinancing and repricing can be paid from your CPF.

Some loan packages have “free repricing options”, which means there is no cost for repricing. Speak to the bank about the terms and conditions, but remember that repricing is not the same as mortgage refinancing; you must be getting a package from the same bank for it to count as repricing.

Why would someone do mortgage refinancing?

The structure of most home loans in Singapore is similar: the interest rates will be low for the first two to three years, but rise significantly afterwards. For example, a typical home loan package might look like this:

- Year 1: three-month SORA + 0.8%

- Year 2: three-month SORA + 0.8%

- Year 3 onwards: three-month SORA + 1.0%

For example, say your current home loan package has an interest rate of 2.2% per annum. After searching around for a bit, you discover that there are home loan packages at just 1.8%. You can keep your costs lower by switching to the cheaper loan package.

Note that there’s no advantage to paying more for a home loan (there are no special features or loyalty points). As such, it makes sense to always find the cheapest current loan on the market, and many homeowners and investors seek to refinance on the third or fourth year when the rate rises.

A lower interest rate will result in lower monthly repayments

Say you purchase a condo for S$1.5 million, for which you get a loan of S$1,125,000. The loan package has an interest rate of 1.65% for the first two years, and an interest rate of 2.2% on the third year and thereafter.

Assuming the loan tenure is 25 years, your loan repayment per month for the first two years will be around S$4,579. From the third year onwards, your monthly repayment would be around S$4,879.

Now, say on the third year, you refinance into a package with a lower rate. You pay S$3,000 for the relevant fees. The interest rates on your new package are 1.4% for the first two years, and an interest rate of 1.9% for the third year onwards.

Your loan repayment per month, for the first two years, will be around S$4,447 per month. Your loan repayments from the third year onwards will be around S$4,714 per month.

In the first two years of your new package, you would save around S$132 per month. That comes to S$168 (minus S$3,000 for the fees) saved over two years. From the third year through to the end of your loan tenure, you would save around S$165 per month.

The total savings come to almost S$42,000 at the end of the loan. (Note that this is a rough estimate; the mortgage banker or broker can work out a more exact comparison for you.)

For investors, reducing the monthly instalments is important to preserve capital gains. The more interest you pay on your loan, the less profit you make upon resale. If you rent out the house, lower monthly repayments are important as you want your rental income to exceed the monthly repayment.

For homeowners, don’t be misled by the apparently small monthly savings. In the above example, the difference of around a hundred dollars a month comes to almost S$42,000 by the end of the loan. If you hoard all the savings, it’s enough to send a grandchild through university.

Switching from a floating to a fixed-rate home loan package

At present, interest rates are rising. Homeowners and investors who have a floating-rate home loan package (pegged to SIBOR or SORA) may seek to keep repayments low, by refinancing into a fixed-rate package.

Let’s say a floating-rate package has a rate of 1% + 3M SIBOR. If the SIBOR rate is 0.8%, the interest rate is 1.8% (1% + 0.8%). If the SIBOR rate rises to 1.9%, the interest rate would be 2.9% (1% + 1.9%).

A fixed-rate package is not pegged to SIBOR or SORA. If the rate is 2.5%, it will remain at 2.5% for the duration of the fixed-rate period, regardless of how the SIBOR or SORA fluctuate.

As interest rates are expected to increase further, it’s recommended that borrowers switch to fixed-rate packages to protect themselves from interest rate hikes.

Switching from HDB loans to a bank loan (only if the bank loan rate is higher)

Until recently, bank loan rates have been lower than the HDB concessionary loan rate.

The HDB concessionary loan rate has been 0.1% above the CPF Ordinary Account (OA) rate for the past two decades. The OA rate is revised quarterly, but rarely changes.

So the HDB loan rate has been at 2.6% per annum for the past 20 years. On the other hand, bank loan rates were lower at around 1.9%.

This is why some borrowers may have used an HDB loan to buy a flat at first, as HDB loans can finance up to 85% of the flat price. A bank loan can only finance up to 75%. Afterwards, they would refinance into a bank loan after purchasing their flat to get a cheaper rate and reduce their monthly instalments.

(Note: you can still use CPF to pay for the mortgage, even after you switch to a bank loan.)

But now that bank loan rates are increasing, it does not make sense to refinance from an HDB loan to a bank loan. Because once you refinance to a bank loan, you can’t switch back to an HDB loan.

Will refinancing every year save you money?

There is a cost to refinancing. At the most basic level, this is the legal cost involved. The amount typically ranges between S$2,500 to S$3,000. Before you refinance, you should check if the savings justify this expense.

For example, say you have a loan for S$1 million, on a 30 year loan tenure at 2.2%. Your monthly loan repayments would be around S$3,797.

Now, say you refinance into a cheaper loan package. The loan tenure is unchanged, and you pay an interest rate of 2%. This lowers your monthly cost to S$3,696 per month.

If you pay S$2,500 to refinancing, you would create a savings of $101 per month. It would take you more than two years just to recoup the cost of refinancing. That’s probably not worth the cost; most borrowers will only refinance if they can recoup the cost within the next six months.

Besides the legal cost of refinancing, note that some banks may also require you to cover other costs, such as the valuation fees.

Always consider the future rate of the loan you’re refinancing into

A third factor to consider is future rate of the loan you’re refinancing into. Note that most home loans are cheaper on the first three years, but jump on the fourth year. For example:

Say your current loan package is 1.8% for the first three years, and 2.2% on the fourth year or thereafter. You’re currently in the fourth year of this package.

The package you’re looking to refinance into is just 1.6% for the first three years – an attractive proposition. However, it jumps to 2.5% on the fourth year or beyond.

In this situation, you’re getting a short-term advantage from the cheaper loan. But eventually, your new loan package is going to cost more than your old one. In that case, it may make sense to keep your old loan package.

A second factor to consider is that some home loans have lock-in clauses. This imposes a penalty if you refinance within a given period (usually between one to five years). The typical penalty is 1.5% of the undisbursed loan amount – so if you still have S$600,000 left to go on your loan, for example, the penalty would be S$9,000.

In general, it is never worth breaking the lock-in to refinance; you’ll always lose money that way.

If your financial situation has changed since you obtained your home loan, you could also find it hard to refinance

Did you get your home loan a long time ago (e.g. in the 1990’s)? If so, you may run into difficulties when refinancing.

The first reason is that, a long time ago, we didn’t have restrictions such as the TDSR, or shorter loan tenures. It’s possible that you qualified for a loan many years back, but you cannot qualify for it now.

The second reason is if your finances change. For example, if you’ve become self-employed and have a variable income, or you developed bad credit, you may not qualify for a new loan. It’s a good reason to keep those credit cards paid on time!

There are some other reasons refinancing may be denied:

Some other factors may impact your refinancing:

- The remaining loan amount is too low (some banks won’t refinance if only a small amount of the loan is left, such as the last unpaid S$50,000).

- The bank doesn’t like your property for some reason (the lease is expiring, or the bank feels it would be hard to sell if foreclosed on).

- You have multiple outstanding property loans, even if you qualify for them all (some banks may feel you’re over-leveraged).

- While there’s no data exchange agreement with other countries, some banks still manage to find out if you have big defaults overseas. This can result in rejection, even if your credit score in Singapore is clean.

Who should do mortgage refinancing?

Those who should consider mortgage refinancing are:

- People in the third year of their loan package, who are not under a lock-in

- Landlords who need to keep repayments low

- Investors who are looking to sell in the short term

- Homeowners who are on a tight budget

1. People in the third year of their loan package, who are not under a lock-in

As mentioned above, interest rates rise on the third year. This is usually when you want to refinance. However, do not do so if your loan package has a lock-in clause. The clause is usually valid for two to three years, and refinancing while under the clause will incur a penalty.

A typical penalty is 1.5% of the loan quantum (e.g. For a loan of S$1,125,000, you would pay S$16,875.) Speak to a mortgage broker for advice, but as a rule of thumb, this penalty is seldom worth paying.

Note that a fixed-rate package is always locked-in. A five-year fixed-rate means a lock-in clause for all five years.

2. Landlords who need to keep repayments low

Landlords should optimise the income they get out of their property, by constantly refinancing into the lowest rates.

3. Investors who are looking to sell in the short term

If you are looking to sell the house in five to seven years, there is no need to be overly concerned with “third year and thereafter” rates. You can consider finding packages with the lowest rates for two years, and proactively refinance into a cheaper package on the third.

The less interest you pay, the higher your eventual profits will be.

4. Homeowners who are on a tight budget

If you need to tighten your belt for some reason, one of the first steps should be to reduce your debt obligations. Just as you would reduce interest repayments for your other loans (e.g. pay a high-interest credit card loan with a low-interest personal loan), you should consider lowering your mortgage repayments. This can be done by strategic refinancing.

Homeowners who are unfamiliar with refinancing can look for a mortgage broker. These brokers can handle the paperwork and refer you to the cheapest bank, and the service is often free (the bank will pay them for helping you to refinance).

[Additional reporting by Virginia Tanggono]

Would you refinance your home loan? Let us know in the comments section below.

If you found this article helpful, 99.co recommends Singapore banks revising home loan mortgage rates in line with US interest rate hike, sending letters to homeowners and Here’s why you should take a fixed rate home loan.

About Ryan Ong

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Leave a comment