As monthly condo sales in Singapore increased for the fourth consecutive month in August to a new high for 2020, many property analysts reasoned that the boom in demand was due to investors shunning stocks. They cited investor uncertainty in the post-Covid economic recovery and instability in the global stock market as reasons behind the reallocation of investment money from ‘dangerous’ equities to ‘safe havens’ such as real estate.

That’s a rather oversimplified and somewhat inaccurate generalisation of what’s going on. The most glaring mistake is the broad-stroke characterisation that it is a bad time to be vested in stocks.

It is not exactly a bad time to be vested in stocks. Stock indices such as the S&P 500 (the most widely used equities benchmark in the world) and Nasdaq have returned to or exceeded pre-pandemic levels, and China’s economy has roared back to life.

In fact, those who are vested in US and Chinese stocks during the period of stock market recovery from April 2020 to date would have at least recouped their losses inccured in February and March, in what was on hindsight probably an overreaction to the Covid-19 pandemic.

What’s actually a train wreck is the Singapore stock market, which has mounted an almost non-existent attempt at recovery from its March lows and now finds itself stuck at either moving either sideways or on a depressing downtrend. Blue-chips such as Singapore Airlines, Singtel and DBS—three of top 30 locally-listed stocks that make up the Straits Times Index (STI)—have proven hugely disappointing to investors who had bought into these big boys believing they would recover most strongly after a crisis, or at least show some signs of life.

Little did they expect STI to be utterly left in the dust by every other major stock index in the world:

| Country | Index | % difference from pre-pandemic high* [Jan-Feb 2020] |

|---|---|---|

| Singapore | Straits Times Index | (-23.6%) |

| United Kingdom | FTSE 100 | (-20.8%) |

| Australia | S&P/ASX 200 | (-17.5%) |

| Hong Kong | Hang Seng | (-14.9%) |

| United States | Dow Jones Industrial Average | (-4.5%) |

| Japan | Nikkei 225 | (-2.4%) |

| United States | S&P 500 | (+0.8%) |

| China | SSE Composite Index | (+6.2%) |

| South Korea | Kospi Composite | (+8.2%) |

| United States | Nasdaq Composite | (+15.0%) |

*At close on 17 September 2020.

Even United Kingdom, which has been blighted by the double whammy of Covid-19 and Brexit, is faring relatively less badly.

In Asia, Singapore is outperformed by every other stock index. Meanwhile, companies with global presence and track records of industry-leading innovation have driven the China and South Korea’s domestic stock market to new highs.

Why is the Singapore stock market doing so badly?

It’s hard to pinpoint a single reason, but there are multiple contributing factors.

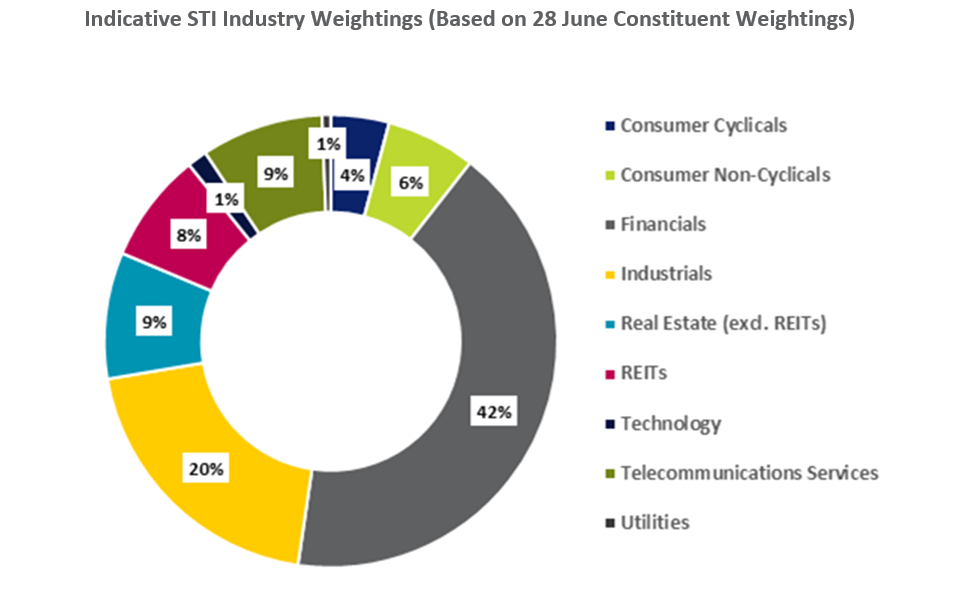

First is the sector mix of companies that make up our stock index, which is largely representative of our local and regional economies. The STI is made up of mostly banks (the big three of DBS, OCBC and UOB), and it’s the financial sector that tends to perform most poorly in a downturn, especially a zero-interest-rate downturn.

To perform in the stock market, it also takes a certain type of leadership and vision for a company to be consistently growing in earnings and profits, and for Singapore it means being able to take on and win in markets beyond our own. China has Alibaba, South Korea has Samsung, but sadly our homegrown listed companies haven’t had the same impact on the global stage.

Oh, and the tech sector that’s a growth driver for the past 15-20 years as well as the next few decades (regardless of Covid-19)? Well, that’s simply nowhere to be found on the STI, partly because the rare few local success stories like Razer and SEA Limited chose to list on the more lucrative Hong Kong and New York stock exchanges respectively.

All the while before Covid-19 stuck, the lack of innovative, breakout companies didn’t bother the average Singaporean investor. The STI’s blue-chips have long been reliable dividend payers, with 4% or higher annual payouts commonplace.

But the pandemic and its effects have crushed the rose-tinted illusion of local blue-chip dividend stocks. They have turned out to be everything but reliable, instead proving to be high risk low reward.

Disappointed in the STI but unwilling to vest too much in US equities

To jaded Singaporean investors, the US equity market may present a high-growth investment environment, but the reality is that their current life stages may preclude any heavy commitment towards US stocks and equity-based funds. Aside from volatility, there is also a general lack of faith in the US debt-driven recovery, which together with a weakening US Dollar dissuades investors outside the States from jumping in with both feet. (Dividends from US stocks are also subject to a hefty 30% withholding tax.)

For a Singaporean investor who is 55 years old and planning to retire in 5 to 10 years, perhaps less than half of ‘nest-egg assets’ should be vested in US equities.

This leaves the other, often sizeable half in question. “Where do I put my funds if I can no longer rely on the Singapore stock market, with the fate of many of its once-celebrated blue-chips in the balance?”

With a short time horizon to retirement or already into retirement, these investors know they should keep their investments in low-volatility instruments such as bonds or Real Estate Investment Trusts (REITs).

But with interest rates kept to a minimum, bonds are simply unattractive at the moment (and will be for at least the next five years) because of their measly yields.

Dividend-paying REITs, although they are typically likened to actual real estate, are anything but similar. With predominantly commercial and industrial holdings and traded like stocks, most REITs are highly correlated to the performance of the stock market and are only slightly less risky than stocks. Any appreciation in value may not be consistent and dividends may also be volatile.

So right now there’s a more robust argument than ever to make actual real estate a sizeable part of any Singaporean investor portfolio. Real estate is also the only asset type that allows for high leverage in its purchase, with very low risk to the borrower, because of the concept of using the purchased property as collateral. (Try asking the bank to loan you $200,000 for Tesla stock and you’ll see what we mean.)

That leverage to buy a property, also known as a home loan, is also now cheapest as it has ever been. Given the decline of STI blue-chips and relative risks and potential drawbacks of other investment types, coupled with rock-bottom interest rates and an economic crisis, Singaporeans are presented with conditions that make this the opportune time to buy a home or invest in real estate.

And not only are home loan rates across the world seeing an all-time low, home loans in Singapore are consistently among the cheapest form of loans in the world (currently at around 2% interest rate).

Real estate, as a real asset, also happens to be one of the most effective hedges against inflation, which is projected to increase in 3 to 4 years time in line with US Federal Reserve projections. And as inflation occurs, the actual value of a loan amount owned will diminish over its tenure. If home prices increase by 3% after 10 years due to inflation, that’s a chunk of home loan interest essentially written off.

Given that a new launch condo typically experiences an increase about 5% in value by the time it’s completed, buyers are essentially getting a zero-interest home loan right now. This will slightly offset the 12% Additional Buyer’s Stamp Duty (ABSD) too. It’s no wonder we keep getting told lately that viewing appointments at sales galleries are fully booked.

It’s not just push factors driving investors towards Singapore real estate

During the Covid-19 pandemic, private residential property prices in Singapore have failed to fall significantly as earlier predicted. Surprisingly, the official Price Index for private residential properties in Singapore increased by 0.3% in Q2 2020 (versus Q1 2020) even as the Gross National Product (GDP)—the measure of a nations’ economic performance—fell by a historic 42.9% in the same period.

Of course, it’s also important to mention that the Singapore government has been playing a pivotal role in making residential real estate a stable and attractive asset for mid- and long-term hold. Not only has the government prevented mortgage defaults during the height of the Covid-19 pandemic by letting owners defer their home loans, a series of measures have also helped locals hold onto their jobs, or at least have enough time to sell their homes at market value.

Singapore’s fabled property cooling measures, including the ABSD, is also a set of underappreciated tools the government has progressively implemented since 2009 to keep residential real estate from sliding down the ‘high-risk, speculative asset’ rabbit hole, which is characterised by volatile boom-bust cycles circa the 1990s.

The ABSD, while imposing a tax on Singapore Citizens buying more than one residential property, technically also puts them in a privileged position with a lower tax rate compared to Permanent Residents (PRs) and foreign buyers. This is a great way to moderate appreciation of property value over time while also ensuring Singaporeans get preferential terms when investing in—quite literally—their own homeland.

Arguably the best part about the cooling measures is that it also gives the government calibrated ammunition to protect buyers and investors from any excessive downside risk. For instance, when the property market happens to weaken past a certain point, the ability for the government to ease the ABSD can be a powerful shot in the arm for property demand.

So, as local investors continue to complain about ABSD, it’s about time they realised that Singapore property could justifiably represent that elusive blue-chip, medium-growth, medium-yield, not-very-high-risk asset that even Warren Buffet might like to get his hands on. Reliable as a safe-haven asset and proving resilient in the midst of the current economic downturn, Singapore residential real estate also has another perk: it’s something local investors can actually live in, too.

What do you think is currently driving property demand in Singapore today? Let us know in the comments below!

If you found this article useful, 99.co recommends How a deep recession could impact the property market in Singapore and 7 things Singapore landlords MUST DO to survive the 2020 recession

Looking for a property? Find your dream home on Singapore’s most intelligent property portal 99.co!

About Kyle Leung

Content Marketing Manager @ 99.co

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Agree 100% on all points!