The Seller’s Stamp Duty (SSD) was first introduced in 1996 to curb rampant short-term investment activity in Singapore’s private housing market. The framework has seen multiple changes over the years; including a rollback and a reintroduction in 2010. The 2025 revision, however, marks the most substantial tightening of SSD rules since 2017.

We have already captured the impact of the policy change on new launches and the tertiary sub-sale market. In this deep dive, we examine in detail what led to the SSD hike, where the sub-sale market has grown disproportionately, and how this latest update hopes to reset buyer behaviour.

Table of contents

The anatomy of a sub-sale: Where, when, and how

Before diving into the causes behind the rise of sub-sales, it’s important to understand what defines a sub-sale and how it differs from a resale.

A sub-sale refers to the transaction of a private residential unit before it obtains its Temporary Occupation Permit (TOP). In contrast, a resale occurs after TOP, once the property is completed and issued its official occupancy status. The classification depends on construction status of a given project: If the unit is still under development, the sale is logged as a sub-sale.

Sub-sales typically occur when a buyer who originally purchased a unit directly from the developer decides to sell it to another buyer before taking possession. The incoming buyer inherits the original Sale and Purchase Agreement (S&PA) terms, but the developer must now issue a fresh S&PA to this new party.

In contrast, resale transactions involve completed units, often several years post-TOP, and are handled directly between the seller and buyer, without the developer’s reissuance of contracts.

Okay, this sounds perfectly normal. Why is this an issue, again?

Sub-sales, at a glance, are just another form of property transaction. You could even frame it as savvy investing or portfolio reshuffling. The issue lies not in the act of sub-selling itself, but in the market psychology it fuels.

Let’s say you have a condo in a new launch project which you would like to sell in the future. You see that someone just sold a unit in the same project for S$1.6 million, before the unit was even completed!

Suddenly, every other seller in that area, including you, starts to think that their unit should also fetch a similar price, or higher. Prices start to rise not because of real demand, but because of an expectation of profit.

And let’s be real, sub-sales can bring in really good profits

That’s because sub-sellers typically buy units at early-bird launch prices, when developers are still trying to meet minimum sales quotas. These units often come with early discounts or incentives. If the project sells out quickly or sentiment improves before the TOP, sub-sellers can sell their units at a premium, without ever living in them or paying much in holding costs.

Let me put on my realtor hat and help you with the math.

Imagine Mr. X picked up an OCR condo unit at S$1.5 million in 2020 during a new launch, and sold it in 2023 before the project completes for S$1.8 million. There would be no mortgage to pay, due to the progressive payment scheme. And no ABSD, as this is Mr. X’s first purchase. Even after factoring in Seller’s Stamp Duty at 4% (as per the old 2017-2025 rates), legal fees, agent commission, and other expenditures, that’s still a potential net gain of about S$250,000 in three years.

And this isn’t hypothetical.

According to reports, the average profit made on sub-sales in 2024 was around S$270,000. Some standout sub-sales include:

- A unit at Boulevard 88, purchased in March 2019 and sub-sold in April 2023, which yielded a whopping S$3.9 million in gains

- A unit at Marina One Residences, sold for over S$2 million in profit within a few years of launch

But of course, not all sub-sales end with champagne. In 2024, 17 sub-sale transactions were unprofitable, with average losses of around S$90,000. Some of the more painful examples include a S$297,600 loss at Riviere, and a S$132,000 loss at Sky Everton.

Interestingly, 8 out of those 17 loss-making sub-sale occurred before the SSD period had expired, indicating that sellers were likely under financial pressure and couldn’t wait out the minimum holding period.

So are sub-sales a concern only when they cause losses?

Data shows that 80–90% of homeowners hold their property beyond 4 years. And sub-sales are less than 10% of overall transactions in most years. So, on the face of it, there really shouldn’t be a problem.

Here’s the thing though: sub-sales aren’t just risky when someone loses money. The real problem is when they affect the rest of the market. In economics, this is a well-documented effect called a “price signalling distortion”, where a small set of transactions disproportionately influences the broader market’s behaviour.

Sub-sale investors tend to cluster in new, high-visibility projects, which have a sure potential for appreciation. When these new units are sold at sharply higher prices before completed, it raises the perceived market value of the project.

These super-high ‘benchmark’ prices aren’t based on what people can actually afford or how much rent those homes would bring in. It’s mostly driven by the optimistic investor’s notion that prices will just keep climbing.

So while most homeowners aren’t selling early; the small group that does, still ends up steering the direction of the market. And that’s the real issue.

As long as things stay stable—low interest rates, steady demand, few restrictions—this behaviour might keep the market buoyant. But the moment something shifts—say, an interest rate hike or a new tax—buyer sentiment can turn quickly.

Owners who bought at the peak, hoping to cash out fast, might find themselves holding a property that’s worth less than what they paid for it. What was meant to be a quick profit becomes negative equity.

And it doesn’t stop there. A sharp price correction can hit not just individual owners, but also banks, developers, and buyer confidence across the board; dragging the rest of the economy down with it.

Has Singapore ever gone through this bubble before?

Yes!

One of the most memorable market bubbles was in the mid-1990s, when sub-sales were rampant. From 1986 to 1996, Singapore’s private residential property index surged by approximately 440%, with roughly two-thirds of that growth concentrated in the early 1990s. In 1996 alone, nearly 1 in 5 transactions was a sub-sale, prompting the government to introduce the first version of Seller’s Stamp Duty (SSD). So rampant was the property mania that there used to be midnight queues outside new launches, and every coffee shop owner was moonlighting as a property analyst.

Another spike came during 2009 to 2013, after the Global Financial Crisis. Buoyed by low interest rates and liquidity, investors flooded back into the market. Sub-sale activity surged again, making up 13% of all private non-landed home sales. This prompted multiple rounds of cooling measures, including the reintroduction of SSD in 2010, and the introduction of Additional Buyer’s Stamp Duty (ABSD) in 2011. These steps were aimed precisely at reducing short-term buying and restoring price stability.

And we have seen sub-sales spike recently as well.

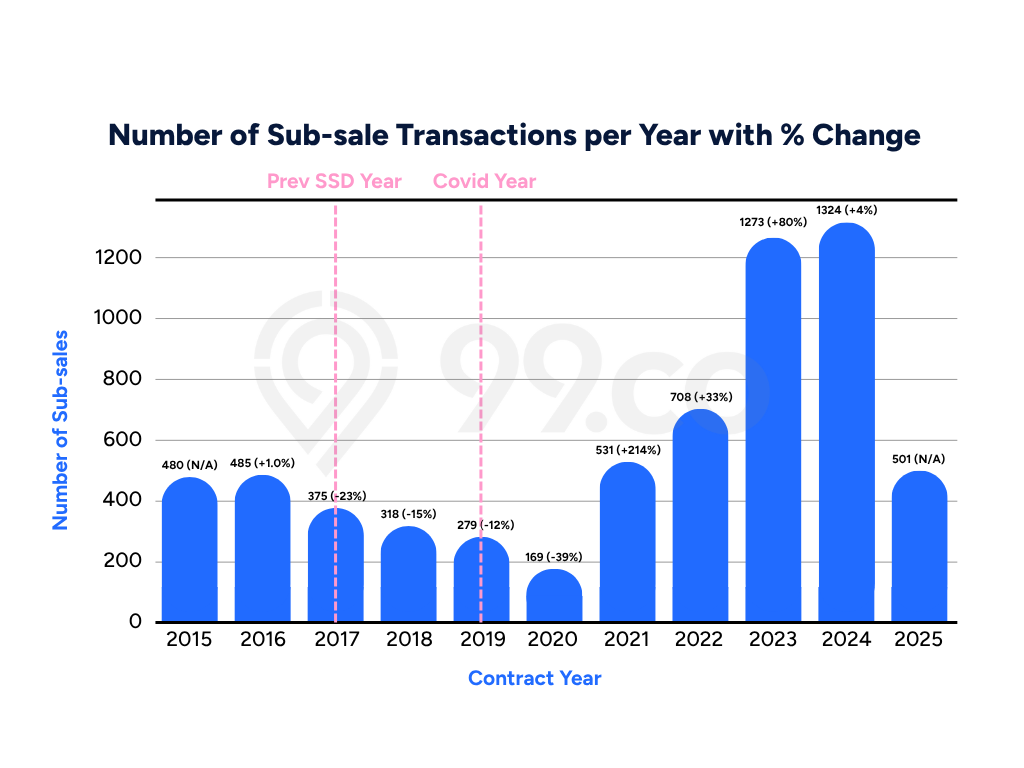

Between 2020 and 2024, the URA’s private property index surged by roughly 33.4%. At the same time, homeowners who were facing TOP delays due to the pandemic, saw a clear opportunity to exit for profit. Sub-sale volumes rose sharply after 2020, climbing from just 169 transactions in 2020 to 1,324 by 2024, the highest in nearly a decade. In overall percentage terms, sub-sales surged from 1.1% of all transactions in Q4 2020 to 9.8% by Q4 2023.

| Region | Share of sub-sales | Units sold | Key drivers |

| OCR (Outside Central Region) | 57.8% | 755 units | More affordable launch prices, larger buyer pool, investor-friendly developments |

| RCR (Rest of Central Region) | 38.4% | 502 units | Attractive mid-tier projects near MRT lines and city fringe growth areas |

| CCR (Core Central Region) | 3.8% | 49 units | High entry prices limit demand; fewer short-term buyers |

A large chunk of this sub-sale activity came from condos in the Outside Central Region (OCR). In 2024, this region alone accounted for 57.8% of all sub-sale transactions, followed by Rest of Central Region (RCR) projects, which contributed 38.4% or 502 units. The Core Central Region (CCR), with its higher price barriers, saw just 3.8% or 49 units sub-sold during the year.

Let’s also look at the top 10 projects that saw the highest number of sub-sale transactions in 2024, along with their average capital gains:

| Project name | Average capital gain | Sub-sale count (2024) |

| Clavon | S$375,581 | 72 |

| Penrose | S$370,013 | 72 |

| Parc Clematis | S$408,878 | 64 |

| Normanton Park | S$263,581 | 61 |

| The Florence Residences | S$170,691 | 55 |

| Sengkang Grand Residences | S$295,030 | 38 |

| Affinity at Serangoon | S$238,822 | 32 |

| Treasure at Tampines | S$302,686 | 29 |

| KI Residences at Brookvale | S$407,894 | 20 |

| Riverfront Residences | S$258,216 | 17 |

The top three developments each saw over 60 sub-sales, with gains averaging well over S$350K. These units sold after being held for just over 3 years but before reaching the 4-year mark, allowing sellers to minimise their SSD liability under the pre–July 2025 rules.

Mega-developments like Normanton Park and Treasure at Tampines also saw high volumes. These projects launched over 1,000 units each and attracted short-term buyers who could exit easily due to size, demand, and strong price appreciation.

So, if the latest spike was mostly due to COVID, then was a policy revision necessary?

Yes, construction delays gave owners a rare loophole, allowing them to sell before TOP without incurring costs. However, as we have noted in this piece, the SSD hike isn’t just a reaction to a few high-profile sub-sales, or a COVID-era loophole. It’s a reflection of how fast the sub-sale market has evolved in recent years, and the possibility of a 90’s style bubble distorting the market.

In a rising market, profits from sub-sales can seem like an inevitable part of the cycle. But when they start to shape pricing psychology and outpace owner-occupier demand, it becomes clear that some correction is needed.

The latest SSD revision doesn’t “punish” investors. It only encourages longer holding periods, steadier growth, and removes artificial price surges from the market. As with past cycles, the goal isn’t to eliminate short-term investments altogether, but to keep them in check. So that the system can keep working for those who need homes, not just those chasing returns.

With this revision, policymakers are once again nudging the balance back toward sustainable ownership, and reiterating that real-estate in Singapore is not just an asset class meant for easy gains.

About 99.co

We are a property search engine with the overarching goal of building a more transparent and efficient property market. We are working towards that future by empowering people with the tools and information needed to find a place to live in the best way possible.

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Leave a comment