HDB decoupling has been a cost saving tactic since around 2013. Once the Additional Buyers’ Stamp Duty (ABSD) was announced, several investors quickly caught on to what was essentially a legal loophole. By transferring full ownership of their flat to a spouse, they could attain their second property at a much lower cost. This has since been changed, but it leaves us wondering why it took so long in the first place:

How does HDB decoupling work?

HDB decoupling occurs when one spouse transfers full ownership of a flat to the other. This can happen for a range of reasons, chief among them being divorce. But when the ABSD was revised in 2013, decoupling became an unintentional method of tax avoidance.

In January 2013, it was announced that the ABSD would affect Singaporeans buying a second property (previously, it only affected Singaporeans buying their third property.) The ABSD now imposes a tax of seven per cent on the property price of a second home.

As a consequence, some couples began to use decoupling to avoid the added tax. They would transfer full ownership of the flat to their spouse (by declaring it a gift), and as such would no longer be property owners. When they then purchased a second property, it would still count as their first.

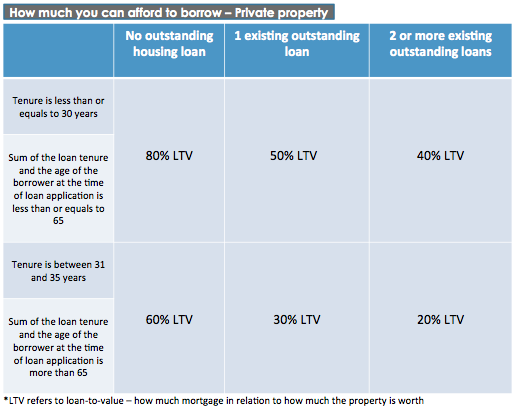

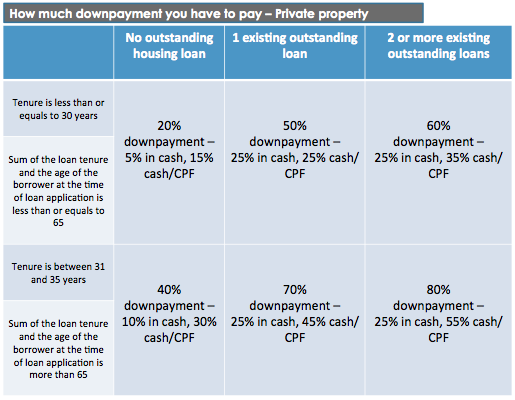

There is a second reason for HDB decoupling: this is to utilise a greater portion of CPF savings when buying property. In most cases, a buyer with no outstanding home loan can borrow up to 80 percent of the value of the house. Of the remaining amount, 15 percent can come from the CPF (the other five percent must be in cash.)

For example, when purchasing a house with a value of $1 million, a buyer would normally be able to use $150,000 from CPF to pay for it.

However, a buyer with an existing property is required to set aside half the Minimum Sum (MS) when using it to buy property. The MS is an amount that must be set aside to create a Retirement Account (RA) upon reaching the age of 55. At present, the MS is $161,000. Visit the CPF website for more details.

As such, a buyer with an existing property must leave at least $80,500 in their CPF.

By decoupling, a prospective buyer would own no property (it is fully transferred to their spouse), and would be able to use CPF monies without restriction.

HDB decoupling was not an obscure practice; it was explained in several websites, and in some cases was even taught to couples at seminars.

New restrictions against HDB decoupling

From 1st April 2016, decoupling will only be allowed under specific situations. These include marriage, divorce, death of an owner, financial hardship, loss of citizenship, and medical grounds. This could have a small impact on the market of potential buyers, who may find a second property less attractive after the ABSD.

Why we should have put an end to it long ago

We believe the restrictions against decoupling are appropriate. This reaffirms the nature of HDB flats as public housing, with an emphasis on affordability and family building. HDB flats should not be used as investment tools.

In addition, HDB decoupling was not without its hazards. By shifting the entire weight of mortgage payments on one spouse, while the other proceeded to take on another loan, there was a higher possibility of over-leveraging. In the event of job loss, for example, this could have a devastating impact on family finances.

Some borrowers may also face problems in future, if relationships sour. If one were to transfer the entirety of a flat to their spouse, they will no longer have any say over whether the flat is sold. In the event of separation, this could cause issues with borrowers who lacked foresight.

That said, according to HDB, the changes for decoupling are just part of a regular policy revision. They were not made in response to buyers avoiding ABSD. This suggests that a more proactive approach is needed toward those who seek loopholes.

While such loopholes may provide short term gains for property sellers, it creates an unhealthy environment in the long run – one in which property agents are encouraged to point out legal loopholes, and buyers are encouraged to “game” the system.

During market downturns such as the present, buyers will be enticed by falling prices. Many will possess a risk appetite that exceeds their true capacity for risk. In this example, we witnessed some buyers willingly dig into their retirement provisions (via the CPF) in order to buy a second property. As decoupling was always discussed in the open, we feel efforts could have been made to nip it in the bud earlier.

About Ryan Ong

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Leave a comment