Beyond the proverbial life goal of owning a condo apartment in Singapore, there is owning an Orchard Condo like Lloyd 65.

With property prices always chasing ahead of income, it seems a distant dream for most to own a prime location condo.

But is it? In a market where many property developers are suffering from weak demand and looming QC/ABSD penalty, this just may be the time to look closely to leverage on discounts and creative schemes offered by developers, to check this off your bucket list and build asset value.

In this article, we review an innovative Rent-to-Buy scheme to see how one can start owning a property in Orchard (Somerset to be exact) for just $200k!

Who is this Lloyd 65 hack great for?

In short – anyone who is

a) Looking to buy a unit for investment or residence in prime location Singapore

b) Has ~200k CASH (note: NOT CPF)

c) Does not have much additional cashflow in the next 2 years

d) Able to hold property for min. 6 years

e) Not affected by ABSD (or that you believe ABSD would be reduced in the next 2 years)

(Note: Foreigners exempted from ABSD includes citizens of US, Iceland, Liechtenstein, Switzerland and Norway)

What is this Lloyd 65 “Rent-then-Buy” scheme?

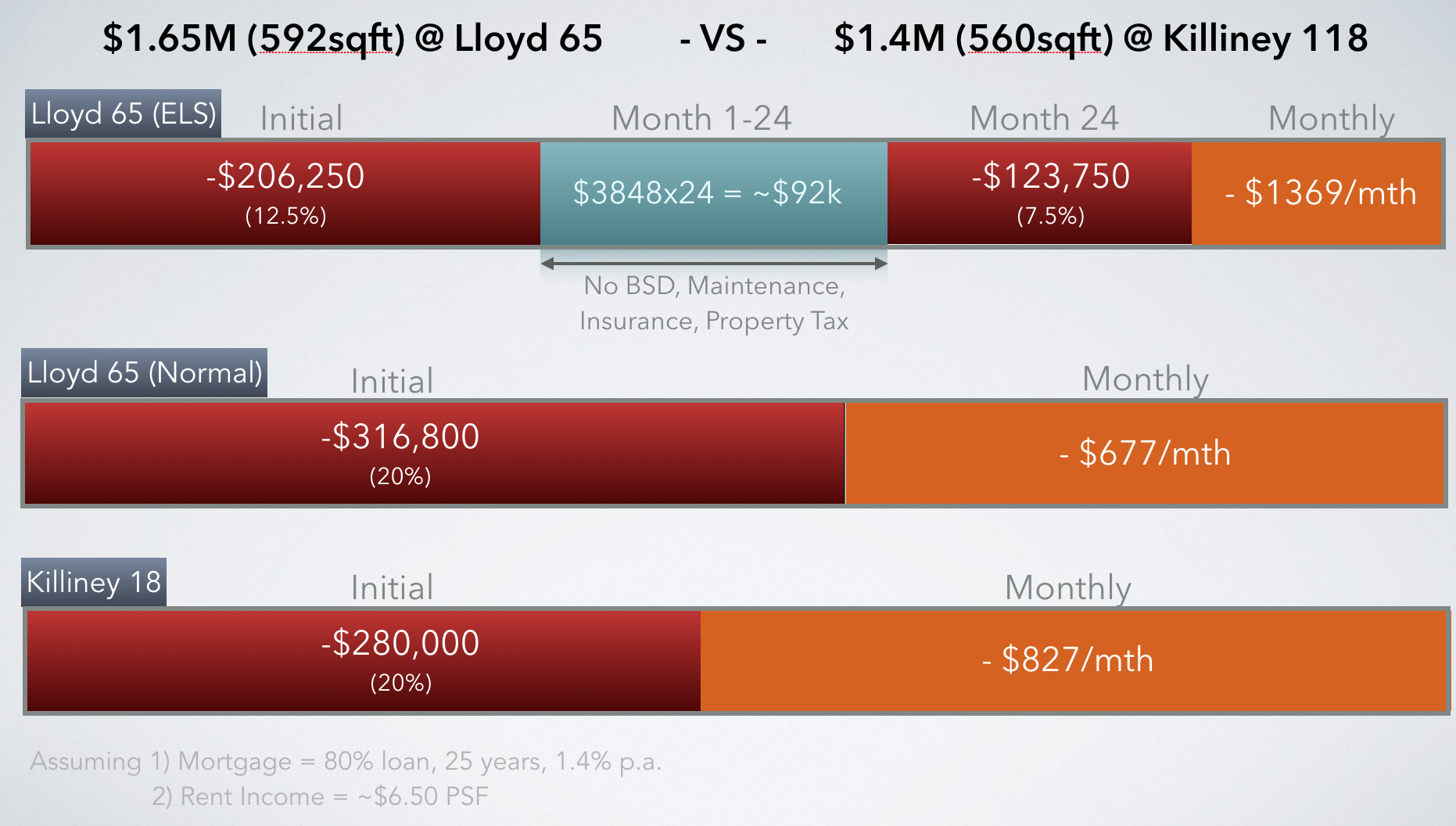

As the name implies, the intent of the scheme is to enable potential buyers of the property to rent it first, try it out, and then decide if they want to buy it. They also have the option to convert the rent paid over 2 years as part of the downpayment for the apartment.

Another way of looking at the scheme is that you only need to put up an initial capital of 12.5%, pay no additional instalments for 2 years, collect rent during this period (or save up if you choose to live there), and then complete the rest of the 7.5% to make it to 20% down payment (assuming you are taking 80% loan). This is the lowest % you need to pony up today in the market, as far as we know, to take the first step to owning a property.

What is so great about it?

Real estate as an asset class does not actually appreciate as much as some other riskier assets, such as mutual funds or stocks. However, one of the key concepts in why real estate is an attractive investment is the idea of capital leverage.

Essentially, if you have $20 and you buy stocks and it appreciates 5% a year, you get $1 gain. But if you have $20 and you buy a $100 property (since banks will lend you $80 on your property), and your appreciation is 3% a year, you get $3 gain. (you might have to pay the bank 50 cents on that 3 dollar in interest, but you still gain more)

This is called the Return on Equity.

This is the key benefit of this scheme as it allows the buyer to pay a much lower upfront cost, by starting to rent the apartment, as a step to eventually owning it. What this does is that it essentially allows you to start building equity on an apartment that is fundamentally worth more with a lower initial capital (12.5% instead of 20%), and then leverage on the potential rent or savings you can accumulate in the next 2 years to offset the rest of the “Top-Up”.

In summary:

The Math

So, it takes less capital upfront to buy – but does that mean its a good buy?

Here we take the Lloyd 65 Experiential Leasing Scheme into comparison with 2 other similar properties in the same vicinity, within 500m of SingTel Comcenter.

| Lloyd 65 (ELS) | Killiney 118 | Espada | |

| Price | $1,650,000 | $1,400,000 | $900,000 |

| Size | 592 | 560 | 355 |

| PSF | $2,787 | $2,500 | $2,535 |

| Initial Capital (L65=12.5% , Rest=20%) | – $206,250 | – $280,000 | – $180,000 |

| Bank Loan Amount | $1,120,000 | $720,000 | |

| Est. Monthly (80% loan, 25 years, 1.4% p.a.) | $4,427 | $2,846 | |

| Year 1-2 | |||

| Rental Asking Price (Lowest) | NA | $3,800 | $2,600 |

| Realistic Rental Income /mth | $3,848 | $3,640 | $2,308 |

| Rental PSF | $6.50 | $6.50 | $6.50 |

| Rental Income over 2 years | $92,352 | $87,360 | $55,380 |

| Cash flow in year 1-2 | + $92,352 | – $18,888 | – $12,924 |

| % of the home you own at the end of 2 years | 12.50% | 25.40% | 25.40% |

| Equity value in $ at the end of 2 years | $206,250 | $355,600 | $228,600 |

| Year 3-6 | |||

| L65 – top-up payment to 20% | $123,750 | ||

| Mortgage Remaining | $1,320,000 | $1,044,400 | $671,400 |

| Monthly payment | $5,217 | $4,427 | $2,846 |

| Rental Income over 4 years | $184,704 | $174,720 | $110,760 |

| Cash outlay in year 3-6 | – $189,462 | – $37,776 | – $25,848 |

| How much of the home you own at the end of 6 years | 31.00% | 36.73% | 36.73% |

| Equity value in $ at the end of 6 years | $511,441 | $514,216 | $330,568 |

| Selling after 6 years | |||

| Base PSF (in Q3 2016) | $2,500 | ||

| PSF Appeciation /year | 3% | ||

| Selling PSF | $2,985 | ||

| Selling Price | $1,767,197 | $1,671,673 | $1,059,721 |

| Capital Gains | $117,197 | $271,673 | $159,721 |

| Mortgage Remaining | $1,138,559 | $885,784 | $569,432 |

| Cash gain at sale | $628,638 | $785,890 | $490,289 |

| Initial Capital | $206,250 | $280,000 | $180,000 |

| Return on Initial Capital | 305% | 281% | 272% |

If you want to play around to see the effect of PSF Appreciation on this calculation, you can find the spreadsheet here

So is it a winner?

We believe so! You have a larger “capital leverage” because you pay less upfront for a larger asset. If you forecast a conservative 3% appreciation on the PSF price of the property per year, which we believe is a reasonable forecast as the national average over last 25 years has been 4.76%. At that appreciation rate, Lloyd 65 would have a better return on equity than other comparable projects in that area!

What’s the catch?

First, the obvious – the effective “rent” you pay to the developer at $6750/mth for a 1-bedder doesn’t really make sense, as similar apartments are asking for $3.5k on 99.co, so we would not advice you to rent it just for the sake of renting. If you decide to go with this scheme, you should be fairly sure that you will end up buying it. (The flexibility to pull out and not go ahead with the purchase does have some benefit, e.g. if you are a trader with $200k savings and counting on a big bonus next year for you to pay for the remaining 7.5% to get to 20% down payment, this gives you some flexibility in case the world does come crashing down and wipes everyone’s bonuses out)

Secondly, the Per-square-foot price you pay is a good 10% more than market, at about ~$2750 versus comparable projects like Killiney 118 and Espada at ~$2500. This is, of course, a premium you pay to essentially be able to put down a lot less initial capital to start building equity in a higher value property. (The developer is essentially loaning you money)

Thirdly, because the initial 12.5% is “Rent”, it can only be paid in CASH and you cannot use your CPF – so this scheme is good only if you have the cash reserve.

For the real estate geeks – how did Lloyd 65 manage to do this?

(Are there other such similar schemes?)

TG Development, the developers behind this project have 3 unique qualities that enable them to put out this scheme to attract buyers

- They are privately owned

(Trivia: owned by the Ong family known for our beloved Tong Garden nuts) - They bought the land before 2011 when ABSD rules were imposed

- They have deep reserves and don’t need the cash

Thus TG Development are not subjected to QC/ABSD penalty and are able to offer the flexibility to the potential buyers to “rent” the place for a much smaller sum upfront, instead of buying it off their hands. We don’t know for sure if there are other developers who could or would offer similar schemes, but it certainly rules out most big listed developers and projects!

== This is part of the 99co Buying First-Hand series, where we take an in-depth analysis of the market for buying from developers ==

Leave us a comment if you want us to clarify anything or analyse another property you are interested in!

About Darius Cheung

CEO at 99.co

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

This is a terrible scheme to advice people and can only be written by the developer. It’s very easy to conduct fraud with this and run away with your money within that 6 years. In real estate transaction it is most important to settle as quick as possible. This article asks you to extend it.

Singaporeans in general have a safe environment to imagine such things to happen, but I feel this article does more harm than good because there is no 2 sides to the argument.

hey justin, if you are referring to “fraud and run away with your money”, it’s really not applicable here since the property is almost already completed, and you will have an Tenancy Agreement that protects your interest as a tenant for the unit for 2 years, and plus an option letter that clearly indicate your right to purchase the unit if you so wish to.

if you are referring in general to developers in other countries who would sell “on plan” (i.e. before the property is built), and run away with the money, it is also not possible in singapore. as singapore has specific regulations around this – essentially sales proceeds are deposited into a special account that developers cannot access (and cannot draw out the money) until a certain stage is completed. We will do an article on this in the future, the full regulations can be found here – http://statutes.agc.gov.sg/aol/search/display/view.w3p;page=0;query=DocId%3A%222f859531-df46-4385-a693-f663b44b7ed6%22%20Status%3Ainforce%20Depth%3A0%20ValidTime%3A%2215%2F06%2F1997-00%3A00%22%20TransactionTime%3A%2225%2F08%2F2016%22;rec=0

this actually makes it incredibly safe to buy first hand units from developers in singapore, which we understand is not the case in many other countries.

I suppose the assumption is the 3% appreciation. 1. There can be base case of no increment. 2. What about buy and hold and not to sell in 6 years?

Yes the base case assumption used in the calculation is 3%.

And yes it is possible there is no appreciation at all (or in fact a decline), we picked 3% because it’s a reasonable guess since last 25 years national average is about 4.7%.

You can play around with the spreadsheet, so yes at 1% it would not outperform the other 2 comparables, but from 2% onwards it would start outperforming.

—

Your 2nd question – buy and hold beyond 6 years?

well we dont have a spreadsheet done up, but if u assume consistent appreciation of at least 3%, it should continue to outperform the other 2 comparables because you have better leverage.

(of course.. if you never sell, like ever, which is extremely unlikely, then there is no such “gain” to talk about, then frankly L65 would actually be a bit more pricy than other comparables because you are essentially paying a premium for better leverage and flexibility)

This is a great blog.

As a foreigner in Singapore, I’ve heard of new financing schemes that are being offered by developers. I like the part you showed the condo comparisons, maths, and pros-cons of the schemes. Some “Rent-then-Buy” articles don’t provide the example of it, hence it leaves users scratching their head (me included). Following is the example: http://www.straitstimes.com/business/property/rent-then-buy-property-developer-dangles-new-lure

Keep up the great work.

Thanks! i’d heart/like your comment if i could! =)

Is this scheme still available?.If put down 800k will it be better?