In September 2024, Singapore’s rental market saw a noticeable slowdown, with both condo and HDB rental volumes dropping for the second consecutive month. Although the volume declined in both rental sectors, Condo rental prices showed signs of stabilisation. The rental market appears to be in a period of flux, and the upcoming months will be critical in determining whether these trends represent a temporary pause or a more sustained shift.

A large wave of new condo completions is expected to influence the rental market in the coming months. Approximately 7,000 new condo units will be completed in the second half of 2024, increasing the available rental inventory and potentially easing the tightness that has characterised the market for some time.

Table of contents

Let’s dive deeper into the rental market in September 2024!

Condo Rental Market – September 2024

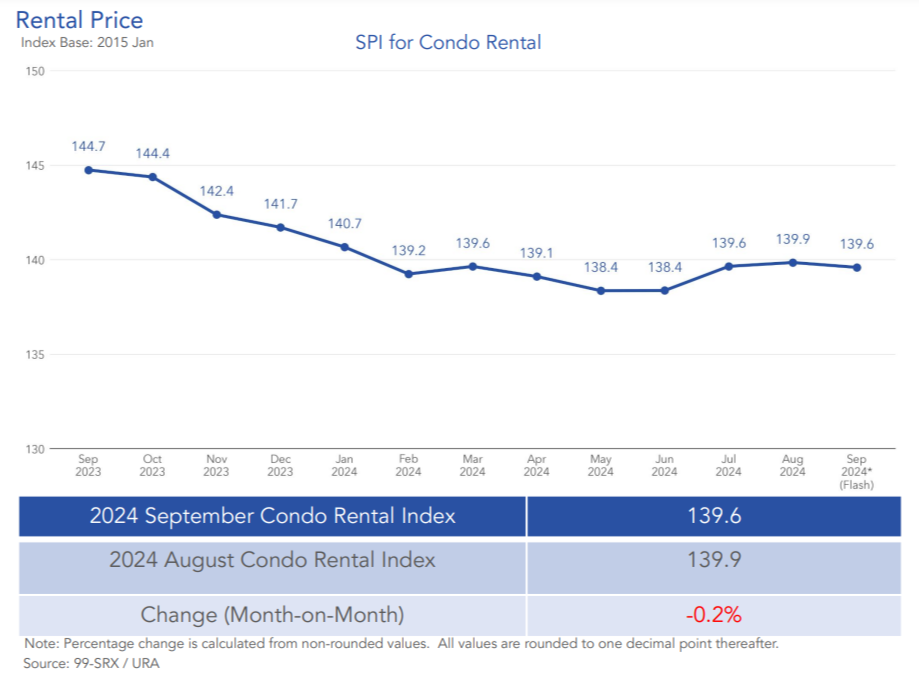

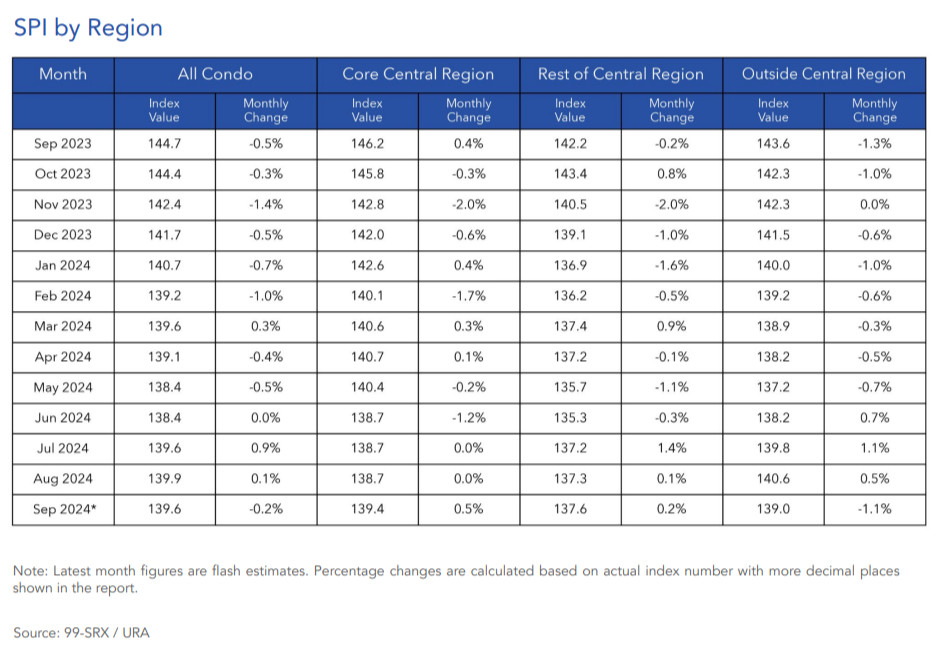

Condo rents decreased by 0.2%

In the private condominium sector, rents saw a slight dip in September 2024, falling by 0.2% compared to August. However, this decline did not happen across all regions. Rents in the Core Central Region (CCR) and the Rest of Central Region (RCR) increased by 0.5% and 0.2%, respectively, suggesting continued demand for central and city-fringe properties. In contrast, rents in the Outside Central Region (OCR) dropped by a more noticeable 1.1%, likely reflecting the increased competition in suburban areas where new developments are concentrated.

On a year-on-year basis, condo rents have decreased by 3.6% from September 2023. This decline happened across all regions, with rents in the CCR dropping by 4.7%, RCR by 3.2%, and OCR by 3.3%. These decreases indicate a general cooling in the rental market, which may be a response to the ongoing stabilisation of rents as well as the anticipation of new supply entering the market.

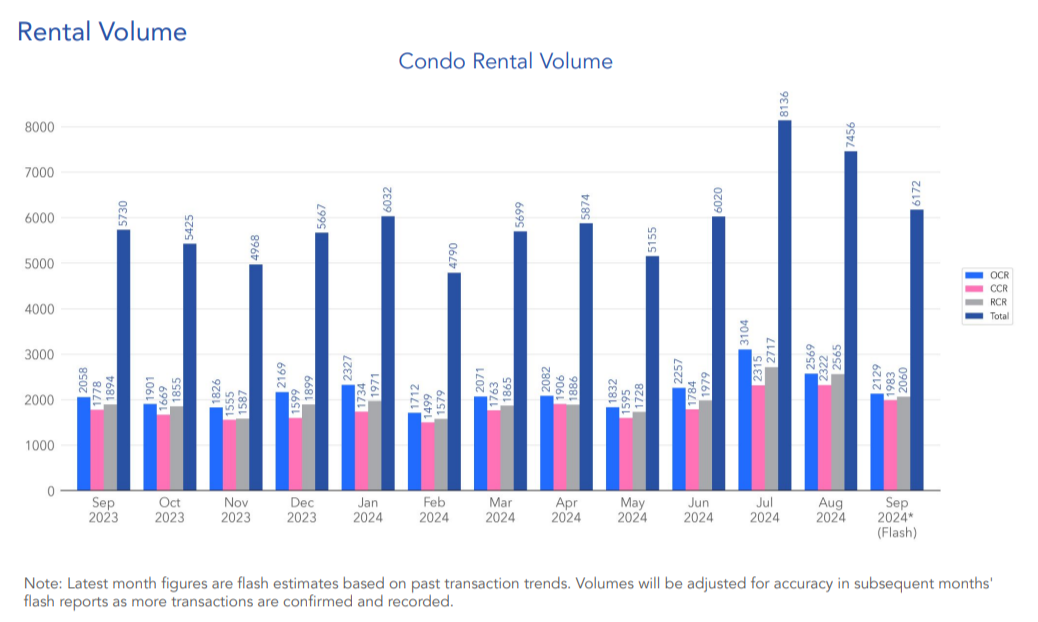

Condo rental volumes decreased by 17.2%

Rental volumes for condos dropped sharply, with an estimated 6,172 units rented in September 2024, representing a 17.2% decline from August. Despite this month-on-month dip, rental volumes were 7.7% higher than in September 2023, indicating that demand remains resilient compared to the previous year. However, rental activity in September was still 5% below the five-year average for this month, suggesting that the market is entering a quieter phase.

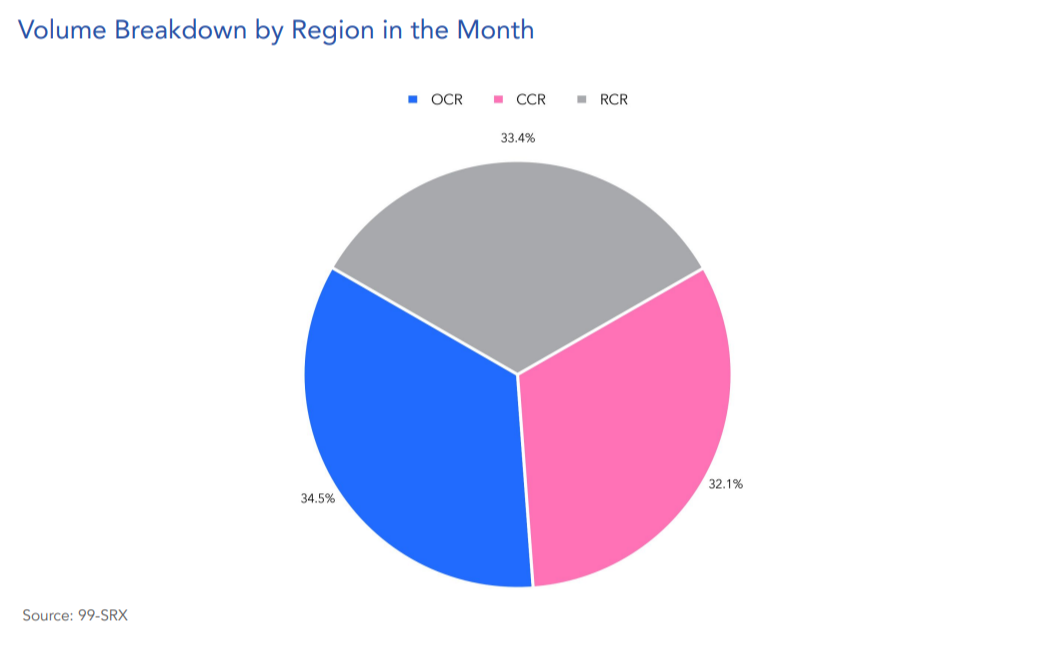

Regionally, the distribution of rental transactions was relatively even, with 34.5% of the total volume coming from the OCR, 33.4% from the RCR, and 32.1% from the CCR. This even split highlights that demand for rental properties remains steady across different parts of Singapore, even as overall volumes decrease.

Additional reading: August 2024: Rental volume drops on both Condo and HDB; 12.3% decrease amid a year-on-year decline for HDB

HDB Rental Market – September 2024

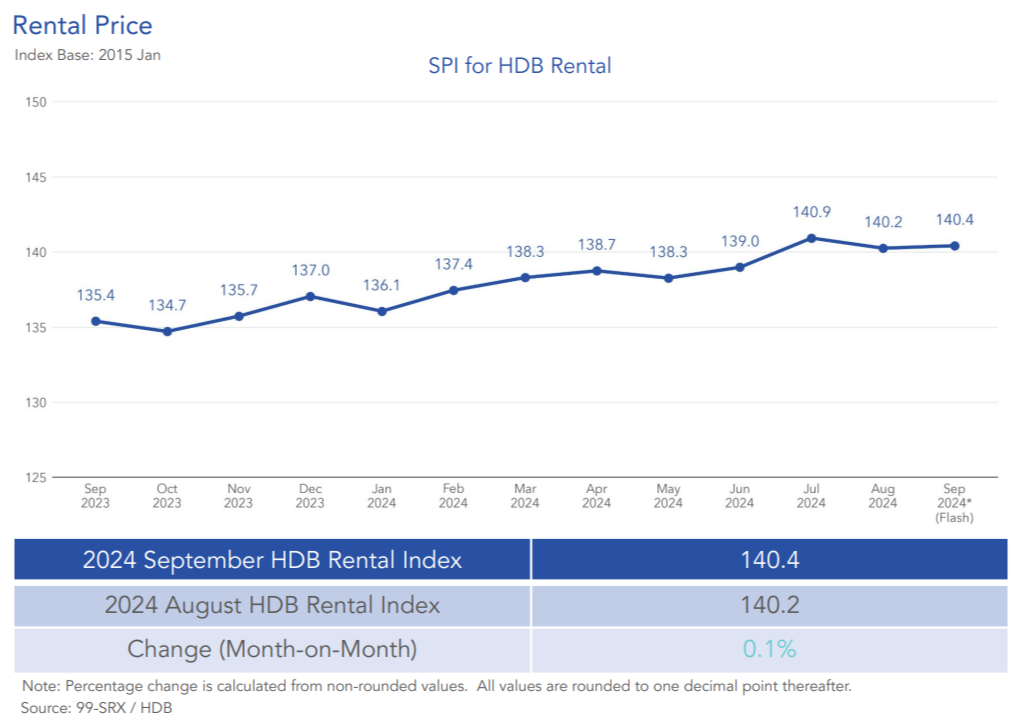

HDB rents increased by 0.1%

The HDB rental market experienced a similar trend, with rents increasing by just 0.1% in September 2024 compared to August. There was some variation within this overall increase, as rents in Mature Estates dipped by 0.1%, while Non-Mature Estates saw a rise of 0.3%.

Looking at the year-on-year performance, HDB rents increased by 3.7% from September 2023, reflecting continued demand for public housing rentals despite the overall slowdown in activity. Both Mature and Non-Mature Estates saw rents rise by 3.7%.

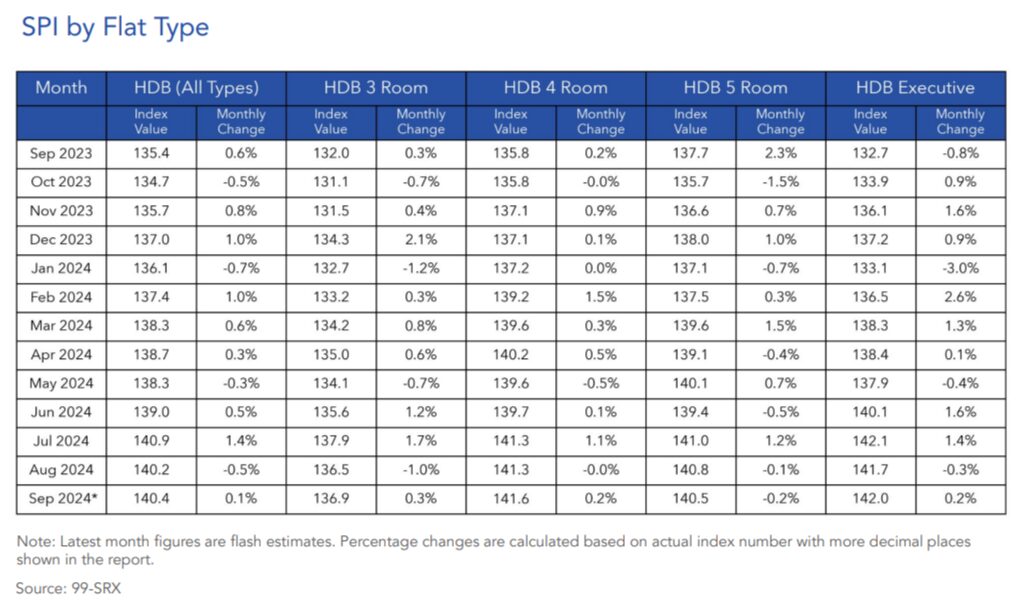

In September 2024, the rent increase was spread across different flat types, with 3-room, 4-room, and Executive flat rents rising by 0.3%, 0.2%, and 0.2%, respectively. However, rents for 5-room flats fell slightly by 0.2%.

Additionally, all flat types recorded rent increases compared to the previous year, with 3-room flats seeing a 3.7% rise, 4-room flats increasing by 4.2%, 5-room flats growing by 2%, and Executive flats showing the largest increase at 7%. This suggests that while the market is stabilising, there is still a strong preference for larger flats, particularly Executive units, which offer more space.

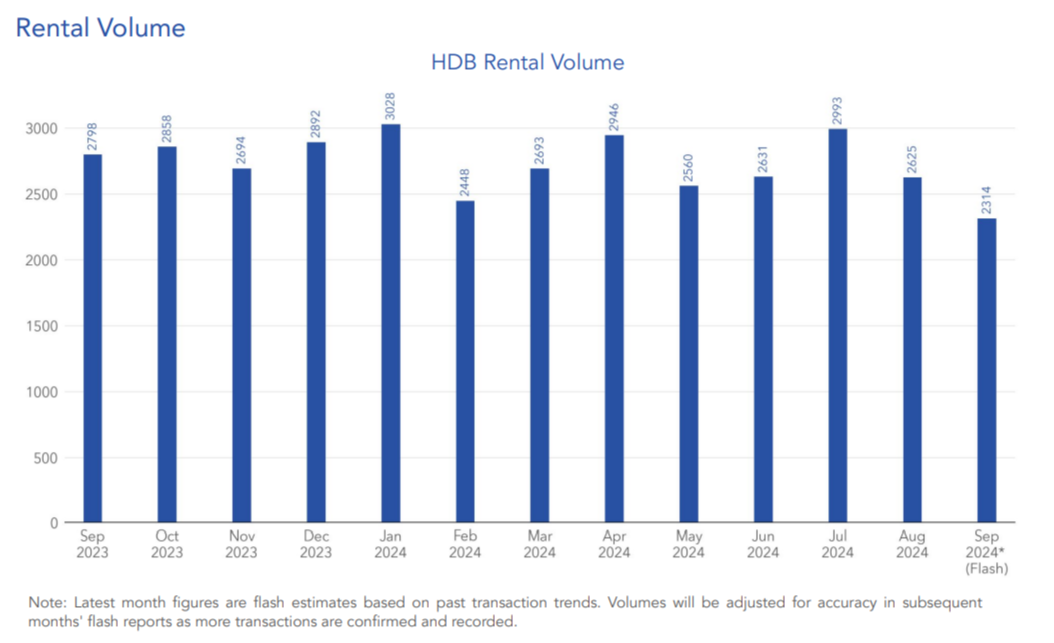

HDB rental volumes decreased by 11.8%

Rental volumes in the HDB market also fell sharply, with an estimated 2,314 flats rented in September 2024, an 11.8% decrease from the 2,625 flats rented in August. Year-on-year, HDB rental volumes were down by 17.3% compared to September 2023, further highlighting the cooling in the HDB rental market. This month’s rental volumes were also 11.7% lower than the five-year average, suggesting that the market is quieter than usual.

This decline in volume may be partially explained by the migration of tenants to newly completed condos. Additionally, some HDB owners are likely upgrading to private properties, which could further reduce rental demand for HDB flats.

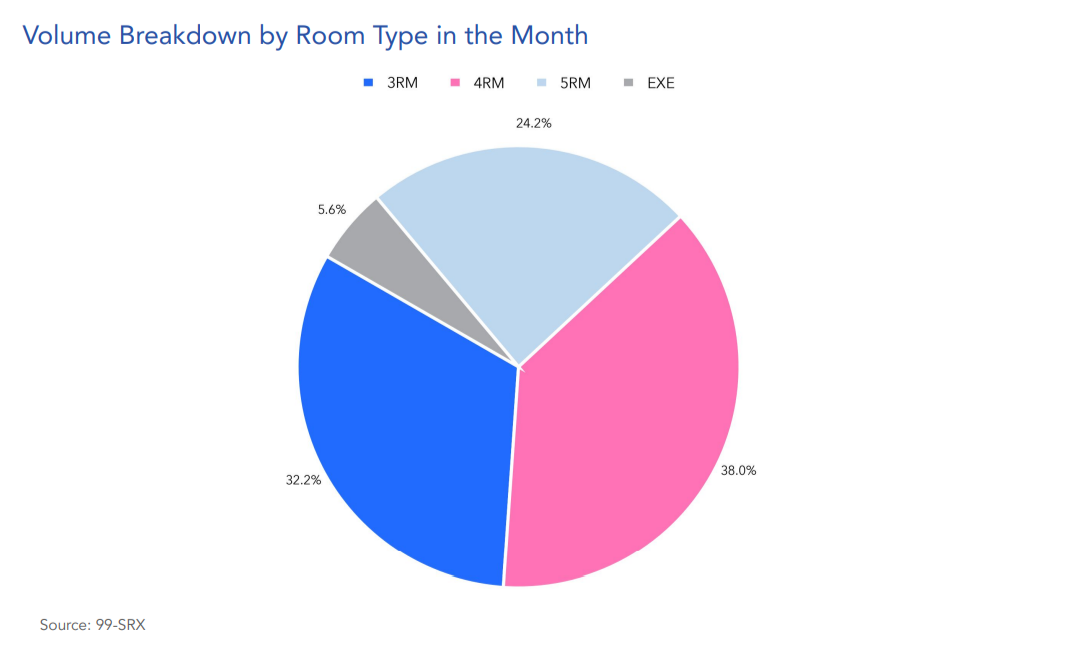

Breaking down the rental transactions by flat type in September 2024, 32.2% of the volume came from 3-room flats, 38% from 4-room flats, 24.2% from 5-room flats, and 5.6% from Executive flats. The dominance of 4-room flats in the rental market underscores their popularity among tenants, likely due to their balance of space and affordability.

Additional reading: HDB resale market: 1.8% price increase and 14.9% volume decrease in September 2024

Key market influences and future outlook

Several factors are contributing to the current slowdown in rental volumes across both the condo and HDB markets. Renters may be delaying their rental decisions as they wait to see how rental prices evolve amid the stabilisation in rents. Additionally, the expected influx of 7,000 new condo units by the end of 2024 is likely to increase the supply of rental properties, particularly in the OCR, which could ease market tightness and exert downward pressure on rents in suburban areas.

For the HDB market, the transition of tenants to newly completed condos and the potential upgrading of HDB owners to private homes are also influencing rental demand. Despite these factors, the HDB rental market may still find support from tenants who opt to rent public housing as a temporary solution while waiting for their new homes to be completed or during transitions between properties.

Looking ahead, the next few months will be critical in determining whether the slowdown in rental volumes represents a temporary pause or a more sustained trend. The increase in rental supply, combined with stabilising prices, could lead to a cooling in demand.

However, external factors, such as the continued demand from expatriates, foreign workers, and international students, will likely provide some support to the rental market. The extent to which rental prices stabilise and how quickly the market absorbs the increased supply will likely be the key factors that shape the rental landscape in the coming months.

What do you think about the rental market in September 2024? Share your thoughts in the comments section below or on our Facebook page.

About Ananda Bayu

Ananda has been wrangling Singapore's complex real estate trends into readable bites since 2020. She writes like she's explaining it to a friend over kopi — because who has time for jargon? When off the clock, she’s probably doom-scrolling through cat memes on X, convincing herself it's the highest tier of "creative inspiration".

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Leave a comment