Resale flats are back in vogue.

Since the government’s implementation of property cooling measures, cash-over-valuation (COV) has been effectively eradicated, and property buyers are flocking back to purchasing resale flats once more.

But while COVs are out, it doesn’t automatically mean a resale flat is the best bet for you financially; you still need to make sure that your purchase is one that you can afford on your budget.

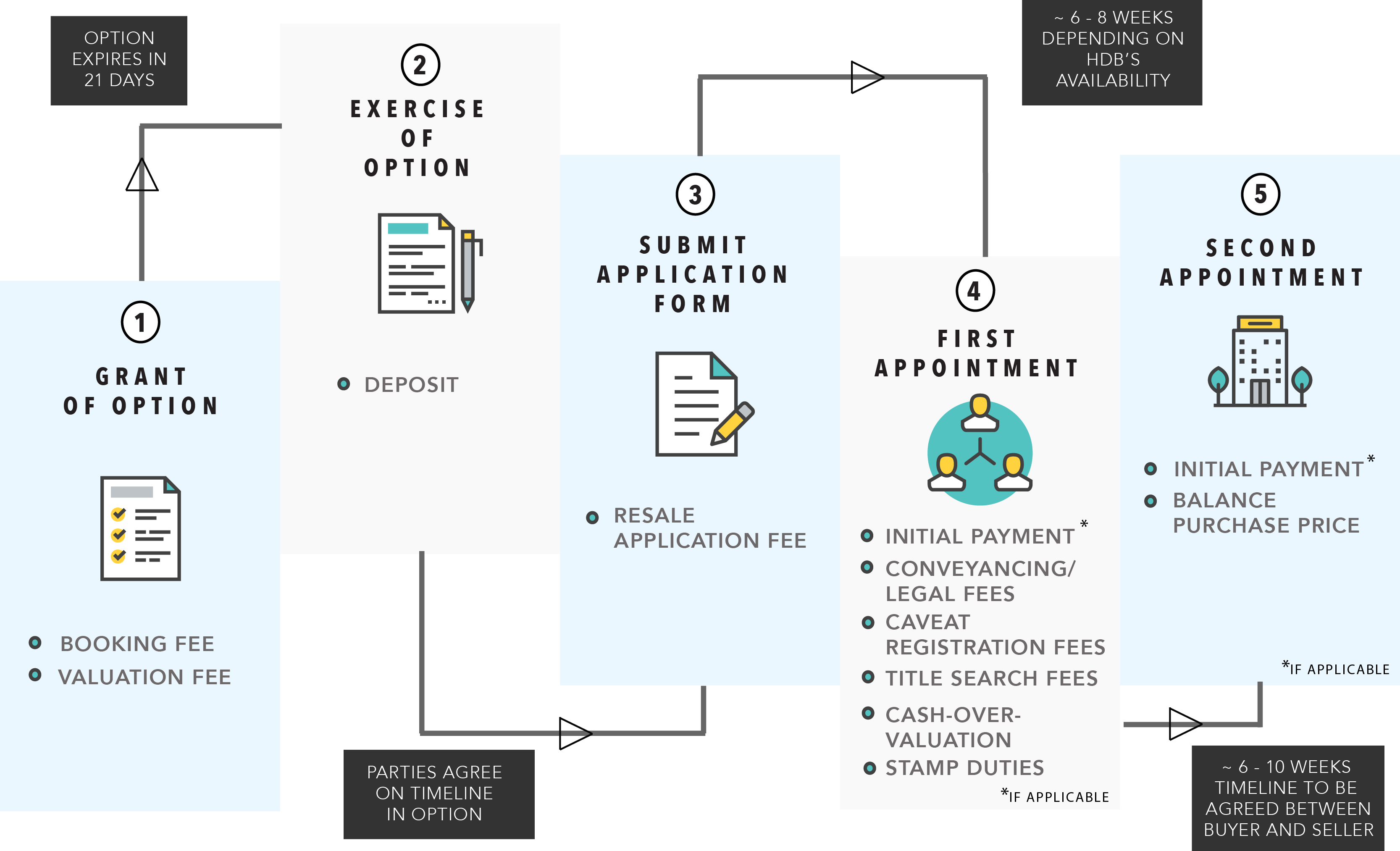

To help you determine that, we’ve come up with a little cheat sheet so you can see what your financial obligations will be like when buying a resale flat, and when they kick in!

| Fee payable / stage purchase | Approximate timeframe | % purchase price / fees payable |

Source of funds |

|

Grant of option (Booking fee) |

– | $1 – $1,000 |

Cash |

|

Valuation fee |

– | 1 / 2 – room flat

$140.40 3 – room and bigger $199.25 |

Credit card (If via e-resale service) or GIRO (If via estate agent toolkit) |

|

Deposit |

Within 21 days* |

$4,000 – $4,999** |

Cash |

| Application fee | Within timeline agreed between parties | 1 / 2 – room flat $40 3– room and bigger$80 |

Credit card (If via e-resale service) or GIRO (If via estate agent toolkit) |

|

Initial payment (HDB loan) + using CPF to pay for initial payment |

~ 6 – 8 weeks

(at first appointment) |

10% of purchase price | CPF |

|

Initial payment (if taking bank loan) |

~ 6 – 8 weeks

(at first appointment)^ |

20% of purchase price^^ | 5% cash + 15% CPF/cash |

|

Stamp duty on option |

– | 1st $180,000 1% 2nd $180,000 2% Remainder of purchase price 3% |

Cash/CPF |

|

Stamp duty on mortgage |

– | 0.4% of loan∈ |

Cash/CPF |

|

Additional Buyer’s Stamp Duty (ABSD)Ω |

– | 5% of purchase price OR market valuation (whichever is higher) |

Cash/CPF |

| Conveyancing legal fees | – | Conveyancing legal feesΨ

1ST $30,000 2ND $30,000 Remainder of purchase price |

Cash/CPF |

| Legal fees† ~ $2,300 |

Cash/CPF |

||

| Caveat registration fees | – | Buyer’s caveat†† $64.45 Mortgagee’s caveat‡ $64.45 |

Cash/CPF |

| Registration feesΦ | – | Lease in-escrow $38.30Mortgage in-escrow $38.30 |

Cash/CPF |

| Title search fees» | – | $10.40 |

Cash/CPF |

| Cash-over-valuation | – | Valuation less purchase price | Cash |

| Initial payment (HDB loan + cash to make inital payment) | ~ 6 – 10 weeks | 10% of purchase price | Cash |

| Home protection scheme« | – | Dependant on gender, loan amount, type and duration.

Calculator available here |

Cash/CPF |

| Fire insurance | – | ~ $1.50 – $7.50 for 5 years | Cheque |

|

Balance of purchase price |

– | Purchase price less initial payment, option fee & deposit

|

Loan / CPF/ Cash |

* Or within timeline agreed in Option

** Booking fee + deposit cannot exceed $5,000 in total

^ Payment timing dependant on bank’s payment schedule

^^ Based on an 80% loan ceiling

∈ Subject to maximum cap of $500

Ω Only applicable to Singapore Permanent Resident households

Ψ Payable if HDB solicitors are acting for you. Same rate applies for both transfer and mortgage. Subject to GST.

† Payable if external solicitors are acting for you

†† Payable if HDB solicitors are acting for you

‡ Payable only if you take a loan from HDB

Φ Payable if you take a loan from HDB, and are using HDB’s solicitors to act for you

» Does not apply if you take a bank loan and have external solicitors act for you

« Payable only if you intend to use your CPF to service your monthly loans

HDB Resale Flat (HDB Loan) (Illustration)

Let’s take the example of newlywed couple David and Anna, who are both Singapore Citizens in their early 20s.

They are first-timer applicants with a combined income of $6,000/month looking to purchase a 3-Room Resale Flat, with a purchase price of $400,000. They have $20,000 in their CPF accounts, and find that they qualify for a Family Grant totaling $30,000.

According to the Valuation Report, the flat is valued at $400,000, so no COV is payable.

They will be financing their purchase with an HDB Loan which will cover up to 90% of the purchase price, for a term of 25 years, and have been asked to pay $1000 as a Booking Fee for the Option. They also intend to service their loan instalments using their CPF.

|

Fee payable / Stage purchase |

% purchase price / fees payable | Source of funds |

|

Grant of option (Booking fee) |

$1,000 |

Cash |

|

Valuation fee |

$199.25 |

Credit card |

| Deposit | $4,000 |

Cash |

|

Application fee |

$80 |

Credit card |

| Initial payment | $40,000 |

CPF |

|

Stamp duty on option |

$6,600 | Cash/CPF |

|

Stamp duty on mortgage |

$500 |

Cash/CPF |

|

Conveyancing fees |

$1,009.01

($405.53 + $603.48) |

Cash/CPF |

|

Lease in-escrow registration fees |

$38.30 |

Cash/CPF |

|

Mortgage in-escrow registration fees |

$38.30 |

Cash/CPF |

|

Caveat registration fees |

$128.90 |

Cash/CPF |

|

Title search fees |

$10.40 |

Cash/CPF |

| Home protection scheme | $241.56

(Yearly premium) |

Cash/CPF |

| Fire insurance | $4.50 |

Cheque |

|

Balance of purchase price |

$355,000 |

Loan/CPF/Cash |

|

Total |

$408,850.22 |

Assuming they wish to utilise the entire HDB loan, here’s what their financial obligation would look like:

HDB Loan : $355,000

CPF : $50,000

Cash : $3,850.22 ($408, 850.22 – $50,000 – $355,000)

*HDB loan will wipe out CPF Savings first, then finance the balance

HDB Resale Flat (Bank Loan) (Illustration)

Now let’s see how the finances work out if David and Anna decide to get a loan from a bank instead.

Since this is their first and only loan, they would be entitled to a bank loan covering 80 percent of their total purchase price. They have also decided to go with external lawyers to help them through the transaction, and will be paying them $2500 for their services.

|

Fee payable / Stage purchase |

% purchase price / fees payable |

Source of funds |

|

Grant of option (Booking fee) |

$1,000 |

Cash |

|

Valuation fee |

$199.25 |

Credit card |

|

Deposit |

$4,000 |

Cash |

|

Application fee |

$80 |

Credit card |

|

Initial payment |

$20,000 (Cash) + $45,000(CPF)

+ $15,000 (Cash) |

5% cash + 15% CPF / Cash |

|

Stamp duty on option

|

$6,600 |

Cash |

|

Stamp duty on mortgage |

$500 |

Cash |

|

Legal fees |

$2,500 |

Cash |

|

Home protection scheme |

$241.56

(Yearly premium) |

Cash/CPF |

|

Balance of purchase price |

$315,000 |

Loan |

|

Total |

$410,120.81 |

Here’s what their financial obligation would look like:

Bank Loan : $315,000

CPF : $50,000

Cash : $45,120.81 ($410,120.81 – $315,000 – $50,000)

About Zareen B.

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Leave a comment