I know some of you guys will be triggered when reading this article, but you need to hear this.

Don’t do it.

Don’t buy that $900,000 HDB flat.

It will be a disaster for you.

Okay, first of all, imma assume you are young and middle class, trying to buy the most expensive home you can afford.

So you just started earning quite a bit of money and you no longer qualify for BTO because you busted the income ceiling, earning more than a combined $14,000 a month.

You can’t afford a condo yet, so you’re looking for the next best thing.

But this $900,000 HDB flat? It is the worst of both worlds.

You should just either buy a more affordable HDB flat, or go straight to a condo. Let me get to it.

Argument 1: If you want to “invest”, there are a lot of better options

Let’s agree on one thing. Money INVESTED in your 20s has the potential to grow more than money invested in your 30s and 40s.

Agree? Yes. Okay, let’s move on.

HDB flats are not investments. They are meant to be affordable public housing. And they will STAY affordable, so give up on capital appreciation.

First, you need to consider that at such a high price, the seller may be asking for more than the actual HDB valuation of the flat (however that turns out; you have to agree on the price and secure the Option to Purchase, before HDB gives you the valuation).

The excess amount over the valuation – or Cash Over Valuation (COV) – has to be paid from your pocket, as it’s not covered by your bank loan. This can result in a bigger initial cash outlay than you planned.

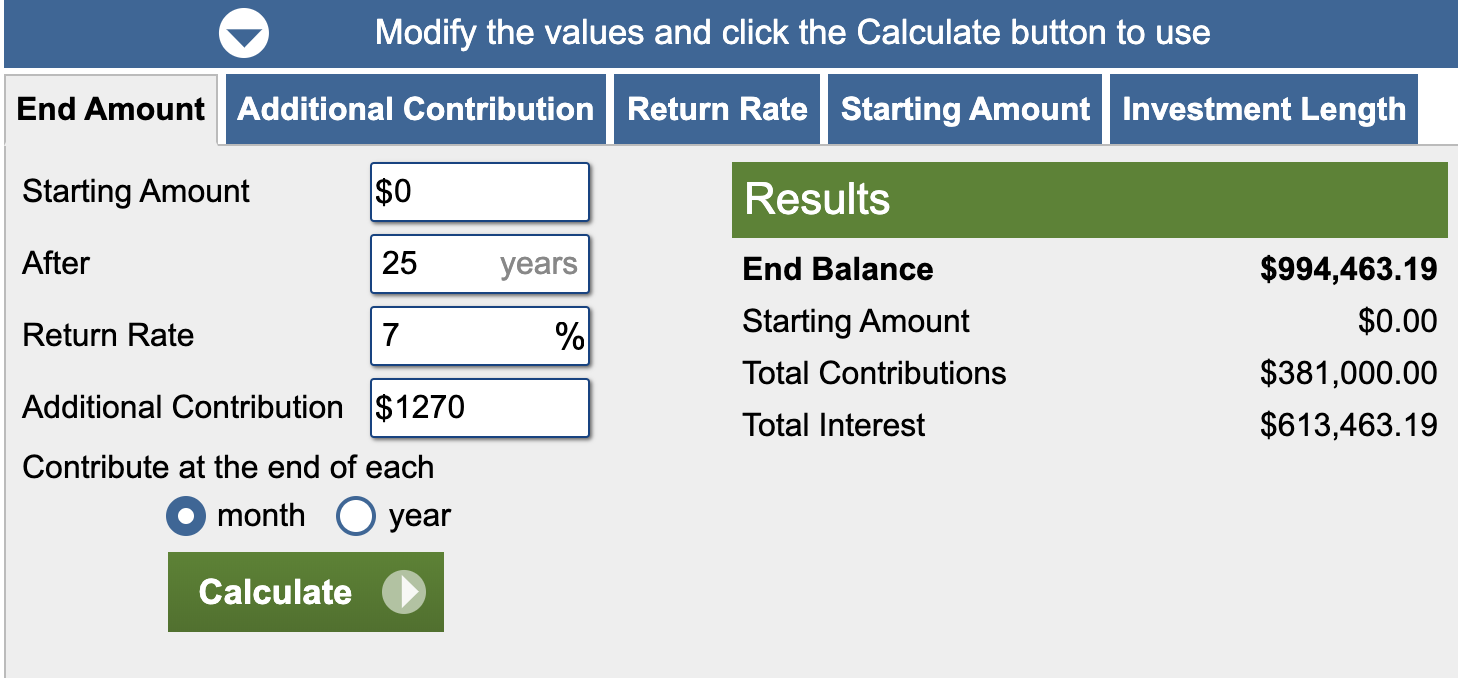

Second, let’s pretend you don’t pay any COV (which is doubtful at such a high price). Let’s say you get the maximum bank loan, covering 75 per cent of the $900,000. The loan is for 25 years, at around two per cent per annum.

This would come to a monthly repayment of over $2,860.

By contrast, a $500,000 flat – using the same loan package – is only around $1,590 per month.

Why is that a big deal?

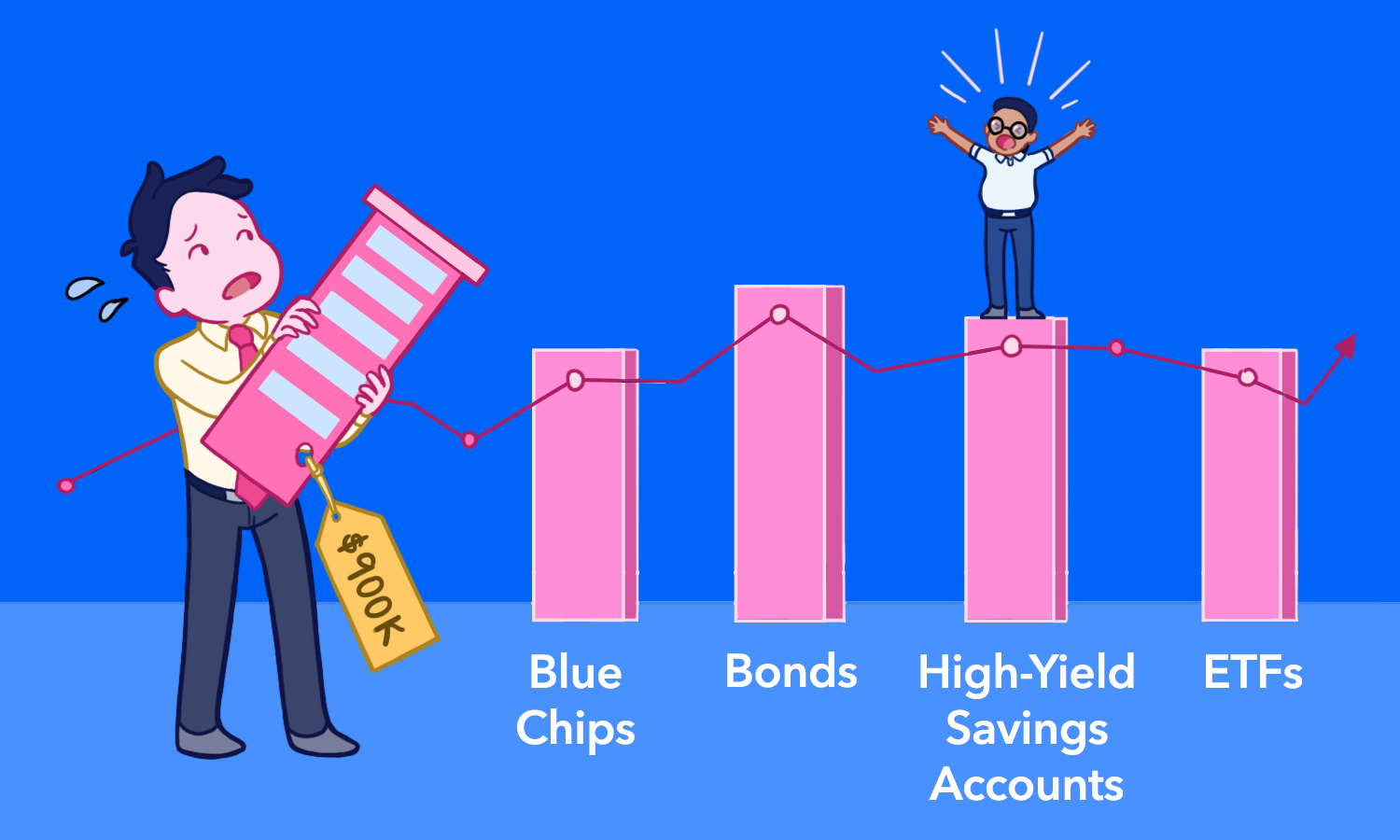

Because the difference in monthly payment is an opportunity cost of $1,270 a month, $15,240 a year, or $76,200 over five years, or $381,000 over 25 years.

Assume you put that in the stock market to accumulate, that’s almost $1,000,000 over 25 years.

If you’re a couple that just BUSTED the ceiling earning a combined $14,000 a month, isn’t that a lot of money?

Let’s face it – $14,000 a month isn’t a small amount, but it isn’t exactly a lot either given the way how Singaporeans tend to spend their money.

Given our rising costs of living, wouldn’t you want to optimise the way you spend your money and give your loved ones the best opportunity to succeed?

This is money that could be used to build an emergency fund, invested to create passive income, bring up children or look after elderly parents. You could even use this money to bring retirement forward at least 10 years, reducing the stress you face from work.

“But I will confirm earn more in the future to afford it, so $900,000 is okay”

Are you sure though? Look around you. No one is immune from retrenchments. Not even the young PMETs in their 20s and 30s. AI and cheaper labour from other countries are threatening our livelihoods. Are you even confident of keeping your job for the next 10 years?

Even if you believe you CAN earn more in the future, you can’t justify a bad purchase with “I can afford it.”

And really, if you believe you can earn more in the future, then why not you buy a condo then?

To simplify:

| $900,000 flat | You can live in it | Probably won’t appreciate faster than a condo (which you can buy at that price), or an ETF / REIT |

| $400,000 flat | You can live in it | Frees up another $500,000 for investment, which will probably appreciate faster than an HDB flat |

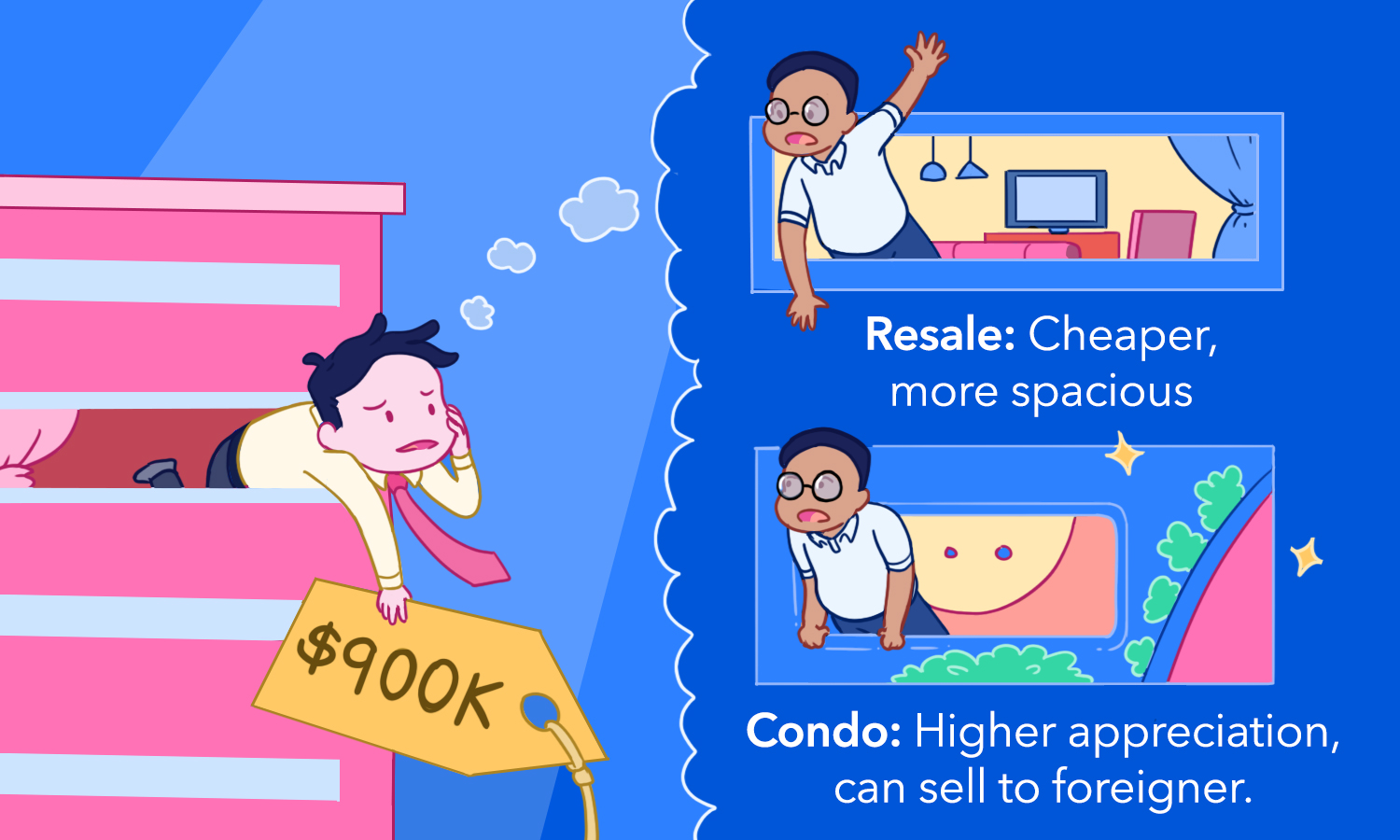

Argument 2: If you want to do own stay, there are a lot better options

$900,000 for a HDB flat? Really?

If you spending that much, why not just go and get condos like this, this and this instead? Sure, the spaces are smaller but there will be a chance for capital appreciation. Or why not just buy a new launch then?

If you need space, why not go for an older (<50 years lease) HDB flat in a central location? Sure, the lease might be shorter, but these can be had from as low as $250,000 for a three-room flat. Queenstown, Dakota and Mountbatten come to mind. Or $500,000 for a four-room HDB.

If the lease bothers you, then why not live slightly further away from the city? Sure, you might need to GRAB or HAIL a car every day for the next 20 years while Singapore disperses its CBD throughout the island.

But even IF you spend $40 on GRAB every day for the next 20 years, that’s only $292,000. Still cheaper than a $900,000 flat.

Argument 3: Who is going to buy your home when you want to sell?

When you buy a HDB, you are limiting your buyer pool to the Singaporean market. No foreigner can buy your HDB. Especially the people who can afford $900,000 homes.

Let’s look at your prospective buyer pool.

- Singapore has a decreasing population, falling below the replacement rate. About 39,000 babies were born in 2018.

- In that same year, new citizens in Singapore totalled 22,076.

- Think very carefully about who these new citizens are. Singapore is trying to bring in people with valuable skills and knowledge – think whether or not they will purchase your $900,000 HDB. Or straight to a $1.5 million (or more) condo.

- Singapore has an aging population – lots of the people around today, won’t be around in 10, 20 years.

Conclusion

The buyer pool is shrinking. The ownstay options are better. The investment options are better.

If you are buying a $900,000 flat, you better have damn good reasons to, such as renting it out and be a stay-in landlord.

About Ruiming He

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Hi there. Your article is so sour, it made my vinegar blush.

Other people can afford. Like the flat. They can buy whatever they want. It makes sense because they are living in something that they want.

You do not call people’s decision senseless bu throwing some calculations.

Calculations cannot calculate why people like you can be so jealous for example.

Be gracious.

triGgEreD

Wise ppls think alike. The only good thing about HDB is creditor free when in bankrupt and loan from bank

Hi there. Your comment is so salty, it made my soya sauce blush.

The article was never about affordability. The writer can write whatever he wants. He made a good logical point about the opportunity costs of buying the 900,000 flat, backed by facts not insults.

You do not make personal attacks about his state of mind/personality because he probably caused you some cognitive dissonance about your purchase.

The Singapore education system forces comprehension as part of English language education. But calculations also cannot calculate why people like you fail to comprehend meanings of articles like the above for example.

Be gracious.

Ok Bimmer driver we jealous of your SES.

It must be 900k hdb high.

But maybe not 900k condo high.

This fellow is pushing people to buy condo. If a $900k HDB flat, sure have good size, good location,.nearby facilities and a good view.

You are half right. Buy a condo or buy a more affordable HDB.

Agree. If the oil prices fall, economy goes into recession and the proud owners of $900k HDB cannot continue to service their mortgages, it may be worth to pick up such a place at half price.

Totally agree. I don’t see how a 99 year condo would not depreciate like Hdb. The perception is that condo value would only go up but hdb would go down

This is a good article .Been trying to put in the heads of my pool of acquaintances.Yes ,900k for a more 25 year old hdb is dumb even if you’re millionaire

Well done author ?

The best article I ever read. It will not be logical for Egoistic SG people, who have NO idea of financial literacy.

Manage your decisions on your finances prudently esp with overpaying for a property that depreciates with time. The high probability of selling your unit depends on key factors like location, surrounding amenities , ease of transportation , etc , buyers factor in all this consideration and personal criterias before deciding . Dwellings in close proximity of all this urban amenities make for good rental as well. My Hdb unit is just next to Starbucks and Lot 1 and everyday i receive flyers for rentals and sale . Just my two cents worth

Thank you and appreciate very much for the info. It is indeed very helpful 🙂

Too many big assumptions for eg

Condo gives opportunity for appreciation but ignoring the fact at the part of property cycle risk of downside is much bigger

Assume 7% return i worked in fund mgt and I have to say its no easy feat for avg retailer

Actually on the contrary with current launches despeciable shoebox sizes – who will want to buy from you if you buy – HDB flat has ample space for family planning