Once in a while, 99.co picks a piece of property jargon to explain it. Today, we look at the Buyer’s Stamp Duty (BSD), and what it does to your wallet when you buy a house.

The BSD is a stamp duty levied on any property purchase in Singapore, whether it’s residential. So it applies regardless of whether you’re buying an HDB flat, private property, or commercial property. BSD is always based on the higher of your property purchase price or valuation.

The Buyer’s Stamp Duty (BSD) in Singapore is a crucial aspect of the property purchasing process, impacting both residential and non-residential property transactions. Understanding BSD is vital for potential buyers as it represents an additional cost that can significantly affect the overall affordability of a property. For residential properties, the BSD is calculated on a progressive scale based on the purchase price or market value, whichever is higher. This system ensures a fair distribution of tax based on property value, where more expensive properties incur higher duty rates.

Buyer’s Stamp Duty (BSD) for residential properties

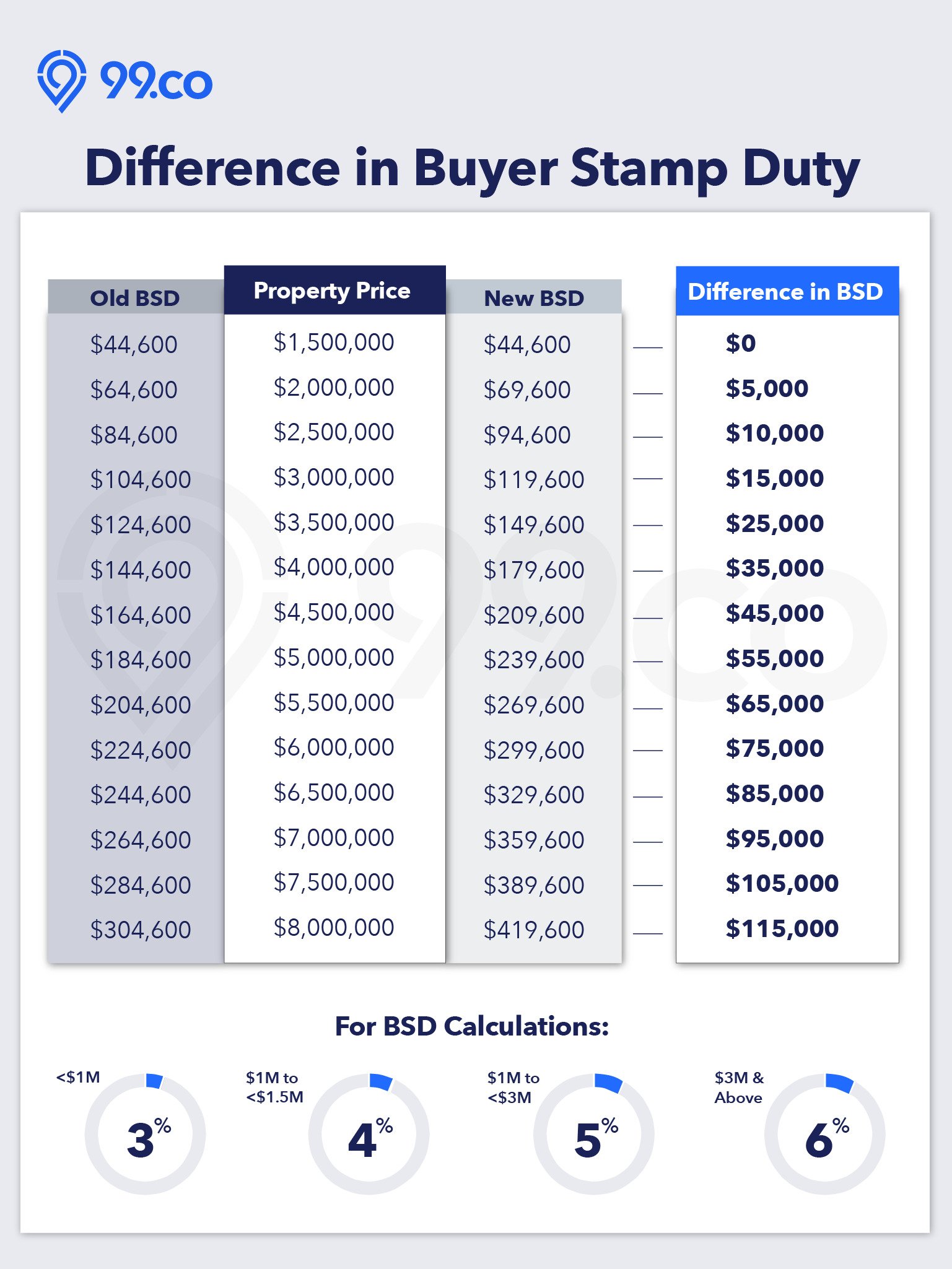

With the effect from 15 February 2023, the Buyer’s Stamp Duty (BSD) is calculated:

| Property price or market value, whichever is higher | BSD rate |

| First S$180,000 | 1% |

| Next S$180,000 | 2% |

| Next S$640,000 | 3% |

| Next S$500,000 | 4% |

| Next S$1.5 million | 5% |

| Remaining amount | 6% |

This means that you’ll need to pay a higher BSD if the new house is priced or valued above S$1.5 million.

Condos for sale

For example, say your Sale and Purchase Agreement states a price of S$3 million for your new home, but the valuation report places your property at S$2.9 million. In such a situation, the BSD would be applied on the S$3 million purchase price, as it’s the higher number.

Here’s what you would pay for the BSD:

| Purchase price of the house | |

| 1% of the first S$180,000 | S$1,800 |

| 2% of the next S$180,000 | S$3,600 |

| 3% of the next S$640,000 | S$19,200 |

| 4% of the next S$500,000 | S$20,000 |

| 5% of the remaining S$1.5m | S$75,000 |

| Total BSD for residential property | S$119,600 |

A faster way to calculate BSD for properties below S$1 million

If the property in question is S$1 million or fewer, we usually use this formula instead:

(3% of price or valuation) – S$5,400 = BSD amount

Let’s say you’re buying an HDB flat for S$600,000. The BSD to pay will be:

(3% of S$600,000) – S$5,400 = S$12,600

The result will be the same as the previous formula; it’s just quicker to work out.

HDB flats for sale

Alternatively, use 99.co’s stamp duty calculator to calculate how much BSD to pay!

What’s the Buyer’s Stamp Duty (BSD) for non-residential properties?

The BSD rate is lower for non-residential properties. Here’s the rate with effect from 15 February 2023:

| Property price or market value, whichever is higher | BSD rate |

| First S$180,000 | 1% |

| Next S$180,000 | 2% |

| Next S$640,000 | 3% |

| Next S$500,000 | 4% |

| Remaining amount | 5% |

For example, say you are purchasing a commercial property for S$2.5 million, with a similar valuation. You would then pay:

| Purchase price of property | |

| 1% of the first S$180,000 | S$1,800 |

| 2% of the next S$180,000 | S$3,600 |

| 3% of the next S$640,000 | S$19,200 |

| 4% of the next S$500,000 | S$20,000 |

| 5% of the remaining S$1m | S$50,000 |

| Total BSD for non-residential property | S$94,600 |

Hold on, what happens if my property has both residential and non-residential uses?

This sometimes happens with, say, HDB shops that have living quarters upstairs. It might also happen if part of your unit is approved for non-residential use, for a limited time (e.g. the downstairs portion is approved for use as a daycare centre, but only for the next few years).

In the first scenario, such as a shop with housing upstairs, you would pay the residential BSD rate on the value of the residential portion. You would then pay the non-residential rate on the value of the commercial portion. This can get annoyingly complicated, so make sure you clarify the numbers with the property agent and valuer before you buy.

In the second scenario, where part of the property is temporarily used for non-residential purposes, you will still pay the residential rate. When in doubt, just check how the land is zoned, which you can do so on the URA master plan. If it’s zoned as residential, then you’re going to pay the residential rate – regardless of what commercial use is temporarily going on.

For non-residential properties, the BSD rates are slightly different, reflecting the diverse nature of property transactions in Singapore. These distinctions are important for buyers to consider, especially when purchasing mixed-use properties. In such cases, different portions of the property may attract different BSD rates, adding a layer of complexity to the calculation. Timely payment of BSD is critical to avoid penalties, and understanding the nuances of BSD calculation is essential for making informed financial decisions in property investments.

When must you pay the Buyer’s Stamp Duty?

It must be paid within 14 days after signing the contract or agreement.

If the document was signed overseas, the time limit was extended to 30 days after the agreement was received in Singapore. To be safe, ensure your law firm (the firm handling the conveyancing) is informed when you’ll be seeking the 30-day period.

If the payment is delayed for less than three months, you’ll be fined either S$10 or the value of the BSD, whichever is higher (Hint: it won’t be S$10).

If the payment is delayed for over three months, you’ll be fined either S$25, or four times the BSD payable, whichever is higher (Bigger hint: it won’t be S$25, and you really don’t want to be this late).

What’s the relationship between BSD and ABSD?

The Additional Buyer’s Stamp Duty (ABSD) is covered here. As the name implies, the ABSD is payable on top of the BSD.

So if you’re a Singapore Citizen buying a second property, for example, you would pay both the normal BSD on the property, plus the 17% ABSD.

Note that, while you can apply for ABSD remission, this doesn’t apply to BSD. You cannot get your BSD money back, regardless of whether you’re buying your first or subsequent property.

Shopping around for a higher valuation? Note the corresponding effect between LTV and BSD

We’ve previously explained the loan-to-value ratio (LTV): it determines how much you can borrow to buy a house.

Many home buyers will find a bank that takes the highest valuation of the property, as they want to borrow more. However, note that LTV applies to the lower of the property price or value. The BSD applies to the higher of the property price or value.

This means that a higher valuation will cause you being able to borrow more for your house. But it will also result in you paying a higher stamp duty. Bear this in mind before actively looking for a higher valuation.

What bit of property jargon confuses you? Let us know in the comments section below.

About Ryan Ong

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Leave a comment