In spite of the belief that speculative behaviour is rare in the real estate market due to the considerable investment costs involved, both recent and current market situations have proven otherwise. In this article, we examine the causes of bubble behaviour and the present situation in Asia.

As put forth by Russian-born American philosopher and novelist, Ayn Rand, “There’s no way to make the irrational work”. In the context of the recent 2007-2009 U.S. property crisis, this saying definitely rings true. Factors such as massive subprime lending, gross borrowing driven by low-interest rates and widespread speculative behaviour in the U.S. property market played a part in creating an unsustainable housing bubble. The subsequent collapse of the bubble opened the door to the 2007-2009 U.S. financial crisis, as well as the 2008-2012 Economic Slowdown – the latter of which continues to shake economies worldwide to date.

The big trigger

Generally speaking, speculative bubbles occur when buyers inflate the demand and price of an asset (or property, in this case) due to unrealistic hopes or estimations of future appreciation in the short-term. Eventually, property prices skyrocket due to the influx of demand from speculators hoping to make a quick profit. The boom then comes to a catastrophic end when the rate of price increase slows down after market demand stagnates or is exhausted – this is typically followed by a sharp fall in actual asset prices and a rise in asset supply as investors exit the market.

In the case of the U.S. property crisis, a number of systemic and socio-psychological factors have been linked to the intensification of demand and speculation in the real estate market. Listed below are some of these causal factors:

1. Low Federal Reserve interest rates

One systemic factor would be the low Federal Reserve interest rates of the early 2000’s which helped fund risky investments via easy credit. Buyers were encouraged to take up mortgages and purchase homes which were perceived as profitable investments prior to the market’s collapse.

However, when interest rates were raised in the period of 2004-2006, this resulted in massive defaults on mortgages as previously affordable homes became too costly for their owners. The rise in interest rates also caused a lessening of demand which further propelled the downwards trend of U.S. property prices.

2. Widespread subprime lending

Yet another exacerbating factor present was the prevalence of subprime lending by U.S. banks – a practice which involves providing mortgages to individuals who are unable to reliably pay back their loans.

Following the overall decline in property value across the U.S. in 2007, many chronic debtors begun to default on their housing loans which contributed to the rising number of foreclosure cases. As a result, the situation became untenable following massive additions of devalued properties to an already high supply of unoccupied homes.

3. The role of psychological factors

The build-up of the U.S. bubble can also be partially attributed to quirks in human psychology. In a paper published in 2011, Yale professor, Nicholas C. Barberis, examines two mechanisms which possibly drove investor behaviour – namely the over-extrapolation of past price changes and belief manipulation.

The former involves an over-reliance on past returns and personal experiences to predict market futures, which explains overconfident decisions on the part of investors.

As for belief manipulation, it concerns the alteration of personal beliefs when one experiences cognitive dissonance. This theory implies that an individual would be more likely to search for plausible-sounding arguments to justify an uncomfortable course of action, as opposed to examining actual circumstances or factors. In turn, this provides a plausible explanation as to why investors go through with unsafe investments, despite the mental and emotional discomfort felt when committing to risky decisions in a dangerous environment (or an overheating market, in this case).

How frothy is the Asian property market? Cooling measures and their effectiveness.

While U.S. property prices have since recovered from the 2007-2009 shock, the lessons learnt are definitely applicable within an Asian context. Shortly after the bursting of the U.S. property bubble, a number of Asian economies found themselves facing a looming real estate crisis of their own.

Between 2007- 2010, prosperous nations such as Singapore, Mainland China and Hong Kong, saw a rapid growth in local property prices following the implementation of monetary policies which sought to enhance recovery through economic stimulation. These measures include lowering central bank interest rates to encourage spending as well as loosening mortgage requirements, both of which contributed to increased activity in local real estate markets.

However, things were set to change as Asian governments stepped in with cooling measures in anticipation of skyrocketing prices.

For instance, in Singapore, a series of macroprudential measures were implemented from 2009 onwards, in order to reduce the systemic risk of the nation’s financial system as well as the real estate market. These precautions consist of eight rounds of temporary cooling measures which range from the imposition of stamp duties to the tightening of housing loan requirements as well as purchasing restrictions on both locals and Permanent Residents (PRs) alike.

Likewise, both China and Hong Kong saw the execution of similar cooling policies. For mainland China, an increase in the minimum down-payment for second homes was implemented in 2010; a limit on home ownership was also put in place at the same time, with each household being able to own up to a maximum of two properties.

Meanwhile, the Hong Kong government chose to execute a series of steps to restrict the borrowing of housing loans instead, with debt limitations placed on all forms of residential properties. For example, all mortgages have a loan-to-value (LTV) cap of 40 to 70 per cent placed on them. The cap amount is also subject to factors such as the value of the mortgaged property and the borrower’s source of income. Moves to increase the available supply of homes in the property market have also been announced, with an estimated 14,600 new units to be added yearly to meet local needs.

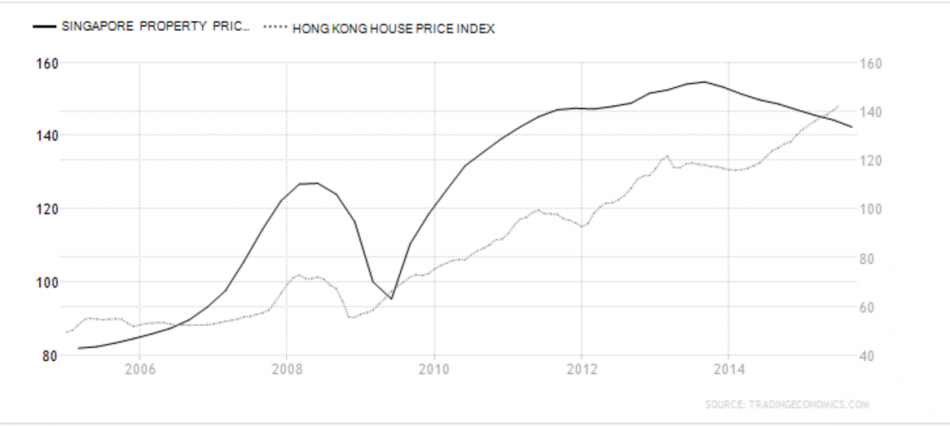

Although these policies have been effective in curbing speculative attempts in their respective countries, the full effectiveness of these cooling measures remains to be seen. This view applies strongly to both the Hong Kong and Singapore property markets as prices continue to climb in recent years, even with the application of the above-mentioned schemes and restrictions. Therefore, it is safe to say that prudence is still of utmost importance when choosing to invest in these property markets.

If you enjoyed this article, you might be interested inThe hidden cost of en-bloc fever andIs your HDB flat an asset or liability?.

Find the home of your dreams today at Singapore’s largest property portal, 99.co!

About 99.co

We are a property search engine with the overarching goal of building a more transparent and efficient property market. We are working towards that future by empowering people with the tools and information needed to find a place to live in the best way possible.

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Leave a comment