Healthcare in Singapore is not cheap, but Medisave is here to lighten the load. If you’re a Singapore Citizen (SC) or Permanent Resident (PR), you’ve probably noticed a chunk of your salary going into your CPF Medisave account each month. But what exactly is Medisave, how does it work, and how can you use it effectively for your healthcare needs? This essential guide to Medisave will break it all down for you.

Table of contents

What is Medisave?

Medisave is a compulsory healthcare savings scheme under the Central Provident Fund (CPF) that helps Singaporeans pay for medical expenses. A portion of your income is automatically set aside in your Medisave account, so you have funds available when you need to pay for hospitalisation, outpatient treatments, health screenings, or even insurance premiums. Unlike regular savings, Medisave funds grow over time with interest, making it a sustainable way to cover medical costs.

How much should I pay for CPF?

The amount you contribute to CPF depends on your age and income level. Here’s the CPF contribution rate in 2025:

| Age of employee | Employer contribution | Employee contribution | Total contribution rate |

| Up to 55 years old | 17% | 20% | 37% |

| 55 to 60 years old | 15.5% (+0.5%) | 17% (+1%) | 32.5% |

| 60 to 65 years old | 12% (+0.5%) | 11.5% (+1%) | 23.5% |

| 65 to 70 years old | 9% | 7.5% (+1%) | 16.5% |

| Above 70 years old | 7.5% | 5% | 12.5% |

How much of CPF goes into my Medisave account?

The older you are, the higher your Medisave allocation is. The CPF allocation rate for Medisave in 2025 is as follows:

| Age of employee | Medisave allocation |

| Up to 35 years old | 0.2162 |

| 35 to 45 years old | 0.2432 |

| 45 to 50 years old | 0.2702 |

| 50 to 55 years old | 0.2837 |

| 55 to 60 years old | 0.3230 |

| 60 to 65 years old | 0.4468 |

| 65 to 70 years old | 0.6363 |

| Above 70 years old | 0.84 |

For example, if the CPF contribution of a 57-year-old is S$100, the allocation that goes to their Medisave account is S$32.30 (S$100 x 0.323).

Additionally, those nearing retirement may consider voluntary Medisave top-ups to maintain sufficient funds for future medical needs. CPF members can benefit from GST Vouchers – Medisave top-ups to supplement their savings.

Note: Medisave contribution differs for self-employed persons. You can use the self-employed Medisave contribution calculator to see how much you should pay for your Medisave.

How much balance can I have in my Medisave account?

As we mentioned before, Medisave savings earn interest. It helps your balance grow over time as you grow older. The current interest rate for Medisave in 2025 is 4% per annum, and it is reviewed quarterly by CPF. This rate is higher than most regular bank savings accounts, making Medisave an effective long-term healthcare savings tool.

However, the maximum amount you can have in your Medisave account is based on the Basic Healthcare Sum (BHS). For CPF members aged below 65 in 2025, the prevailing BHS is S$75,500 and will be adjusted yearly. Your BHS is fixed once you turn 65, hence the yearly adjustments will no longer apply.

Any contribution beyond your BHS will be channelled to your CPF Special account or Retirement account.

What can Medisave be used for?

Medisave can be used to pay for your hospitalisation, day surgery, long-term healthcare needs, and many more. Please refer to the full list of what you can use with Medisave from the Ministry of Health’s page.

Additionally, you can also use your Medisave fund to pay for your family’s medical expenses. They can be of any nationality, except for grandparents and siblings, who must be SCs or PRs. This allows families to share medical costs and support one another during health emergencies.

Here are a few examples of how Medisave can cover your healthcare expenses:

Paying for hospitalisation

MediSave can be used to pay for hospital stays, including ward charges, daily treatment fees, surgery, and medications. The withdrawal limits vary depending on the type of treatment and duration of stay. For instance:

- General hospitalisation expenses can be claimed up to S$550 per day for the first two days and S$400 per day thereafter.

- Surgical procedures have specific withdrawal limits, ranging from S$250 to S$7,550, depending on complexity.

- Psychiatric hospitalisation is covered up to S$150 per day, capped at S$5,000 per year.

Covering outpatient treatments

Outpatient medical treatments, such as chemotherapy, dialysis, and vaccinations, can be paid for using MediSave. Patients with complex chronic conditions will be able to use up to S$700 yearly, while other patients will be able to use up to S$500.

- Chronic Disease Management Programme (CDMP): Covers conditions such as diabetes, hypertension, stroke, and asthma. Patients with two or more chronic conditions under CDMP qualify for MediSave700.

- Cancer treatment: Medisave covers chemotherapy up to S$1,200 per month and radiotherapy up to S$2,800 per session, depending on the type of therapy.

- Vaccinations: Medisave can be used for nationally recommended child and adult vaccinations, such as influenza and pneumococcal vaccines.

- Scans and diagnostics: Includes MRI, CT scans, and mammograms, subject to withdrawal limits.

Health insurance premiums

Medisave funds can be used to pay for national health insurance schemes like MediShield Life, CareShield Life, and Integrated Shield Plans. This ensures that Singaporeans can maintain health insurance coverage without needing to pay large sums upfront.

- MediShield Life premiums can be fully covered by MediSave.

- Integrated Shield Plan (IP) premiums have withdrawal limits depending on age, ranging from $300 to $900 per year.

- CareShield Life and ElderShield: Long-term care insurance premiums can be paid using Medisave.

Long-term and palliative care

For individuals with severe disabilities or those requiring long-term care, Medisave offers support through various schemes:

- Medsave care: Allows eligible individuals with severe disabilities to withdraw up to $200 per month to manage care expenses.

- Home palliative and day hospice care: There will not be any withdrawal limit if the bill is paid using the patient’s own Medisave account. However, there’s a lifetime withdrawal limit of S$2,500 if they tap on their family member’s Medisave or is a paediatric patient.

- Stay in approved IHPCS: Up to S$250 per day for general palliative care, and up to S$350 per day for specialised palliative care

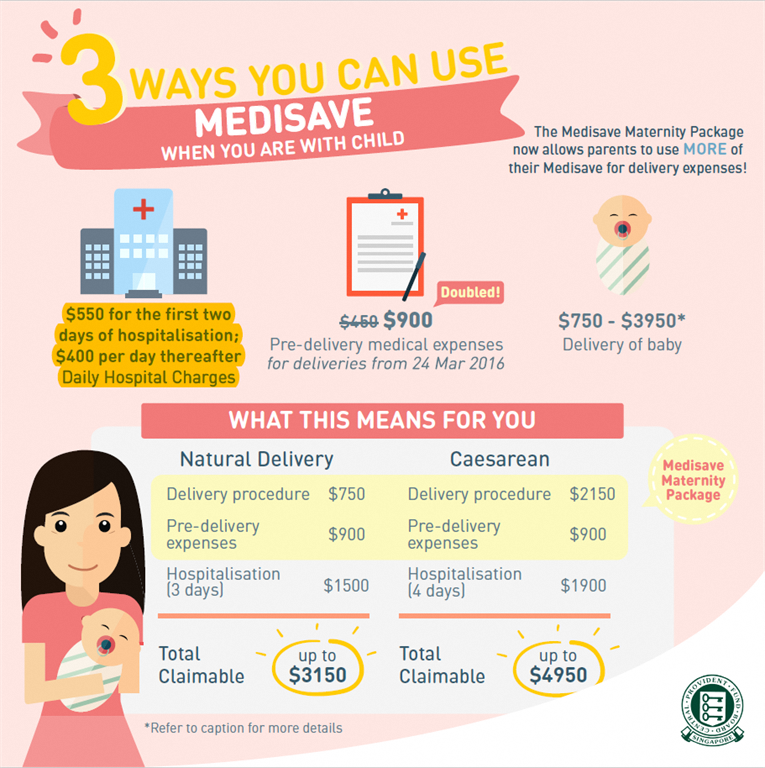

Maternity and delivery costs

Expectant mothers can use Medisave to offset costs for childbirth and related medical expenses under the Medisave Maternity Package (MMP):

- Pre-delivery expenses: Up to S$900 can be used for consultations and tests.

- Delivery costs: Withdrawals range from S$750 to S$3,950, depending on the type of delivery and hospital ward class.

- Newborn care: Medisave can also be used for neonatal intensive care and other post-delivery medical needs.

Day surgery and dental procedures

Certain surgical and dental procedures performed in outpatient settings are also covered under Medisave, subject to limits based on complexity. Examples include wisdom tooth removal, cataract surgery, and endoscopy.

What happens if your Medisave runs out?

If your Medisave funds are insufficient, you’ll have to pay the remaining medical expenses out of pocket. However, you can use your family members’ Medisave to cover your bills if they have sufficient savings. Government subsidies and financial assistance schemes like MediFund and CHAS can also help low-income Singaporeans manage healthcare costs.

About Ananda Bayu

Ananda has been wrangling Singapore's complex real estate trends into readable bites since 2020. She writes like she's explaining it to a friend over kopi — because who has time for jargon? When off the clock, she’s probably doom-scrolling through cat memes on X, convincing herself it's the highest tier of "creative inspiration".

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Leave a comment