If you are reading this, chances are you are probably relying on — or intending to rely on — your Central Provident Fund (CPF) to pay the monthly mortgage instalments for your property. However, there is a limit on how much CPF funds you can use sometimes. To avoid the rude shock of realising you have exceeded your CPF Housing Withdrawal Limits for property (and have to pay the rest of your home loan in cash), read this article.

You will pinpoint how much of your home can be paid off with your CPF funds.

Understanding the CPF Housing Withdrawal Limits

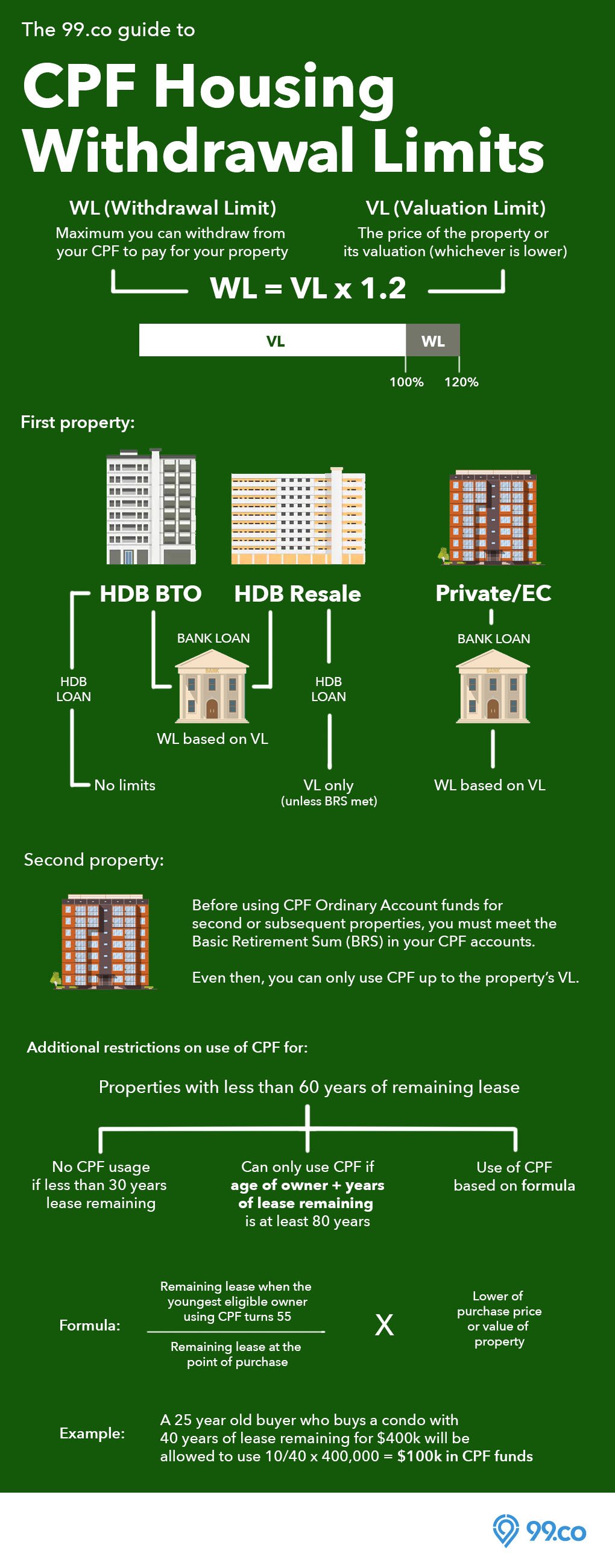

In a nutshell, the total amount of CPF funds you can use to pay off your property depends on two limits: the Valuation Limit (VL) and the Withdrawal Limit (WL).

Let’s take a second to define these: the VL refers to the purchase price or the value of the property at the time of purchase (whichever is lower). The WL refers to the maximum CPF you can put towards the property, and this is currently set as 120% of the VL.

Found the infographic useful? Let’s go into greater detail:

Note that your CPF savings can only be used if the property you are purchasing is freehold or has a remaining lease of over 20 years, with enough leases to cover the youngest buyer until they are at least 95 years old.

If you are getting an HDB loan:

For a BTO flat

Good news! Neither the VL nor the WL applies to you, and you can use your CPF to pay off your house in full.

For a resale/DBSS flat

The VL applies to you. If you want to use your CPF savings beyond your VL, then you will have to:

- Meet the Basic Retirement Sum (BRS) in your Ordinary Account (OA) and Special Account (SA) if you are below 55, or

- Meet the BRS in your OA, SA, and Retirement Account (RA), if you’re 55 and above

Read this: What happens if your housing loan deductions reach your CPF Basic Retirement Sum (BRS)?

Detailed scenario:

Say you want to buy a resale flat with a remaining lease of 65 years. Given that the purchase price of the flat is S$500,000 and the value of the flat is S$480,000, your VL will be capped at S$480,000.

Now, calculate your monthly instalment based on your loan amount, tenure, and interest rate.

Assuming a S$100,000 down payment, a loan amount of S$400,000, a tenure of 30 years and an interest rate of 2.6%, you will pay S$1,601 each month.

With a VL that is S$480,000, you will hit the limit within 22 years and 1 month.

If you cannot meet your BRS, then you will have to switch to paying cash once this happens. If you have met your BRS, then you will continue using your CPF savings to pay your mortgage.

(For HDB loans, the WL is not applicable.)

Find out if you’ll hit your CPF Housing Withdrawal Limits with the CPF Housing Withdrawal Limits Calculator.

If you are getting a BANK loan:

As long as you are taking a bank loan, both the VL and WL apply to you, regardless of your housing type.

For a flat purchase priced at S$500k and valued at S$480k:

VL = S$480,000

WL = S$480,000 x 1.2 = S$576,000

Like the previous scenario, meet your BRS to continue to service your mortgage with your CPF savings once you go beyond your VL of $480,000.

The difference here is that once you hit your WL of S$576,000 (at the 27-year, 4-month mark for a 30-year tenure), pay cash regardless of whether you have met your BRS.

Buying a second property?

If you are buying a second property, the WL will be capped at 100% of the VL.

You can use your remaining CPA OA to fund your second property, after setting aside your BRS.

After hitting your CPF limit, the rest of your monthly mortgage needs to be paid in cash.

Buying a property with less than 60 years of remaining lease?

You can still use your CPF OA to fund such a property under certain conditions:

Scenario 1: If you have a property financed with OA savings that DO NOT cover you till you’re 95:

- You may need to set aside the relevant BRS, depending on your age.

Scenario 2: If you have a property financed with OA savings that WILL cover you till you’re 95:

- You may need to set aside the relevant FRS, depending on your age.

Scenario 3: If you DON’T have a property financed with OA savings:

The percentage of your OA payments for either of these three scenarios will be pegged to the lower purchase price or valuation price of the property.

Also, regardless of which scenario you find yourself in, the lease needs to cover the youngest buyer until they are at least 95 years old.

This is the HDB’s way of ensuring you will have a roof over your head while having enough funds for retirement.

A final word on using CPF funds to finance your property

To minimise the cash outlay for their properties, many Singaporeans will milk their CPF for all its worth. Before you do so, be mindful of whether you will hit the CPF Housing Withdrawal Limits before your loan tenure is up.

If you do, make sure you will have enough cash savings by then and have the financial means to service the rest of your loan tenure by cash. The more CPF funds you allocate to housing, the less you will have for retirement, so make sure your debt repayments do not make up most of your income.

Also, consider whether it’s worth paying your instalments via CPF, given that you face the double consequence of sacrificing the 2.5% interest rate that you would otherwise earn in your CPF Ordinary Account, plus that you will have to return accrued interest to your CPF account if you sell the property.

Read this: More people were unable to fully return their CPF monies after selling their house

Long story short, if you decide to use the bulk of your CPF funds to finance your property, make sure you have a decent cash savings and/or investment plan for your retirement.

FAQ about CPF Housing Withdrawal Limits

The CPF Housing Withdrawal Limits comprises two primary components: the Valuation Limit (VL) and the Withdrawal Limit (WL). The VL is the lower purchase price or the property’s valuation at the time of purchase. The WL is set at 120% of the VL, showing the maximum amount of CPF funds that can be used towards the property purchase.

If you are buying a Build-To-Order (BTO) flat, neither the VL nor the WL applies, and you can use your CPF funds to pay off your home. For resale or DBSS flats, the VL applies, and you can use CPF funds beyond the VL only if you meet the Basic Retirement Sum (BRS) in your CPF accounts.

When purchasing a property with a bank loan, both the VL and WL apply. Once your CPF withdrawals reach the VL, you must meet the BRS to continue using CPF funds. After your withdrawals exceed the WL, you will need to pay in cash, regardless of whether the BRS has been met.

For a second property, the WL is capped at 100% of the VL. For properties with less than 60 years remaining on the lease, CPF usage is permitted under certain conditions but requires that you set aside the BRS or Full Retirement Sum (FRS), depending on whether the property covers you until you’re 95 years old.

Before using CPF funds for property financing, consider the impact on your retirement savings because of the 2.5% interest foregone in your CPF Ordinary Account, and the requirement to repay accrued interest if you sell the property. Ensure you have sufficient cash savings or a solid investment plan for retirement, especially since using CPF funds for housing reduces the amount available for your retirement needs.

Have a question on CPF housing withdrawal limits? Ask us in the comments below!

If you found this article helpful, 99.co recommends Deciding between HDB loans and bank loans? Here’s a quick reference and 5 property financial disasters homeowners don’t realise they’re exposed to

About Elizabeth Tan

Elizabeth is a writer, a Harry Potter fanatic, and a Game Of Thrones addict.

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Leave a comment