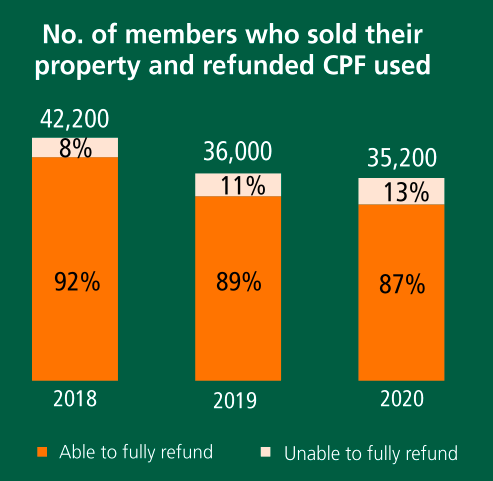

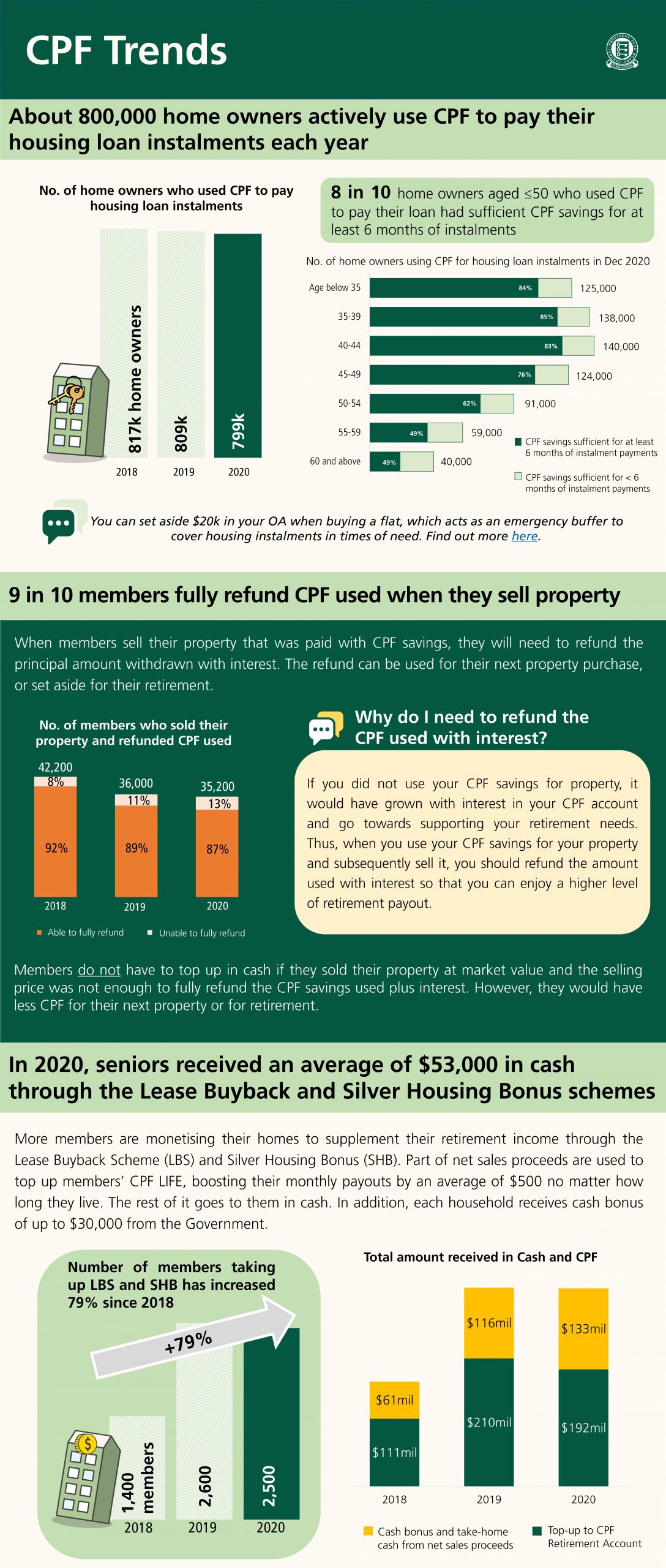

The number of people who could not fully return their CPF monies used for housing after selling their house has increased from about 3,380 in 2018, 3,960 in 2019 to 4,580 in 2020, according to a Lianhe Zaobao report yesterday. Citing a recent CPF report, this translates to an increase of 8% in 2018, 11% in 2019 to 13% in 2020.

CPF savings used have to be returned to the CPF account when the house is sold

While CPF savings are meant for retirement, members can use their CPF Ordinary Account (OA) savings for housing. This includes paying for the downpayment and monthly instalments of the home loan.

However, the caveat is that they would have to return the amount used, plus the accrued interest to their CPF savings if they sell the property. The accrued interest is the interest members would have earned if the savings were left in the OA instead.

On the other hand, if the property was sold at a market price, after paying off the outstanding loan, if the remaining balance is less than the amount of CPF savings to be returned, they would not have to top up the difference in cash.

(You’ll also have to return your CPF monies plus accrued interest to your account if you’re selling your share of the property. You can read more about it on CPF’s website here.)

Fewer people returned their CPF savings after selling their house

Within the same three-year period, there has been a decrease in the number of people returning their CPF savings after selling their house. The number has gone down from 42,200 in 2018 to 35,200 in 2020.

At the same time, more people have been unable to return their CPF savings in full after selling their house. One possible reason for this is that some may not realise how significant the accrued interest is until they have to sell their house and return it.

(One way to reduce the amount of CPF savings you have to return is to make a voluntary housing refund, which you can read more about here.)

Fewer people used their CPF savings to pay for home loan instalments

Another trend that the Zaobao report highlighted is that fewer homeowners were using their CPF savings to pay for home loan instalments. The figure has dropped from 817,000 in 2018 to 799,000 in 2020.

This means that more people are using cash to pay for their home loan instalments, which could help reduce the amount of CPF savings needed to be returned should they sell their house.

You can refer to the full CPF trends report here.

What do you think of these CPF trends? Let us know in the comments section below or on our Facebook post.

If you found this article helpful, 99.co recommends How your HDB sale proceeds might get “taken” by CPF and Negative Sale: How selling your HDB/condo could put you in instant debt.

Looking for a property? Find the home of your dreams today on Singapore’s fastest-growing property portal 99.co! If you would like to estimate the potential value of your property, check out 99.co’s Property Value Tool for free. Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

About Virginia Tanggono

Virginia covers the property news in Singapore, from record sales to profile stories on home ownership. In her free time, she occasionally searches for spoilers of movies and TV shows.

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

why you need to top up cpf in the form of accrued interest. this dont make sense. people are using cpf because they dont have money and yet need to pay for their own interest? they are not bank paying interest for themselves. this accured interest requirements has to be removed.

I opine,if the HDB owners fully paid for the HDB housing loan n are above retirement age,HDB should not charge for any accrued interest on CPF n they should be exempted.

Hope,my suggestion got airing

Thanks.

If you ever believe CPF is yours and yours only, and for retirement purposes, which was the original intent by our founding father LKY, then you can’t be more wrong! Tell me a bank that charge you interest for drawing your own money? Tell me SGD600 per month is enough for you to survive in the ever costly Singapore! It’s all a farce!!! When you go bank to cha’ge CNY money, you will get to change whenever there’s enough to meet the withdrawal. But if there’s shortage, you will be advice to come again the next day or next week. Ever why CPF cannot be withdraw in full? Think!!!

Why does HDB require us to pay the acrued interest , isn’t the cpf money our hard earned money safekeep for the purpose of buying a home..

And why are we paying interest to our money?

These is making the people fall into more debt.. is that what the government wants, that we are in debt and cannot have a quiet retirement, instead have to work even at old age to cover these debts..when the money is used for valid purpose ls and not spluring.

Government need to realise , we are their citizen not a foreigner, we should be protected from such debt. Not having to face more debts , as it is the cost of living is already high and still increasing with more gst , increase in all matters etc household bill, erp pricing,coe ,petrol tax, summons and home tax increae.. Where will find the money to have a family and save for our kids future . Even school fees are increasing.. so tell me how to retire as we grow older … Amid covid and no jobs, govrnment still require us to make these payments ..

Give us a break … We need to appreciate and care for the elder generation and let those with families to have some savings.. if this trend continues, i forsee Singapore have lesser babies and the young educated migrating to other countries to seek better future than singapore . .

Ease up on the rules n tax , and strengthen your peoples needs, give them better jobs, better opportunities, lower down on the cost of hdb housing and for resale ,ease on the tax and gst..

Not all of us are born with a silverspoon …

We are struglling day by day.. just to make sure all bills and needs are taken care.. and its getting harder everyday..

A wealthy nation doesnt mean a Happy nation.. if behind it is all the means to squeeze the people …

And not reward them for their hard work to build this nation ground up.

Please be a caring and thoughtful leader.. not someone who only commands and does not know how the people are suffering….

We need a peoples leader, someone from the Middle income or low income family to rise..

Maybe one day… I pray for out kids future..

HDB should not charge accrued interest on CPF n they should be exempted. Buying a house it’s a form of investment and there are risk involved. When people making a loss from selling a house, why HDB still further their burdens to pay off the interest again.

Dont think it is hdb that require u to pay the accrued interest. It is cpf that requires it

many people who purchased an old resale flat that left less than 60 years lease around 2012 to 2017, suffered a loss when selling their flats now.. as their flats have depreciated by 100k to 200k. so they are not able to return the CPF used.. in fact, some of them got quite a big amt of their CPF wiped out.

..the Government should stop the property trading. Speculation in HDB,…because most if these leverage to the hilt,..hoping to profit from Capital Appreciation…cash flow from rentals ( enforcement is very rare…),..

Do most simply use their talents to play life-sized Monopoly game, glorified by Property Gulus….

But the bigger picture reveals that Society, Future Generations eventually suffer…as a casualty of these Mathematical Games.

Yes/ No ?

Majority of people commenting either doesn’t know the full return terms, or are just commenting based on their own narrow thinking… Maybe writer can make it clearer about the reasons and exemptions as well.

It’s unacceptable that those Seniors who sold their home after LKY Set Age of CPF withdrawal for Retirement to PAY BACK CPF for retirement plus interest!!

It’s more likely that some percentage of People who DIES EARLY Unfortunately NEVER GOT TO SEE THEIR OWN RETIREMENT MONIES and even get to smell their Years of Blood and Sweat to save that sum!

Sometimes one wonders WHAT AGENDAS such Policy benefits those who sets the rules instead of letting these oldies enjoy their final years spending their own monies instead of being tied down!!!!!!

From Age 55 retirement extended to Age 60 THEN UP UP UP until going 70!! Goodness gracious!!! The people above 60 years old Age is a most sensitive for many low wage earners and those with little CPF monies in their retirement account!!! WHY MENTALLY TORTURE THESE PEOPLE who can’t spend their, that little monies in their retirement account!! Worse even not enough CANNOT Withdraw AT ALL from Either, OA or Medisave or what little amount in retirement account!!!

CPF should not hold those much needed monies especially the ones that have no monies even in banks!!!

BE Sensitive to THESE PEOPLE TRULY INDIVIDUALS NEEDS as their means of SURVIVAL!! RELEASE TO THEM AND PLEASE DON’T HOLD THESE MISERABLY POOR PEOPLES MONIES!!!!!!!!!!

CPF is ultimately meant for retirement, and to ensure that the future generations are not overly taxed with the burden of supporting the elderly. It isn’t meant to be your personal bank account where you can withdraw funds as and when you want. If you choose to use cpf savings for your housing, the condition is that you are able to sufficiently provide for yourself and would be able to cough up the amount plus interest to support your own retirement. If you accept that you are always free to NOT use your cpf funds for housing, or just don’t sell your house.

No doubt there are those who are truly lacking in money, but those are the extremely small minority. The problem with most people is that they spend too much. I know many acquaintances who readily complain about the rules/tax/gst/jobs, yet they regularly eat at restaurants, drive a car, go for aesthetic treatments, etc. Living a basic life in Singapore is actually relatively cheap. It’s only when you add in all the unnecessary items that it starts to get expensive.

The accrued interest is compounded interest of 2.5% based on the amount withdrawn (lump sum and monthly mortgage payments) over the withdrawn period. The accrued interest goes back to the individual(s) CPF OA account. So actually, this helps to increase your CPF OA sum which eventually will be transferred to your retirement account. Personally to me, it is a good approach that the govt is helping us (the citizens) in our retirement. I did my sums before I sold my hdb and as such, I was about to return both the original sum plus accrued interest and have some positive cash returns as well.

Kalang guni man got no cpf and die without money bring to oven .. haha

Maybe 99.co can correct my interpretation if I am wrong. The accrued interest is not the amount being paid to CPF nor HDB and disappear. It is mentioned in the article that “On the other hand, if the property was sold at a market price, after paying off the outstanding loan, if the remaining balance is less than the amount of CPF savings to be returned, they would not have to top up the difference in cash.” So it should not be considered as debt. It is the additional amount that should had been parked into my CPF account after house sales. This can be withdrawn by cash at 55 under their terms and conditions fulfilled, or given back to me for retirement as CPF Life Payout, or given to my beneficiary when I die. Is my understanding correct?

and why retirement account cant be use to buy hdb the cpf that you people automatic trsf it to RA,seems like we are your children after 65 you give as back our pocket money every month,I dont know I can live longer to feel the money so why not l pay all the RA money for my BTO that’s my retire home too

I’m considering myself as mid class and the few lucky ones with no debts. HDB fully paid and own another property. Life is bless for me. But Im worry and fear for the future of SG. The worry for my children and the next generation. The high cost of HDB flats,( easily 600k and above for new) the competition for jobs and University. I don’t want my children to be in the rat race, slave to mortgage loan. A milking cow working for the gov or society. Our quality of MPs just sucks and can’t compared with the 1st gen of old guards and the list goes on…

But before we can complain more, do understand there’s no perfect country and government. There’s always a trade off and can’t have best of both world. Yes, sg flats are expensive. But most of us have a home or shelter over our head. (Try compare to our neighbouring country Thai,info,Viet,phill, JB and worse HK) SG is a small country with no natural resources and it’s getting hard to be in the game especially when neighbouring countries are slowing catching up. Sg may not be the best place for our next future generations maybe 20-30 years from now. My advice for my kids would be to ask them to venture the world ( studying/ working/ business) most likely my future generation would not be here to stay for good.

Thats because when you allow Public Housing to raise till like there is no tomorrow, you are actually robbing the people CPF. The HDB should justify their BTO housing price tags and be transparent about it.

CPF is for Retirement ..rule number 1.

Any amount taken out for Housing muz b put back + interest… rule number 2

STOP The CPF abuse … effectively with rule 1 n 2.

Retires with CPF saving with your hard earned saving honorably n with pride.

So what does cpf do when the owners do not have enough moneysmart to return? So don’t need to return? Then that’s a loophole.

We agree that the HDB houses should not be too expensive for future generation to bear. But will we be happy when our HDB price drops? With the recent cooling measure announced on 16 Jan, it is interesting to see what happen to our existing HDB house price…

From the 99.co article, no need to return. “if the property was sold at a market price, after paying off the outstanding loan, if the remaining balance is less than the amount of CPF savings to be returned, they would not have to top up the difference in cash”. I do not think it is a loophole. The whole idea is to enforce saving for retirement. Return also return to my CPF account which I can withdraw later with CPF Life. (99.co please correct me if I am wrong) One may say may not live so long. Actually live long long then need money. Once old, cannot walk, cannot see well, cannot drive taxi, cannot work in Macdonald. Where to get roti money. From children? If no children, from where? When I see how helpless an elderly is, and even need to buy expensive diapers for night time to contain more urine. I realized how important saving is for elderly. A house for shelter and some saving when I cannot walk to urine at night.

So many people misunderstood the CPF system … Which is rather sad. It is one of the best retirement system in the world and makes one responsible for his or her retirement and not kicking down the can down the road.

Those who are against accrued interest on amount taken out of CPF must understand that the primary purpose of CPF is for retirement. The accrued interest is amount that your CPF would have grown to had you not used your CPF housing.

CPF gave the concession to use CPF for housing but it must not deplete the amount of CPF for retirement. If you have met the retirement sum, there is no need to return the accrued if you are age 55 and above. If you are against accrued interest, then don’t ever use CPF for housing.

I suggest the whole proceed (in proportion to used) from sale of flat be returned to CPF and forget the idea of accrued interest in this way, just like when you use CPF money to buy share.