Buying an HDB resale flat comes with its perks, one of which is the generous HDB resale grants you can qualify for. These grants have seen significant updates over the years, making it easier for first-time buyers to afford their homes. With the HDB Flat Eligibility (HFE) letter, you will know upfront if you are eligible to receive CPF housing grants.

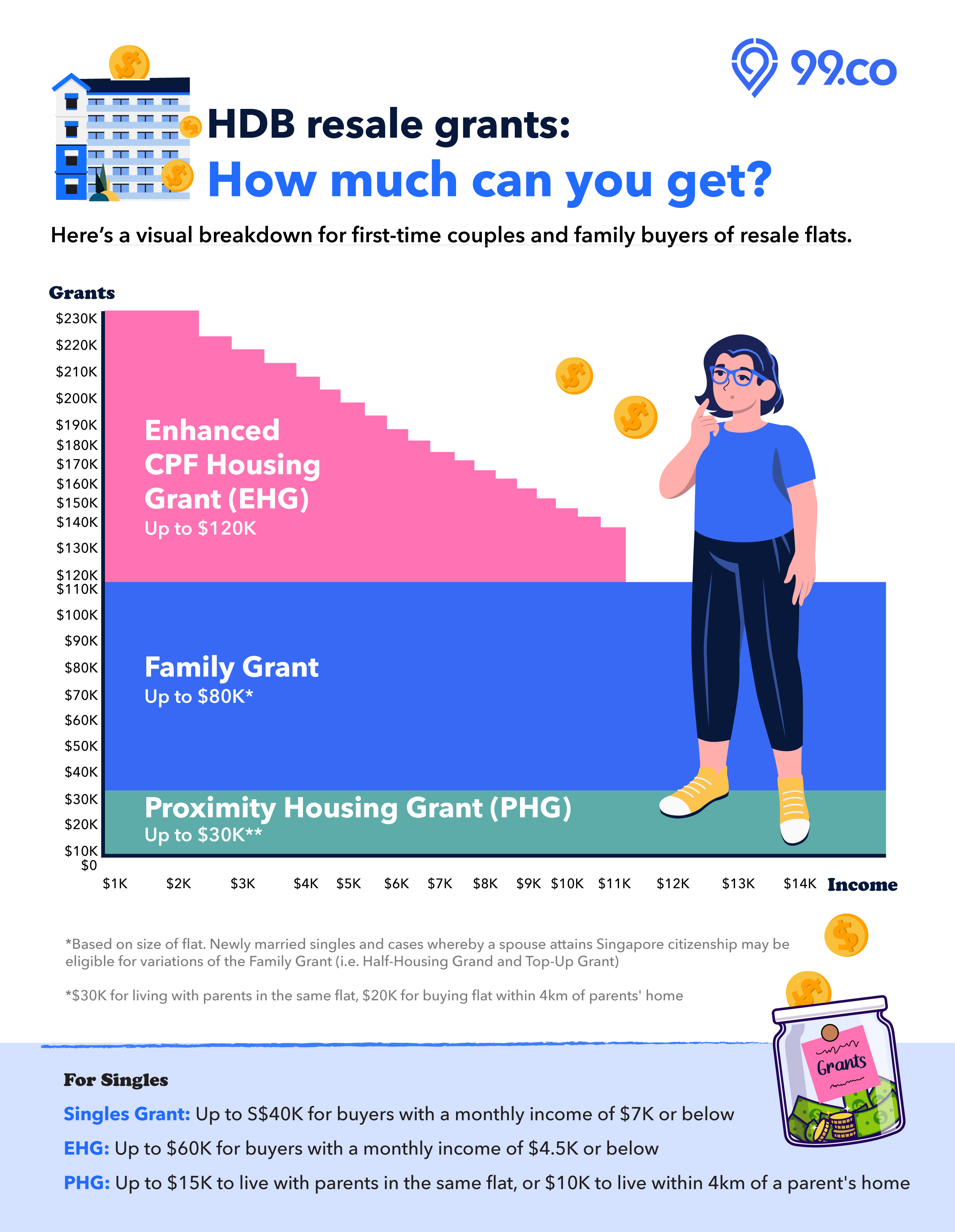

Since the announcement during the National Day Rally 2024, the Enhanced CPF Housing Grant (EHG) has been significantly increased to further support first-timer families and singles. In 2026, families can now receive up to S$120,000, while singles are eligible for up to S$60,000.

These changes could mean that HDB resale flats may be cheaper than a Build-to-Order (BTO) flat, even though HDB sells BTO flats at a discount. After all, the Family Grant and Proximity Housing Grant do not apply to BTO flats.

Plus, the key perks of buying a resale flat are an unlimited choice of locations and the fact that resale flats are already completed and ready for moving in. Resale flats also typically have well-developed amenities, such as schools, markets, and eateries, surrounding them.

Table of contents

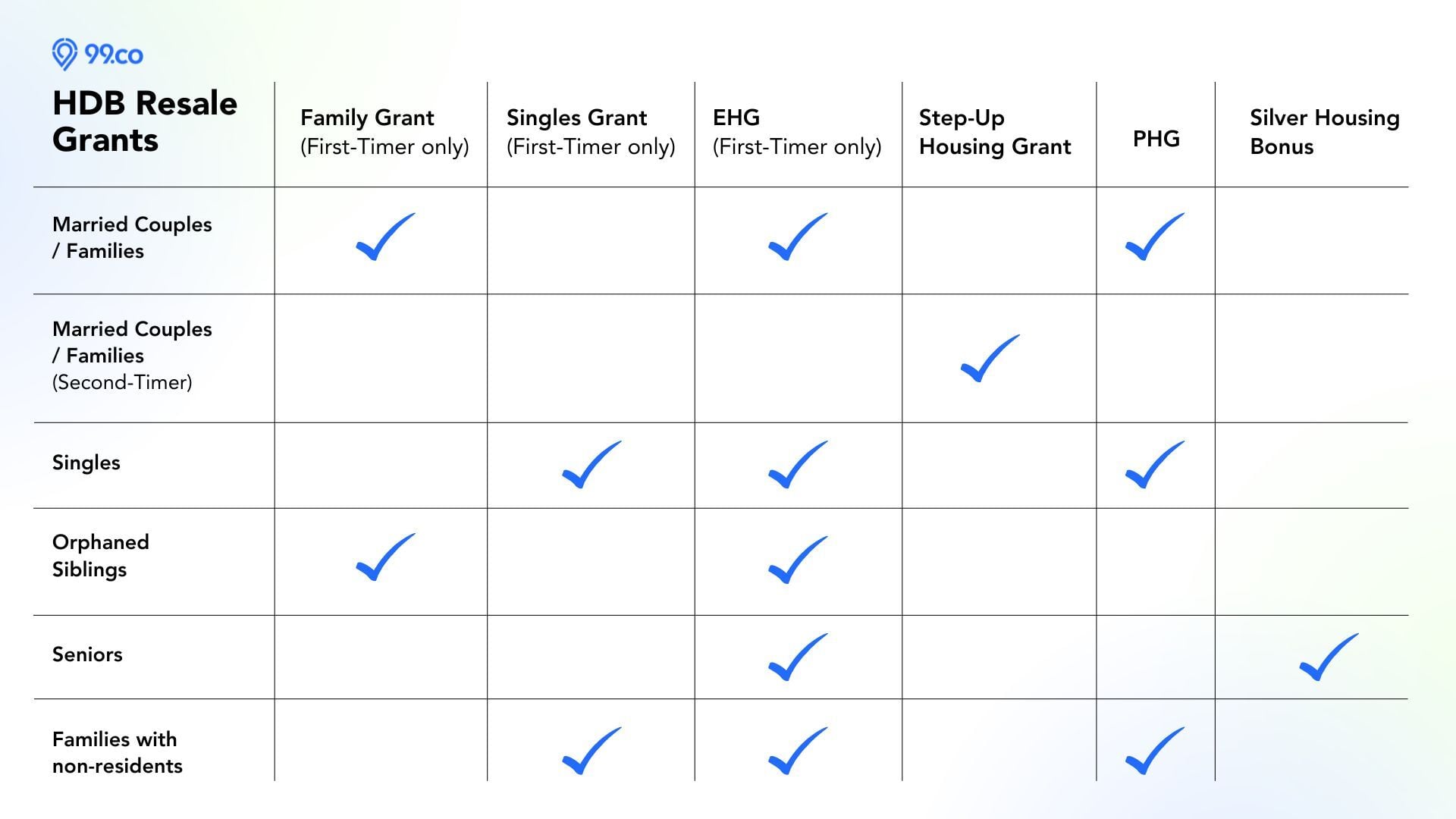

Types of HDB resale grants

Get ready; it’s quite a long list. (There’s a handy infographic below, too.)

Here are grants that might be available to you:

For married couples/families

Family Grant (FG)

- How much: S$80,000 if buying a 2- to 4-room HDB resale flat; S$50,000 if buying a 5-room or larger HDB resale flat.

- Income ceiling: To qualify for the Family Grant, the buyers’ household income must not exceed S$14,000. For extended families, the income ceiling is S$21,000.

- Who can qualify: Married/engaged couples or families who are first-timer applicants, buying an HDB resale flat and do not exceed the income ceiling. If one party is a Singapore Permanent Resident (SPR), they will receive S$10,000 less.

Enhanced CPF Housing Grant (EHG)

- How much: A maximum of S$120,000.

- Income ceiling: To qualify for the Enhanced CPF Housing Grant (EHG), the buyers’ household income must not exceed S$9,000. This is a tiered grant, meaning the lower your income, the higher your EHG amount you may be eligible for.

- Additional criteria: The remaining lease of the flat must be more than 20 years and cover the youngest buyer or essential occupier to the age of 95. At least one of the applicants or essential occupiers must have worked continuously for at least 12 months and still be working at the point of the HFE letter application.

Proximity Housing Grant (PHG)

- How much: S$20,000 if living near your parent’s/children’s home (within 4km); S$30,000 if living with your parents/children in the same resale flat.

- Income ceiling: The PHG has no income ceiling restrictions.

- Additional criteria: Applicants for this grant must not have previously received the PHG.

Here’s the breakdown of the HDB resale grants in a handy infographic

Case Study

Here’s an example:

You and your spouse are first-time applicants and want to buy a 5-room HDB resale flat near your parents’ home. Living near your parents will give you peace of mind with one child and a baby on the way. You will receive:

S$20,000 in PHG, as you live within 4km of your parents’ but not with them.

You earn S$5,000/month, and your spouse earns S$3,500/month. The average gross monthly household income is S$8,500. This means:

- You have met the income ceiling and are therefore eligible for the Family Grant. As you are purchasing a 5-room flat, you will receive S$50,000 in Family Grants.

- You have also met the income ceiling and are eligible for the EHG. According to the S$8,500 household income, you will receive S$10,000 in EHG Grants.

You’re eligible for S$80,000 in HDB resale grants in this scenario. Not bad!

[Psst, there’s more about BTO/resale grants for couples in this article, which includes a flowchart to help you see what grants you may be eligible for.]

For singles

Singles Grant

- How much: S$40,000 if buying a 2- to 4-room HDB resale flat; S$25,000 if buying a 5-room or larger HDB resale flat.

- Income ceiling: To qualify for the Singles Grant, your average household income for the past 12 months must not exceed S$7,000 if you buy under the Single Singapore Citizen Scheme. For the Joint Singles Scheme, the income ceiling is S$14,000.

- Additional criteria: The remaining lease of the flat must be more than 20 years.

Enhanced CPF Housing Grant (EHG) for Singles

- How much: A maximum of S$60,000.

- Income ceiling: To qualify for the Enhanced CPF Housing Grant (EHG) for Singles, the buyer’s household income must not exceed S$4,500.

- Additional criteria: The remaining lease of the flat must cover the buyer to the age of 95.

Proximity Housing Grant (PHG)

- How much: S$10,000 if living near your parents’/children’s home (within 4km); S$15,000 if living with your parents/children in the same resale flat.

- Income ceiling: The PHG has no income ceiling restrictions.

- Additional criteria: Applicants for this grant must not have previously received the PHG.

For newly married couples

Top-Up Grant

- How much: The Family Grant amount you are eligible for currently, minus the Singles Grant amount you previously received.

- Income ceiling: The household’s combined income must not exceed S$14,000 monthly.

- Additional criteria: You have previously received a Singles Grant to buy a resale flat or bought a 2-room BTO flat under the Single Singapore Citizen Scheme, Joint Singles Scheme, or with family members or non-resident spouses.

Citizen Top-Up Grant

- How much: S$10,000.

- Additional criteria apply if an SPR spouse, child, or parent/sibling originally listed in the flat application gets Singapore citizenship.

Step-Up CPF Housing Grant

- How much: S$15,000.

- Income ceiling: The household’s combined income must not exceed S$7,000 monthly.

- Additional criteria: Only those currently living in a public rental or 2-room subsidised flat in a non-mature estate are eligible.

The maximum amount of HDB resale grants you can get is S$230,000.

With the three main grants — Family Grant, EHG and PHG — available for resale flats, you may be eligible to receive a total of S$230,000. Pretty impressive, huh?

In comparison, the typical BTO applicants will be eligible for a maximum of S$120,000 in grants, as they may only be eligible for the EHG. BTO applicants do not qualify for the Family or Proximity Housing Grant.

If you are wondering why there is a large gap, it is because resale flats are generally sold at market value. On the other hand, HDB sells BTO flats at a discounted price. The discount is mainly due to the additional waiting time for a BTO flat to be built.

For certain locations and towns, if you factor in the higher HDB grants available for a resale flat, buying an HDB resale flat can be even lower than a BTO flat.

(Of course, the catch is that the cheaper HDB resale flat may have a lower remaining lease, whereas a BTO flat comes with a fresh 99-year lease.)

How do HDB resale grants work?

How to apply for HDB resale grants?

You’ll need to apply for the HFE letter before the owner issues you an option to purchase (OTP) a resale flat.

Based on certain criteria, such as income, HDB will determine your eligibility to

- Buy an HDB flat (BTO or resale)

- Receive grants you qualify for and the respective grant amounts

- Get an HDB housing loan and the loan amount

One thing to note is that the income assessment period is 12 months, calculated up to two months before the HFE letter application. This may affect your eligibility for certain grants with an income ceiling.

Moreover, the HFE letter will be processed within 21 working days. So, apply for the HFE letter before starting your home-hunting journey to better understand how much you can afford.

After you’ve received the HFE letter, you can proceed with searching for your dream home.

For a quicker look at how much you can afford, use 99.co’s affordability calculator

Once you and the sellers have agreed on the asking price and exercised the OTP, you must submit a resale application via the HDB Resale Portal (your agent may help you with this).

You’ll be asked to specify which housing grants you apply for on your resale application.

How will you get the HDB resale grants?

Once approved, the housing grants are disbursed to your CPF Ordinary Account (CPF OA) to pay upfront for your HDB resale flat. The grant amount covers any outstanding downpayment of the flat before being used to reduce the amount you need to loan.

You can find out which suits you better: an HDB or a bank loan.

But here’s the catch. When you eventually sell the flat for which you received these grants, you must return them and a 2.5% per annum interest for every year you’ve had your flat back to your CPF OA. The good news is that you can use it for your next home purchase.

To learn more about accrued interest, read this article: How the CPF accrued interest can affect your property sale proceeds.

Next step, find your ideal HDB Resale flat

Now that you’re all caught up with HDB resale grants, it’s time to start looking for a home. 99.co HDB Resale Flat Listing portal has several comprehensive filters to enhance your property search:

- Travel Time lets you narrow down listings by travel time. If you hate commuting or want to find the sweet spot between up to five locations, use this to find your ideal resale flat.

- Radius Filter lets you search for listings within 4km of an address. This is helpful if you want to qualify for the Proximity Housing Grant (PHG).

- School Filter lets you see listings within 1km of any primary school in Singapore.

- MRT Filter allows you to find properties within walking distance to the nearest MRT station.

- Remote Viewing lets you see listings that are available for online viewing. This lets you get a feel of the respective flats, before coming down for a physical viewing. A time-saver, if you ask us!

Have a question on HDB resale grants? Ask us in the comments below!

If you found this article useful, 99.co recommends How much do you need to earn to buy an HDB resale flat? and COV Singapore — What is Cash Over Valuation (COV) of a resale HDB flat?

Frequently asked questions

Depending on your eligibility, a few main grants are available: the CPF Housing Grant, Enhanced CPF Housing Grant and Proximity Housing Grant. Other grants include Top-Up Grant and Step-Up Grant.

What’s the maximum amount of HDB grants I can receive?

If you’re buying an HDB resale flat as a couple/family, you can receive up to S$230,000 with the three main grants — Family Grant, EHG and PHG.

What is the Family Grant, and who qualifies for it?

The Family Grant provides S$80,000 for a 2- to 4-room HDB resale flat and S$50,000 for a 5-room or larger flat. The household income must not exceed S$14,000 (S$21,000 for extended families), and it is available to married/engaged couples or families who are first-time applicants.

What is the Enhanced CPF Housing Grant (EHG), and its criteria?

The EHG provides up to S$120,000 based on a tiered system where lower income qualifies for higher amounts. The household income must not exceed S$9,000. Additional criteria include a minimum remaining lease of more than 20 years; at least one applicant must have worked continuously for 12 months.

What is the Proximity Housing Grant (PHG), and its criteria?

The PHG provides S$20,000 for living near parents/children (within 4km) and S$30,000 for living with parents/children. There is no income ceiling, but applicants must not have previously received the PHG.

What are the additional grants for singles and newly married couples?

- Singles Grant: Up to S$40,000 for a 2- to 4-room flat and up to S$25,000 for a 5-room or larger flat.

- Enhanced CPF Housing Grant (EHG) for Singles: Up to S$60,000 with an income ceiling of S$4,500.

- Top-Up Grant and Citizen Top-Up Grant: Additional grants are available for those who previously received a Singles Grant or have a new Singapore citizen in the household.

How will I receive my HDB grants?

Housing grants are disbursed to your CPF Ordinary Account (CPF OA) to pay for your HDB resale flat upfront. The grant amount covers any outstanding downpayment of the flat before being used to reduce the amount you need to loan.

Can I keep my HDB grants forever?

Sorry, if you sell the flat for which you received these grants, you’ll need to return them, as well as a 2.5% per annum interest for every year you’ve had your flat, back to your CPF OA. The good news is that you can use it for your next home purchase.

About 99.co

We are a property search engine with the overarching goal of building a more transparent and efficient property market. We are working towards that future by empowering people with the tools and information needed to find a place to live in the best way possible.

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

My daughter is 25 this year can she buy a resale flat n me as a second owner…we actually staying in one room rental flat n asking for transfer for 2 rooms rented flat…as advice the hdb branch officer ask my daughter to buy a flat coz its not worth of renting coz the renting will be higher as my daughter pay is about $2500…so the hdb branch officer ask my daughter reconsider to buy a house…my daughter ever went to hdb n my daughter couldnt get any grant coz i ever bought a house n ever use grant before…can you pls help can my daughter buy a house n can she get any grant…my daughter n i ever go to hdb n the officer say my daughter can buy house only if my name under occupier pls advice if my daughtet can get the grant n buy house with her age now …thk u

Hi Rozita, thanks for your query. As a single, your daughter can only buy a HDB flat when she turns 35. If you’re just listed as an occupier, she will still. However, if you’re currently living in a one-room rental flat, you may be eligible for the Step-up grant of $15,000. Also, depending on what grants you have taken before, you + your daughter may be eligible for the EHG (Singles), and also the Proximity Housing Grant of up to $30,000. You can get more info from this article: Quick Guide to BTO and Resale HDB Grants for Couples [2020 Edition]

Hi I bought my resale 3rm HDB in 2013 at the time both of us PR. I converted to singapore citizen on 2018. Is it consider first time application for my situation now? My pay is ard $3500 and my wife not working. May i know how much grant I can get?

Hi Kok Weng, you are considered a first timer as long as you didn’t take any grant from HDB for your resale flat. Otherwise, you’ll be a second timer. You may refer to this article for more information on possible grant amounts: Quick Guide to BTO and Resale HDB Grants for Couples [2020 Edition]

Regarding the grant amount deposited into our OA, it’ll be used to offset the down-payment, that’s clear. However, what if you’re taking a bank loan and your EXISTING OA balance already covers the 20% requirement, does that mean the purpose of the grant is simply to reduce the amount taken off your OA (hence, you can compound a greater OA balance) and it ultimately has no difference towards your loan amount and mortgage?

For example (Bank loan)

Prop price: 100000

Downpayment: 25000

OA balance before grant: 25000

Downpayment by cash: 5000

Downpayment by CPF: 20000

Loan amount: 75000

Grant amount: 20000

In this case, the loan amount is still the same as without grant, right? The only diff is my OA won’t start from zero.

Kinda confused, so thanks in advance.

Hi Dave, yes, you are right. The existing CPF-OA amount will remain untouched if the cash + grant amount covers the downpayment fully and your bank loan is in place. You may also choose not to apply for the grant.

How can my brother purchase a flat ? He’s divorced and single now. No dependents. Is he entitled to purchase a balance flats from the 2 bedroom flexi flats?

Hi there,

I’m a Singaporean and my wife is a foreigner holding an LTVP.

We just had our first child a few weeks ago.

Under what scheme will we fall under? Foreign spouse scheme?

If so how much grants can I receive.

Hi I am divorced and in my 2nd marriage.

Bought 1st HDB resale with 1st timer grant. 2nd HDB bought from open market. Divorced and gave away entirely unit to my ex- wife. Remarried and current with is PRC and on Long Term Visit Pass . What grant can i take up if i were to buy from open market. If i apply for BTO, will HDB waive the levy as I am no more interest in the earlier property and did not profit and in fact given away my entire OA.

I am a male, divorced about 6 years ago, age 47, may I know what Grant’s is applicable to me when I buy a resale flat? I am not allowed to buy flat directly from HDB? Can I use my CPF to service my bank loan? And can I take a loan from HDB? The above are some of the queries that I have, need advice…thks.

Hi there, wanted to clarify as my spouse is currently a LTVP holder, am i still eligible to buy a resale flat? (understand that i am not eligible for a BTO flat). Would also hope you can answer some of my queries below :

1. Currently i have a joint ownership with my father in my current flat, if i remove my ownership form the current flat, am i eligible to purchase a resale flat?

2. If i am eligible, which type of grant can i take? Current flat i did not take any grant fyi.

3. Also, what is the payment procedures like when purchasing a resale flat?

Hello, does all 3 applies if my spouse is a non SC?

EHG, Family grant and PHG, if i stay near my parents. Appreciate the reply. Thanks!!

My parents just divorced. I am 27 year old and planning to buy a 3 room resale flat with my mother. Am I able to buy a resale flat together with my mum as I am less than 35 year old? Also if I am able to do that, what are the grants we are eligible for if my mother have not taken any grants before. Thanks in advance!

Can I get these grants for a Executive Apartment as well?

Good article! We are linking to this great article on our site. Keep up the good writing.

Currently I am applying for HDB resale hse. My property agent didn’t know of the 6 mth rule of the self employ and do a submission of the application in 22 October 2020. Thus HDB rejected my single grant of 25000 as they wanted april to Sept 2020 income which 8k but my may to October 2020 is 6k. In this situation, what shall I do?

Hi, I and my ex-wife bought 4rm resale flat many years ago as PR in joint tenancy. Now we are divorced. She agreed to transfer the flat to me, and refund her CPF and accrued interests about $30k. I am above 35 years old and now converted to Singaporean. Can I apply for the HDB single grands and enhanced grant to pay for the $30k CPF refund to my ex-wife? Thanks.

We are family of four of which myself ,my wife and my youngest son are all SPR except for my oldest son is now an SC. We’ve been SPR since 2006. May I enquire where we can fit-in to apply for a resale flat. Is there a waiting period for HDB approval,. We can only use our CPF for this purpose.

Thank you

Hi.as am singaporean,are we entitle for 2nd time for hdb housing loans…?

We had bought am 2nd hand EC,about 8years old.still not yet privatise yet.that loans is from ocbc. in singapore,buying am EC, is consider,am private apt/condo. Are thay no different derive from minimun stay of 5 years.them allow to sell to singaporean/pr.but not to foreigner,unlike private condo.can sell anytime to foreigner.i buy am EC, is till not privatise.still under the hdb guideline.not privatise guideline…wat is that going to do with 2nd timer entitle hdb housing loans .and those who ever buy amEC,that took bank loans .instead of hdb loans.am i believe many singaporeans is facing this issue….where is local born singaporean given any choice of priviledge.for hdb loans.is for all singsporean/pr. Must be entitle for hdb loans,this is national democratics by our’s belove ,LKY. Thanks.