What is ABSD (Additional Buyer’s Stamp Duty)?

The most notorious cooling measure, the Additional Buyer’s Stamp Duty (ABSD), is a stamp duty paid on your residential property. The cost is a percentage of your property price or valuation, whichever is higher.

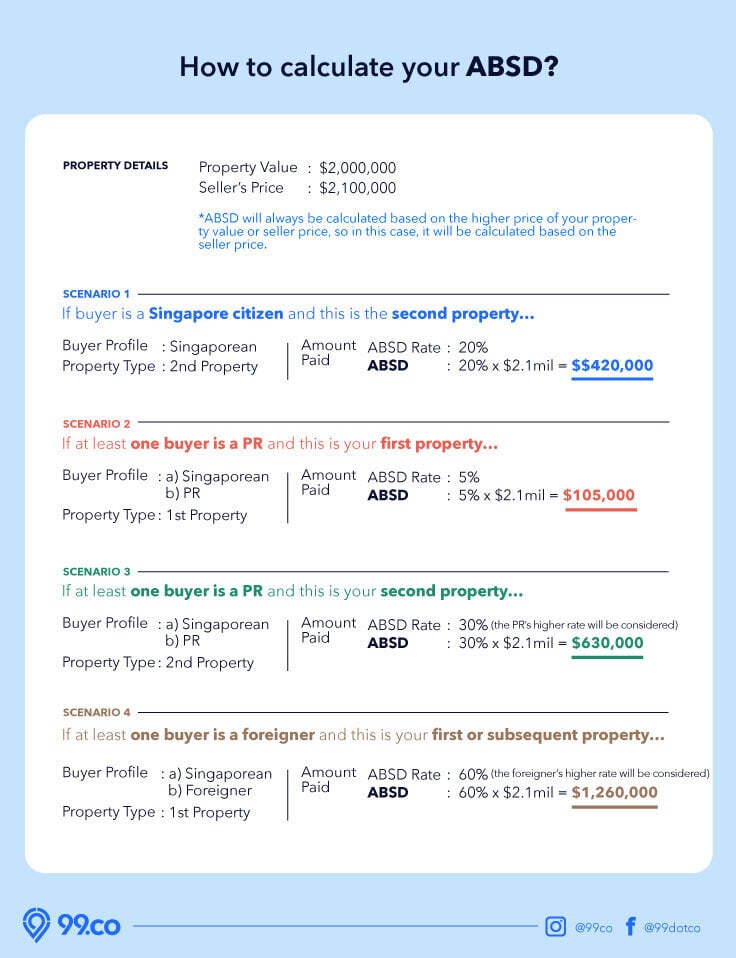

For example, say you’re buying a residential property valued at S$2 million. The seller’s price, however, is S$2.1 million. If this is your second residential property, as a Singaporean, you’re subjected to an ABSD rate of 20%. This means you pay a stamp duty of 20% of S$2.1 million (S$420,000).

The amount payable varies and is based on:

- Your citizenship or residency status

- The number of residential properties you own

- Whether you’re an individual, an entity, or a developer

|

ABSD rate from 16 December 2021 to 26 April 2023 |

ABSD rate from 27 April 2023 |

Increased by |

||

|

Singapore citizens |

First residential property |

0% |

0% |

– |

|

Second residential property |

17% |

20% |

3% |

|

|

Third and subsequent residential property |

25% |

30% |

5% |

|

|

Permanent Residents (PR) |

First residential property |

5% |

5% |

– |

|

Second residential property |

25% |

30% |

5% |

|

|

Third and subsequent residential property |

30% |

35% |

5% |

|

|

Foreigners^ |

Any residential property |

30% |

60% |

30% |

|

Entities |

Any residential property |

35% |

65% |

30% |

|

Trustees |

Any residential property |

35%* |

65% |

30% |

|

Housing developers |

Any residential property |

35% (remittable) + 5% (non-remittable) |

35% (remittable) + 5% (non-remittable) |

– |

^Excluding Nationals and Permanent Residents of Iceland, Liechtenstein, Norway, and Switzerland, and Nationals of the United States of America, who will be subject to the same ABSD rate as Singaporeans.

*The ABSD rate for trustees was from 9 May 2022 to 26 April 2023.

What if you’re purchasing the property with another person?

If you’re jointly buying the house with another person with a different profile (eg. different residency status and/or several houses owned), you’ll be subjected to a higher ABSD rate.

SC-PR buyer with no residential properties

Let’s say you’re buying a S$2 million condo with your partner, who is a PR. This is the first property for both of you as an unmarried couple. However, given your partner’s PR status, you will be subjected to a 5% ABSD rate. This means that the ABSD to be paid will be S$100,000.

SC-SC buyer, with one buyer owning a house

Likewise, if you and your partner are Singaporeans, and your SO has another property to their name, you’ll be subjected to a higher rate. Here, you will be subjected to an ABSD rate of 20%. So the ABSD to be paid will be S$400,000.

Here’s an infographic summarising how to calculate the ABSD.

Alternatively, use 99.co’s stamp duty calculator to calculate how much ABSD to pay!

But you may be eligible for the ABSD remission if you’re already married.

What is ABSD remission, and how do you get it?

You can apply for ABSD remission if:

- You are a married couple in Singapore,

- At least one spouse is a Singapore Citizen

- Jointly purchase the property

If you purchase a second house, you’ll first have to pay the ABSD as usual (this is within 14 days of purchase). However, you can apply for a remission if you sell your first home within six months of buying the second one.

For example, say you just got married and upgrading from your shoebox unit to a bigger condo unit. For convenience, you purchase the condo unit before you sell your shoebox apartment.

Resale condos for sale

You must pay the ABSD within 14 days of signing the Option to Purchase (or Sale and Purchase Agreement if no OTP is issued) to buy the condo unit. You can then apply for the money back if you sell your shoebox within six months of getting your condo.

Note that you must remain married when you apply for the remission, and you must not have bought more properties before applying.

Hold on, what if the second property is still being built?

If the second property is under development (e.g. a new launch condo), you must sell your first house within six months of the second property getting its Temporary Occupation Permit (TOP) or Certificate of Statutory Completion (CSC), whichever is earlier.

New launch condos for sale

Why do we have ABSD?

ABSD serves various purposes.

First, it applies downward pressure on property prices. When the government feels that private property prices are getting out of hand, they increase the ABSD to slow the price increase. This prevents the formation of property price bubbles, which can wreak havoc on the local economy.

Given the price increase in the last couple of years, the government raised the ABSD rate in December 2021.

While this moderated the property market, prices are still on the rise, prompting the government to increase the ABSD rates again in April 2023.

A second purpose is to create an ownership bias, ensuring most of Singapore belongs to Singaporeans. That’s why the stamp duty is steeper for companies and most foreigners.

(Under the Free Trade Agreements with the respective countries, Nationals, and Permanent Residents of Iceland, Liechtenstein, Norway, Switzerland, and Nationals of the United States of America will be subject to the same ABSD rates as Singaporeans. This means they won’t have to pay 60% for their first home purchase here.)

A third reason arose during the en-bloc fever of 2017. Foreign developers caused a huge surge in en bloc sales. This artificially injected huge amounts of cash into the property market, which could later have translated to excessive supply and inflated home prices (the more developers pay for land, the more their properties cost).

In response, the ABSD has become especially high on property developers to put the brakes on land purchases and en bloc sales. For instance, developers are now subjected to an ABSD rate of 40%. While the 5% is non-remittable, the 35% is remittable if they can finish construction and sell all the units within five years.

It’s also why we see some developers giving discounts for condos that are nearing their ABSD deadlines.

Does ABSD matter to the average Singaporean who doesn’t own more than one house?

ABSD is indirectly keeping your home affordable. It’s less great in that if you’re moving to a new house, it can cause cash flow issues.

(This isn’t an issue if you’re moving from an HDB flat to another HDB flat or a new EC since you won’t have to pay the ABSD. )

For example, say you’ve lived in a shoebox unit all your life, but now you’ve got married. You need a bigger condo unit. Well, if you buy a condo unit before selling your old shoebox, you’ll have to pay the 20% ABSD within 14 days of making the purchase.

You can apply to get the money back, but this can only be done if you sell your old shoebox within six months of buying your new, bigger condo. Any disruption to the process — such as buyers pulling out at the last minute — can inadvertently cause you to give up the ABSD remission.

There’s also the annoying fact that you need sufficient cash to pay for the ABSD first when you’re already forking huge sums for a new house (although ABSD can be paid through your CPF).

For these reasons, sell your old house before buying a new one, however inconvenient it may seem.

Can you avoid the ABSD?

Technically, no, you can’t. But there are a few ways to get around the ABSD legally. These include decoupling and buying a property in a trust. There are a few pitfalls to these strategies.

For instance, with decoupling, you may pay more than the ABSD itself. This is because you have to incur legal fees for the decoupling itself. Your partner will also have to pay the BSD to buy your share. So be sure to do the math first before jumping into decoupling.

As for buying a property under a trust entails putting it under your child’s name (since your child doesn’t have a property to their name yet). One downside is that you’ll have to pay the property in cash. And when your child buys a property on their own in the future, they’ll have to pay the ABSD.

However, since 9 May 2022, those buying under a trust will be subject to ABSD, with the rate initially implemented at 35% before increasing to 65% in this latest round of cooling measures. They can still apply for remission, but they’ll have to pay the ABSD first and meet the following conditions:

- All beneficial owners of the residential property must be identifiable individuals (i.e. you cannot transfer it to an unborn child)

- The beneficiary owner must own the property now and not in the future; and

- The trust deed cannot be changed or revoked or come with any conditions, e.g. the child will only own the house when they get married, so it must be a genuine gift to the beneficiary

Alternatively, you won’t be subjected to the ABSD if you’re buying a new EC (since you have to dispose of the existing property) or a commercial property.

How to pay ABSD in Singapore?

You can settle your ABSD payment conveniently through the e-Stamping Portal. Payments can be made using NETS, a cheque, or a cashier’s order.

Alternatively, you can visit IRAS Surf Centre e-Terminals or SingPost Service Bureaus in Chinatown, Novena, Raffles Place, and Shenton Way.

[Additional reporting by Virginia Tanggono]

Planning to sell your house soon? Let us help you get the right price by connecting you with a premier property agent.

If you found this article helpful, 99.co recommends a Full list of new launch condos (with unsold units) approaching their developer ABSD deadlines in 2023/2024 and Dual-key condo: Analysing the pros and cons.

Frequently asked questions

Additional Buyer’s Stamp Duty (ABSD) is a stamp duty to be paid on top of the Buyer’s Stamp Duty (BSD). Whether you need to pay for it depends on factors such as your residency status and the number of residential properties you own.

What is the current ABSD rate?

As of 27 April 2023, the current ABSD rate for Singaporeans is 20% for the second residential property and 30% for the third residential property.

When do I have to pay ABSD?

You’ll have to pay the ABSD within 14 days of signing the Option to Purchase (or Sale and Purchase Agreement if no OTP is granted) for the property.

Can ABSD be paid using CPF?

No, you must pay the Additional Buyer’s Stamp Duty (ABSD) in cash.

Is ABSD refundable?

ABSD is not refundable. However, there may be specific circumstances where you can apply for remission and get a refund.

Does ABSD apply to HDB flats?

Yes, ABSD applies to all residential properties in Singapore, including HDB flats.

How do I pay ABSD?

You can pay through the e-Stamping Portal using NETS, cheques, or cashier’s orders. You can also visit IRAS Surf Centre e-Terminals or SingPost Service Bureaus.

About Ryan Ong

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

I have one private residential unit for stay. If I am buying a shop house, am I subject to any ABSD