Considering HDB loan vs bank loan is most probably the second thing many first-time homeowners have on their minds, after figuring out where their first home should be. To make your home purchase journey a little bit smoother, we’ll break down the differences between HDB loans and bank loans for you!

Table of contents

Overview

Here’s the key points about HDB loan vs bank loan:

- Both have the same maximum loan-to-value (LTV) ratio of 75%, meaning you’ll have at least a 25% downpayment to be paid in cash and/or CPF OA savings.

- Interest rates of bank loans are highly variable, whereas HDB loan rates seldom change (the current concessionary rate is 2.6%)

- You can switch from an HDB loan to a bank loan, but not the other way around

- In terms of late payments, HDB is more lenient than banks

| HDB Loan | Bank Loan | |

| Interest Rates | Concessionary rate is fixed at 0.1% above the prevailing CPF rate. Current rate for HDB loan is 2.6%. | Interest rates are more variable, depending on market conditions. (including fixed rate home loans, which will follow a floating rate after the lock-in period) |

| Eligibility | Has an income ceiling, currently at S$14,000 (S$21,000 for extended families)Can take up to 2 timesRequires at least 1 SC buyer | No income ceilingNo limit on number of loans takenAnyone eligible to buy an HDB flat, including PR households who can buy from the resale market |

| Loan Tenure | Loan tenure capped at 25 years | Longer maximum loan tenure of 30 years |

| Refinancing | Can refinance to bank loan | Cannot refinance to HDB loan |

| Early Repayment | No penalty on early repayment | Early repayment penalty |

Let’s do a more detailed breakdown of this HDB Loan vs Bank Loan table!

Differences between HDB loan vs bank loan

1. Interest rates and monthly instalments

The concessionary rate for HDB loans is always fixed at 0.1% above the prevailing CPF rate. With the current CPF rate at 2.5%, the interest rate for HDB loans is 2.6% per annum.

It also means that your interest rate is more or less locked for the entirety of the loan tenure, so you’re less likely to see any drastic changes to your monthly instalments.

In contrast, depending on the market conditions, bank loan rates are more variable. And this isn’t limited to home loans with a floating rate.

This applies to loan packages that are pegged to fixed interest rates as well. After a lock-in period of two to five years, these so-called fixed-rate home loans follow a floating rate.

So technically, there is no perpetual fixed-rate home loan in Singapore.

Bank loan interest rates are mainly determined by these three floating-rate benchmarks:

- Singapore Interbank Offered Rate (SIBOR), which will be replaced by the Singapore Overnight Rate Average (SORA) by the end of 2024

- Board Rate (BR)

Whether you’re taking a SIBOR, SORA, BR or FHR home loan, the interest rate is the prevailing rate plus the bank’s spread.

“3M SORA + 1” means the interest rate is the prevailing three-month SORA rate, plus 1% charged by the bank (the spread).

Every three months, when the SORA rate changes, the interest rate will be changed to match the new rate.

This means that if you have a 1M SORA rate home loan, the loan repayment amount will change every month. If you have a 3M SORA rate home loan, the loan repayment amount will change every three months, and so forth.

However, note that SOR and SIBOR home loans are currently being phased out to make way for SORA, with some deadlines to observe:

- 31 March 2022 – 6-month SIBOR will be discontinued

- 30 June 2023 – SOR will be discontinued

- 31 December 2024 – 1-month and 3-month SIBOR will be discontinued

Likewise, “BR +0.5” means that the interest rate is the current board rate plus the bank’s spread of 0.5%. The difference is that the board rate is set entirely by the bank.

Meanwhile, an FHR home loan is pegged to the bank’s fixed deposit rates. So it’s pretty similar to a BR home loan as the rate is essentially determined by the bank.

Are bank loans cheaper?

The historical interest rate for bank home loans has been above 3%. In the early 2000s, the rate was 3.25 to 4%, making them more expensive than HDB loans.

However, due to the Global Financial Crisis in 2008, bank interest rates have been at record lows for several years. It was only in 2015 to 2016 that interest rates started going up again, leading to a high of 2.88% in 2019.

But as Covid-19 emerged and triggered a global pandemic in 2020, interest rates dropped again. Rates started increasing again in the fourth quarter of 2021 when three-year fixed rates were at 1.15%.

With the economy recovering in 2022, inflation followed, leading the US Fed to raise interest rates again. Consequently, banks here started hiking their interest rates, going as high as 4.5% for a two-year fixed-rate home loan in November 2022.

In short, whether or not bank loans are cheaper depends on the interest rates at the time, especially if you’re taking a floating-rate home loan.

When interest rates are lower than HDB’s concessionary rate (which has remained at 2.6% for the past two decades), taking a bank loan can be cheaper due to the lower monthly instalments.

But when interest rates rise above 2.6%, taking an HDB loan will be cheaper.

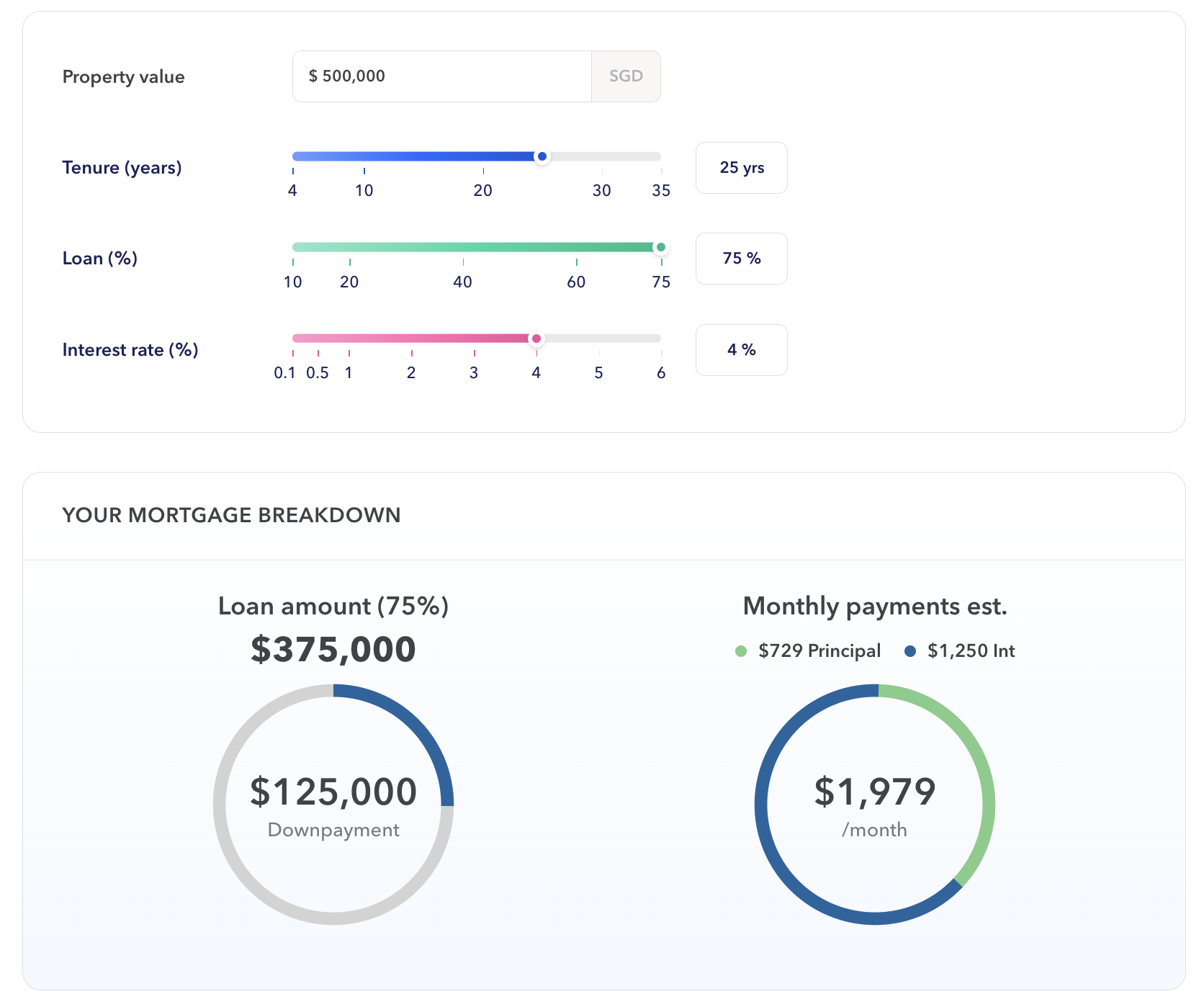

Comparing HDB Loan vs Bank Loan for a $500,000 flat with a 25-year tenure:

1. HDB Loan

With an LTV of 75%, the maximum loan quantum for an HDB loan is S$375,000, and the downpayment (25%) is S$125,000.

If you’re taking a HDB Loan (2.6% interest rate per annum) with a 25-year tenure, the monthly repayments will be S$1,701.

2. Bank Loan

With an LTV of 75%, the maximum loan quantum for Bank Loan is S$375,000, and the downpayment (25%) is S$125,000.

Breakdown of downpayment – $125,000

- Cash/OA Savings – $100,000

- Min. 5% cash payment – $25,000

If you’re taking a Bank Loan (4% interest rate per annum) with a 25-year tenure, the monthly repayments will be S$1,979.

*Bank loan rates are variable, subject to market conditions

When bank loans are cheaper

When interest rates fall below HDB’s concessionary rate, let’s say to 1.8% per annum, your monthly instalment will be cheaper at S$1,553.19.

When bank loans are more expensive

On the other hand, when interest rates rise above HDB’s concessionary rate, for instance to 4%, your monthly instalment will be more expensive at S$1,979.39.

You can also use 99.co’s mortgage calculator to figure out the monthly instalments for your home loan.

2. Eligibility criteria

Whether you’re buying an HDB BTO or resale flat, HDB loans come with stricter eligibility criteria, including the income ceiling.

Income ceiling

If your gross monthly household income is more than S$14,000, you won’t be eligible for an HDB loan.

If you’re applying as an extended family, the monthly household income must not exceed S$21,000.

| Family profile | Income of Group A (cannot exceed S$14,000/month) | Income of Group B (cannot exceed S$14,000/month) | Income ceiling of extended family |

| Parents* with single working children | Parents with one single working child | Other single children | The total incomes of Group A and B must not exceed S$21,000 |

| Parents* with married child** | Parents with single working children (if any) | Married child’s family** | |

| *Includes widow/widower or divorcee.**Includes applicants buying a flat with their fiancé/fiancée. | |||

Conversely, bank loans don’t have an income cap, so it’s suitable for those with a higher income.

Number of times you can take a home loan

What’s more, you can only take up an HDB loan twice. If you have maxed out on this, you’ll need to get financing from the bank.

Residential status

Do also note that to be eligible for an HDB loan, at least one of the buyers must be a Singaporean. This means that PR households (who are eligible to buy HDB flats from the resale market), can only take up a bank loan.

Other requirements to meet include:

- Must not have disposed of any private residential property in the last 30 months before applying for the HDB loan eligibility (HLE) letter

- Must not own more than 1 market/ hawker stall or commercial/ industrial property

3. Loan tenure

HDB loans are capped at 25 years, while bank loans for HDB flats have a longer maximum loan tenure of 30 years. However, the LTV will be reduced to 55% if the loan tenure exceeds 25 years or extends beyond the borrower’s 65th birthday.

(Read our guide on LTV limits to learn more about how the number of outstanding home loans you have can affect the loan amount.)

Having a longer tenure can be a good thing, as it allows you to lower your monthly repayments and spread them out. On the other hand, it also means paying a higher interest over time.

4. Refinancing

You can refinance your HDB loan into a bank loan (subject to the bank’s approval), even after getting a higher LTV for the initial loan. With a lower interest rate, you can reduce your monthly repayments.

However, you can’t refinance your bank loan into an HDB loan. What you can do is reprice it with the same bank or switch to another bank to refinance it.

5. Late payments

HDB charges for late payments of monthly instalments and reviews the rate annually. From 1 April 2022 to 31 March 2023, the rate is 7.5% per annum. It’s reviewed annually in April.

At the same time, they’re generally more lenient and open to negotiations for late payments. If for instance you get laid off and you do not manage to pay your home loan for a while, you may approach HDB for an extension or alternative repayments to try and keep the loan going while you’re getting back on your feet.

But this doesn’t mean you can get away without paying your home loan; you can still be asked to sell the flat and downgrade.

Similarly, with bank loans, your bank can help you work out viable repayment options. But banks are generally less forgiving to minimise their losses. So if you fail to repay your loan at some point, the road to foreclosure is a lot shorter.

HDB flats for sale

6. Early repayment

Another good thing about the HDB loan is that there’s no lock-in period, so there’s no early repayment penalty. This allows you to pay it off earlier to reduce the amount of interest to be paid and the financial burden on your plate.

But if you’re taking a bank loan, it’s better not to pay it off early. The bank will charge a prepayment fee if you cut short your bank loan within the lock-in period since they earn from the interest.

The benefits of consulting with a mortgage broker

Navigating the complexities of home financing can be challenging, especially for first-time homeowners. Working with a mortgage broker can provide valuable insights and personalized advice tailored to your financial situation. A mortgage broker can help compare different loan options, understand the details, and ensure the best possible deal. They have access to a wide range of loan products from various lenders, which can be beneficial when interest rates fluctuate.

By leveraging their expertise, individuals can make a more informed decision between HDB loans and bank loans, potentially saving time, money, and stress in the long run. This added layer of professional guidance can be crucial in securing a loan that aligns with long-term financial goals.

HDB loan vs bank loan: Which is better?

Ultimately, whether you should go for an HDB loan or a bank loan depends on your financial situation, your level of risk aversion, and your willingness to keep up with fluctuating interest rates.

If you’re on a tight budget, HDB loans should be considered first, as there is a smaller cash outlay. The fixed interest rate also gives you a better idea of how much you’re paying monthly for your home loan.

It’s also more suitable for those who only want to deal with the property loan paperwork once, and don’t want to spend time tracking interest rates now and then.

And when interest rates are down (and the HDB concessionary loan rate seems high in comparison), you can always refinance from an HDB loan to a bank loan.

If you intend to upgrade fast (e.g. sell the flat and buy private as soon as you can), you should consider a home loan that offers a lower interest rate. This helps to reduce your monthly repayments and minimise the interest eating into your resale gains.

At the same time, everyone’s case is different. To better understand which home loan is best for you, speak to 99.co’s mortgage broker. We can help you break down your finances and weigh the pros and cons to help you make an informed decision.

[Additional reporting by Virginia Tanggono and Ananda Bayu]

Would you get an HDB loan or a bank loan? Let us know in the comments section below or on our Facebook post.

If you found this article helpful, 99.co recommends What happens to your mortgage when you sell your house? and Buying via BTO, SBF or Open Booking? Everything you need to know about the payment timeline.

Frequently Asked Questions (FAQs)

How much loan can I get with an HDB loan?

You can get up to 80% of the purchase price or valuation, whichever is lower. For a S$500,000 flat, the maximum loan amount is S$400,000.

How much loan can I get with a bank loan?

The LTV for a bank loan is 75% of the purchase price or valuation, whichever is lower. For a S$500,000 flat, the maximum loan amount is S$375,000.

Can I switch to a bank loan after taking an HDB loan?

Yes, you can. When bank interest rates are lower than HDB’s concessionary rate, this is one option to reduce your monthly repayments.

About Ananda Bayu

Ananda has been wrangling Singapore's complex real estate trends into readable bites since 2020. She writes like she's explaining it to a friend over kopi — because who has time for jargon? When off the clock, she’s probably doom-scrolling through cat memes on X, convincing herself it's the highest tier of "creative inspiration".

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter