The most unappealing part of buying a condo is not when you stand in snaking queues in show flats. Rather, it is realising that you have to pay for the property which usually takes the thrill out of the whole affair.

That is why you should know all about the condo payment schedule before you enjoy the home-hunting experience. Let this article help you with all the important deets!

Table of contents

New launch vs resale condos: The key differences

Buying a condo unit typically falls into either of two categories:

- Buying a unit in a completed development. This is usually a resale or an unsold unit directly from a developer, such as Clover By The Park, Sky Habitat, and Thomson Grand.

- Buying a unit in an uncompleted development, a building under construction (BUC). This is usually a new launch condo unit, like SORA and The Hillshore, bought directly from the developer, but can also be a sub-sale from a buyer.

There are various factors that might push you towards one. For example, you might not wait three-plus years for your unit to be constructed, or purchase a unit in a development that is already been completed (and can be inspected with your own eyes). The thing is that while the condo payment schedules for the two types are not vastly different from each other, there are differences you should know.

Condo payment schedule of uncompleted developments (new launch condo)

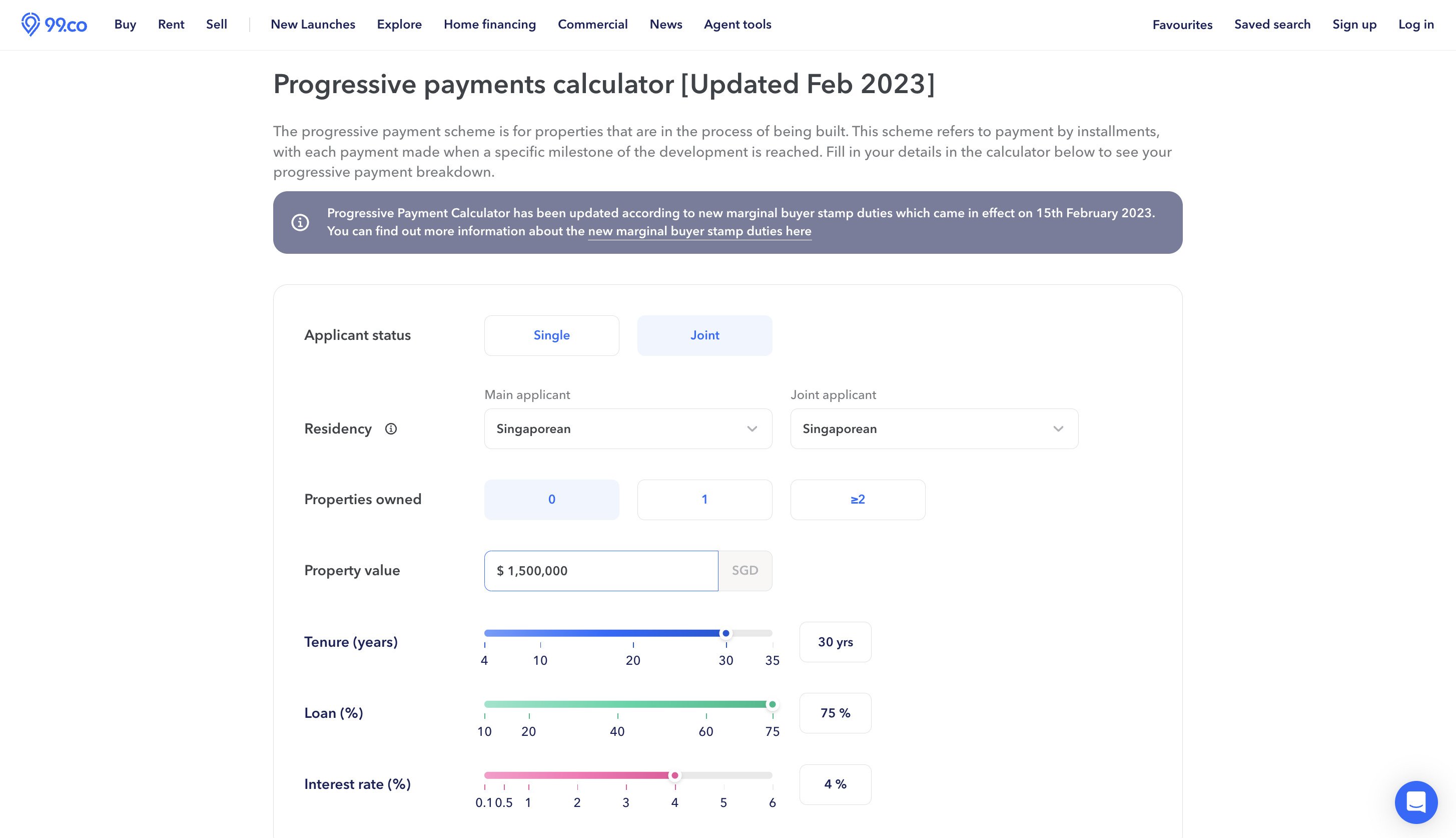

Let’s take the example of the newlywed couple Eddie and Alexandra, both Singapore citizens with a combined income of S$14,000/month and a CPF balance of S$60,000.

They are interested in purchasing a unit in a recent development that has yet to start construction at S$1,500,000. To help process their transaction, they have engaged private legal counsel who have agreed to charge S$3,500 for the entire purchase and have received their valuation report at S$350.

Since this would be their first bank home loan, they are entitled to up to 75% of the purchase price according to the loan-to-value (LTV) limit. This means that if they were to take out the full 75% financing, the loan quantum would be S$1,125,000.

As for the stamp duty, as they are both Singaporeans and this is their first property, they will only have to pay the Buyer’s Stamp Duty (BSD).

You can use 99.co’s Stamp Duty Calculator to calculate how much BSD you are subjected to.

Here’s what their condo payment schedule would look like if they opt for the progressive payment scheme available for new launch condos.

| Fee payable/stage of work | Approximate timeframe | % of purchase price | Amount payable | Payment mode |

| Exercising the option (Option or booking fee) | 5% | S$75,000 | Cash | |

| Sign the Sale and Purchase (S&P) agreement to exercise the OTP | Within 3 weeks of receiving it | |||

| Buyer’s Stamp Duty (BSD) | Within 14 days of signing the S&P | 1% of first S$180,000 | S$44,600 | Cash/CPF |

| 2% of next S$180,000 | ||||

| 3% of the next S$640,000 | ||||

| 4% of the next S$500,000 | ||||

| Downpayment | Within 8 weeks of exercising the option | 15% | S$225,000 | Cash/CPF |

| Legal fees | ~S$2,500 – S$4,000 | S$3,500 | Cash/CPF | |

| Valuation fee | ~S$350 – S$500 | S$350 | Cash/CPF | |

| Foundation of work | ~6 – 9 months from launch | 10% | S$150,000 | Cash and/or bank loan |

| Reinforced concrete framework | ~6 – 9 months later | 10% | S$150,000 | |

| Brick walls of unit | ~3 – 6 months later | 5% | S$75,000 | |

| Ceiling of unit | ~3 – 6 months later | 5% | S$75,000 | |

| Door and window frames in position, wiring, internal plastering and plumbing of unit | ~3 – 6 months later | 5% | S$75,000 | |

| Car park, roads, and drains serving the project | ~3 – 6 months later | 5% | S$75,000 | |

| Notice of vacant possession | TOP date | 25% | S$375,000 | |

| Legal completion date | Date of legal completion/certificate of statutory completion (CSC) | 15% | S$225,000 | |

| Total | S$1,548,450 |

Keep in mind that the booking fee of S$75,000 needs to be paid entirely in cash, and cannot be supplemented using CPF or a bank loan.

What is the monthly instalment for a new launch condo?

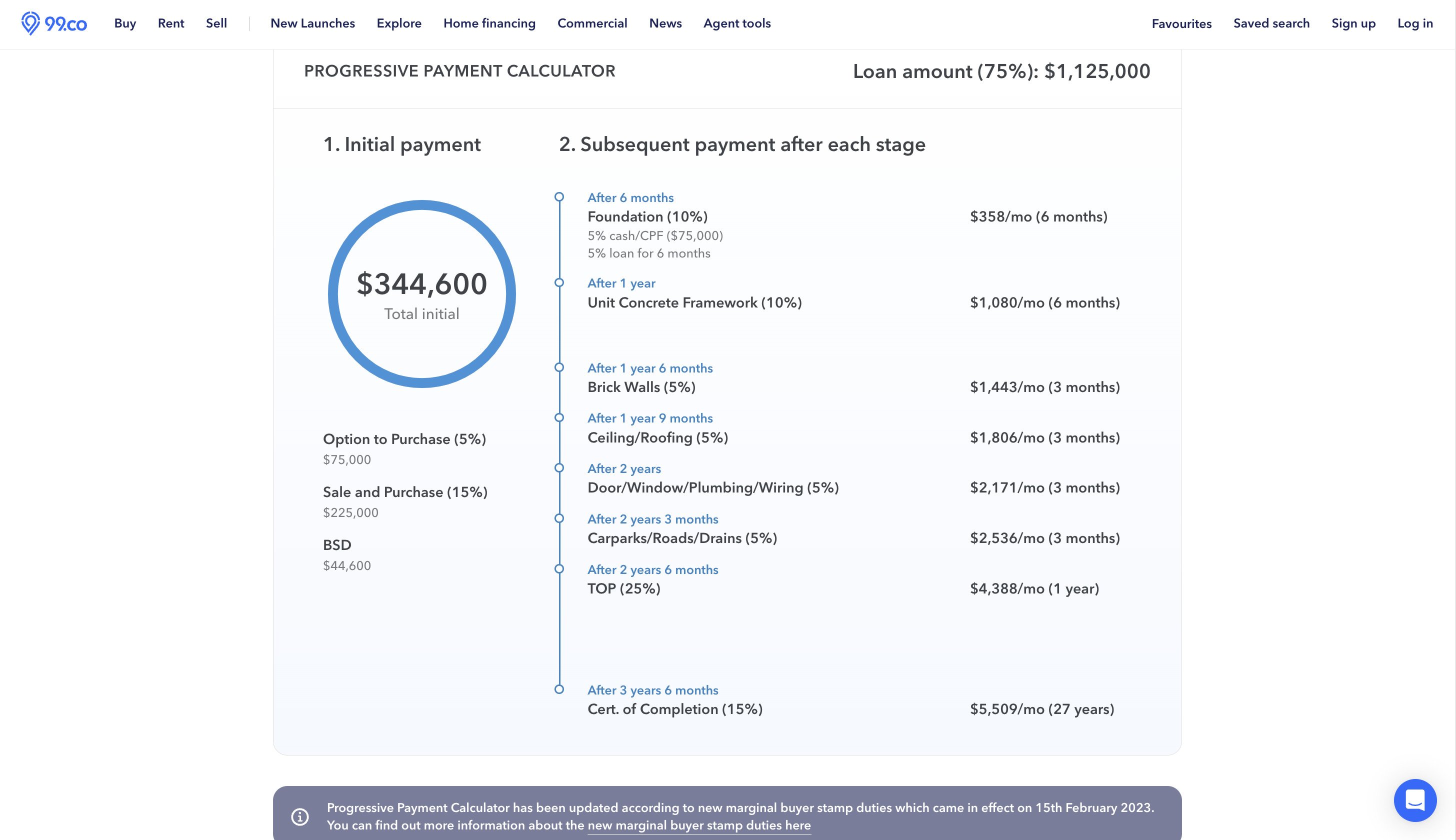

To get a breakdown of how much the couple would pay per month with the progressive payment scheme, we filled in the following details on 99.co’s progressive payment scheme calculator. We assume the home loan is on a 30-year tenure and an interest rate of 4% per annum.

Here’s how much the couple would pay per month as the condo gets built.

You can also use 99.co’s progressive payment calculator to do the math for you!

New launch condos for sale

Condo payment schedule for completed developments

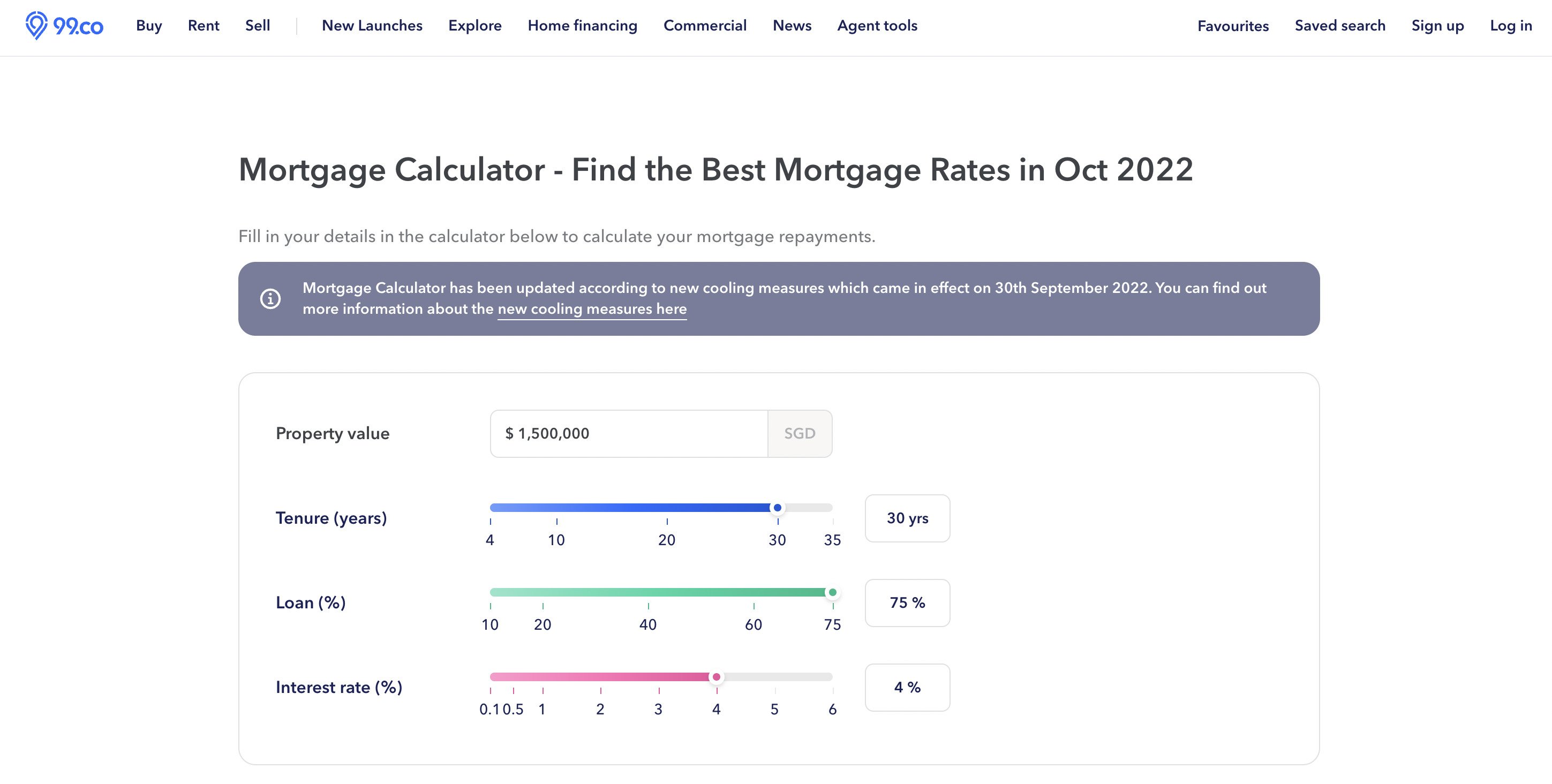

Now let’s see how the finances work out if Eddie and Alexandra decide to buy a completed development (i.e. a resale condo) instead.

| Fee payable/stage of work | Approximate timeframe | % of purchase price | Amount payable | Payment mode |

| Grant of option (Booking fee) | 1% | S$15,000 | Cash | |

| Exercise of option (Option fee) | Within 14 days of grant of option | 4% | S$60,000 | Cash |

| Buyer’s Stamp Duty (BSD) | Within 14 days of exercising the option | 1% of first S$180,000 | S$44,600 | Cash/CPF |

| 2% of next S$180,000 | ||||

| 3% of the next S$640,000 | ||||

| 4% of the next S$500,000 | ||||

| Legal fees | ~S$2,500 – S$4,000 | S$3,500 | Cash/CPF | |

| Valuation fee | ~S$350 – S$500 | S$350 | Cash/CPF | |

| Legal completion of sale and purchase at lawyer’s office | ~ 8 – 12 weeks of exercise of option | 95% (balance of purchase price) | S$1,425,000 | Cash and/or bank loan |

| Total | S$1,548,450 |

Again, the S$75,000 in booking and option fees must be paid completely in cash; CPF funds and bank loans cannot be used.

What is the monthly instalment for a resale condo?

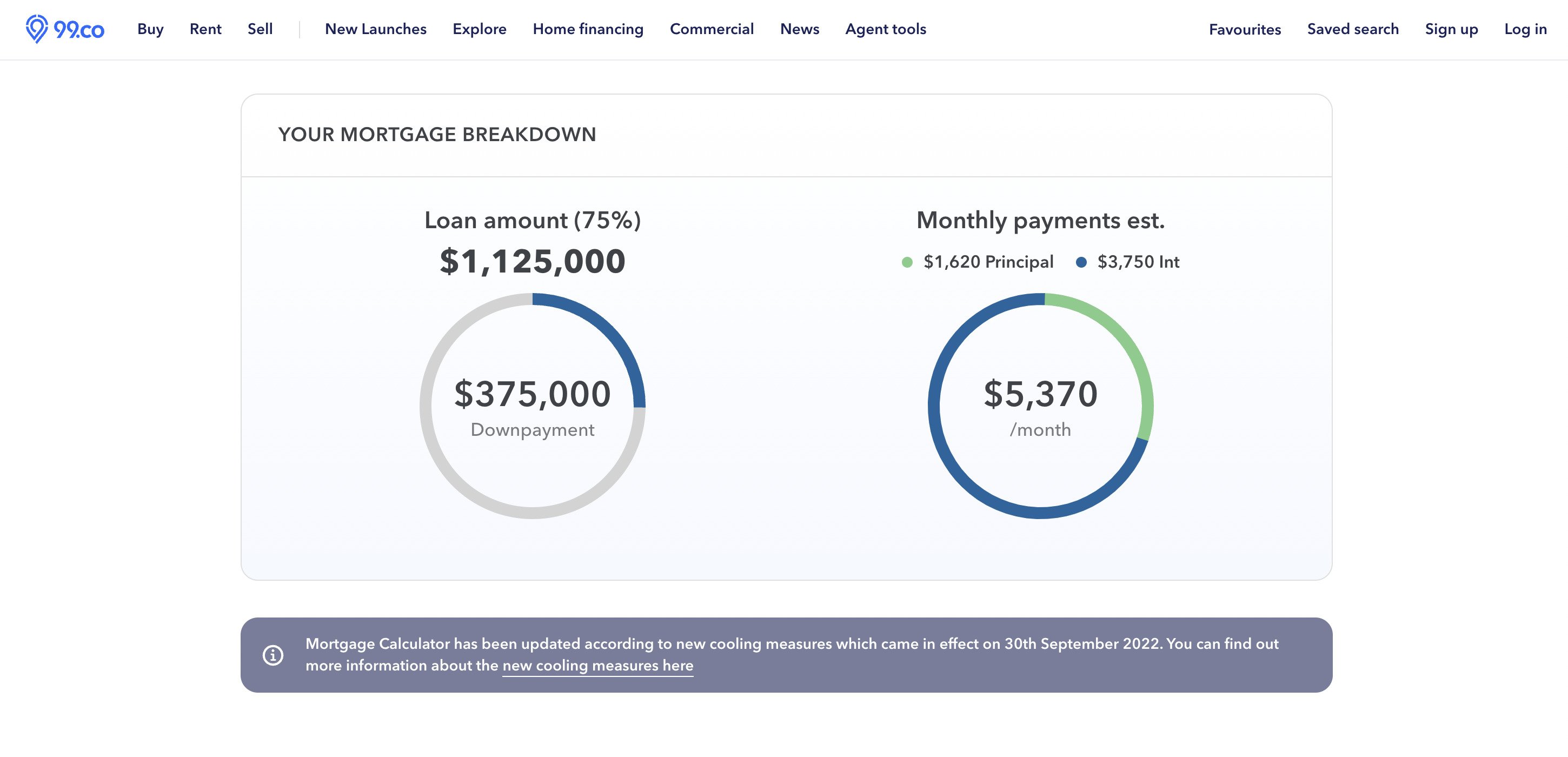

Likewise, assuming the couple would take a 30-year home loan at an interest rate of 4% per annum, here’s how much they will have to pay for the monthly instalments. This is calculated using 99.co’s mortgage calculator.

Resale condos for sale

Other costs and fees related to buying a condo

One cost will be renovation costs, depending on how extensive the renovation will be.

Plus, there is the condo maintenance fee, which you will have to pay every three months. The fee varies by condo, but it can range from S$250 to S$1,000 a month.

Also, don’t forget about the property tax, which is based on the annual value of a property. The annual value of a condo unit is higher than an HDB flat.

Detailed financing options for condo purchases

When purchasing a condominium, whether it’s completed or under construction, buyers typically rely on a combination of cash savings, CPF (Central Provident Fund), and bank loans to finance their purchase. Here’s a breakdown of the various financing options available:

1. Cash payments

Cash payments involve using your own liquid funds to cover part or all of the condo purchase price. This is the simplest form of payment, and it doesn’t require any third-party involvement.

When to use: Many buyers may choose to pay with cash for the booking fee, exercise fee, and even stamp duty, as well as part of the down payment. Cash payments can also be used for the final balance of the condo after progressive payments have been made.

Pros:

-

- No interest charges or loan repayments.

- Greater flexibility and fewer financial obligations post-purchase.

- Potential to negotiate better terms with sellers or developers since no loan approval is involved.

Cons:

-

- Large cash outlay, which could deplete savings.

- Not ideal for buyers who want to keep a substantial cash reserve for other investments or expenses.

2. CPF (Central Provident Fund)

CPF is a mandatory savings scheme for Singaporeans and Permanent Residents (PRs), which can be used for property purchases. Buyers can use their CPF Ordinary Account (OA) to pay for various costs related to purchasing a condo, such as the booking fee, stamp duty, progressive payments, and even the mortgage (if eligible).

Eligibility: Only Singapore citizens and Permanent Residents (PRs) can use their CPF savings for property purchases. There are also limits on how much CPF can be used, which vary depending on factors such as the property price and the amount of CPF savings in your account.

How it works: The CPF Ordinary Account can be used for the purchase of the condo’s booking fee and stamp duty, as well as progressive payments based on construction milestones. Buyers can also use CPF to finance the mortgage. However, the amount used must not exceed the purchase price or the market value of the property, whichever is lower.

Pros:

-

- Uses funds that you’ve already saved, meaning you don’t need to spend additional money from other savings or get a loan.

- Lower upfront out-of-pocket costs.

- It reduces the amount you need to borrow from a bank (if using a loan).

Cons:

-

- Once CPF is used for the condo purchase, it will need to be repaid with interest when the buyer sells the property, and the repayment will affect future withdrawals from your CPF.

- There is a limit to the amount you can use, and once you use CPF for the purchase, your CPF balance will be reduced, which could impact retirement savings.

3. Bank loans

Bank loans are one of the most common ways to finance the purchase of a condo, especially for buyers who need to borrow a significant amount. The loan is usually secured against the property, meaning the property itself serves as collateral.

How it works: The loan amount is typically based on a percentage of the condo’s value or purchase price, whichever is lower. The repayment is spread over a period of time, generally between 25 to 35 years, and includes both principal (the amount borrowed) and interest (the cost of borrowing the money).

Types of bank loans:

- Fixed-rate loan: The interest rate remains constant for a specified period, typically 3 to 5 years. After that, the rate may change based on market conditions.

- Floating-rate loan: The interest rate is tied to a reference rate, such as the Singapore Interbank Offered Rate (SIBOR), and fluctuates according to market conditions.

- Combination loan: This is a hybrid loan that allows borrowers to mix both fixed and floating rates for different portions of the loan.

Eligibility criteria: To qualify for a bank loan, you will need to meet certain eligibility requirements set by the lender, such as:

- Minimum income requirements.

- Credit history check.

- Debt servicing ratio (DSR), which measures the proportion of your income that goes toward debt repayment.

Loan-to-value (LTV) ratio: For a first mortgage, the LTV ratio is typically capped at 75% for properties costing up to $1 million, and 60% for properties above $1 million. This means you must provide a down payment of at least 25% (for properties under $1 million) or 40% (for properties above $1 million).

Pros:

-

- Allows buyers to purchase a condo without having to pay the full price upfront.

- Spreads payments over an extended period, making monthly payments more manageable.

- Offers flexibility with a choice between fixed and floating rates.

Cons:

-

- Interest charges over time, which can increase the overall cost of the property.

- Monthly loan repayments can be a financial burden for some buyers, especially if interest rates rise or if there is a change in income.

- The approval process may take time and involves a thorough review of your financial history and capability to repay the loan.

4. Other financing options: HDB loans & Government grants (for specific buyers)

For those buying Executive Condominiums (ECs) or certain types of public housing, government loans and grants may be available:

- HDB loan: For Singaporean citizens buying an EC, you may qualify for an HDB loan, which offers lower interest rates compared to bank loans.

- Government grants: First-time homebuyers may be eligible for grants such as the Additional CPF Housing Grant (AHG) or Proximity Housing Grant (PHG). These grants can help reduce the amount you need to borrow and can be used in conjunction with CPF savings and bank loans.

How to choose the right financing option

When choosing your financing option, it’s important to consider your financial situation, loan eligibility, and long-term goals. Here are some tips:

- Assess your financial health: Review your monthly income, existing debts, and credit score to determine which loan options you can qualify for. Make sure the monthly repayments are within your budget.

- Evaluate your loan options: Compare interest rates for different loan types (fixed vs. floating) and ensure you understand the repayment structure.

- Consider CPF usage: If you are a Singapore citizen or PR, using CPF for your condo purchase can help reduce your out-of-pocket payments, but remember that it will affect your future CPF balance.

- Consult a mortgage broker or financial advisor: A mortgage advisor can help you navigate through different loan packages, help you determine the best financing structure, and guide you through the entire process.

By exploring these financing options, buyers can make an informed decision on how best to fund their condo purchase, balancing their upfront costs and long-term financial commitments.

Thinking of selling your house to move to a new launch or resale condo? Let us help you with the process by connecting you with a premier property consultant.

If you found this article helpful, 99.co recommends Should Singapore adopt the Danish Mortgage Model? and Full list of new launch condos (with unsold units) approaching their developer ABSD deadlines in 2023/2024.

[Additional reporting by Virginia Tanggono]

Frequently Asked Questions (FAQs)

What is the condo payment schedule for new launch developments in Singapore?

The condo payment schedule for new launch developments involves several stages of payments, including exercising the option, signing the Sale and Purchase agreement, paying the Buyer’s Stamp Duty, downpayment, legal fees, valuation fee, and progressive payments based on the construction progress.

How is the condo payment schedule structured for completed developments (resale condos) in Singapore?

The condo payment schedule for resale condos typically includes stages such as the grant of option, exercise of option, Buyer’s Stamp Duty, legal fees, valuation fee, and final completion of the sale and purchase transaction at the lawyer’s office.

How much is the down payment for a condo?

Generally, if you take the full 75% financing from the bank loan, the downpayment will be 25%. 5% must be paid in cash, while the remaining 20% can be paid in cash and/or CPF.

How does the progressive payment scheme work?

The progressive payment scheme allows you to pay according to the different stages of the construction. For instance, after the foundation work is done, you’ll have to pay 10% of the purchase price within 14 days.

Can you use CPF to pay for a condo?

You can use your CPF Ordinary Account savings to pay for your condo. This includes the downpayment, stamp duty, and home loan instalments. Depending on the law firm, you may also be able to pay the legal fees with your CPF.

What happens if I am unable to make my monthly instalments on time?

If you cannot make your monthly payments on time, contacting your bank or financial institution is crucial. Delayed payments can result in late fees and negatively impact your credit score. Discussing your situation with the lender may lead to temporary relief options or loan restructuring.

What is the typical tenure of a condo loan, and are there options for early repayment?

Condo loans typically have tenures ranging from 25 to 30 years. Most loans offer options for early repayment, either through lump-sum payments or increased monthly instalments. However, terms and conditions might be associated with early repayment, so it’s advisable to consult your lender for details.

What are the monthly instalment amounts for the new launch and resale of condos in Singapore?

The monthly instalment amounts for condos depend on loan tenure, interest rate, and loan amount. Tools like 99.co’s progressive payment scheme calculator and mortgage calculator can help estimate these amounts based on individual preferences and financial situations.

What additional costs and fees are associated with buying a condo in Singapore?

In addition to the purchase price and associated fees, buyers should consider renovation costs, condo maintenance fees payable every three months, and property tax based on the annual value of the property. These additional costs can vary depending on the extent of renovation and the specific condo development.

About Sophiyanah David

Sophi, a seasoned copywriter specialising in Singaporean real estate and property, is one of the minds behind 99.co's informative articles. Like her colleagues at 99.co, Sophi is dedicated to keeping you informed about the ever-changing world of real estate so you can find your forever home. When off the clock, you can find her giggling and kicking her feet as she reads her romance novels, watching anime - if FMBA is not your fave, she might fight you (but you'll probably win) and looking up latest skincare trends.

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter