BTO-ing is more than just paying a S$10 fee for your desired project, crossing your fingers and hoping for the best. If it’s your first foray into the property market, your HDB BTO application would be the start of a learning curve. There’s a lot of technical jargon to wrap your head around, from PLH, HFE to MSR.

Not to worry, though, here’s a crash course to make your BTO journey a smoother one!

Ethnic Integration Policy (EIP)

Commonly referred to as the “racial quota”, the Ethnic Integration Policy (EIP) was introduced in 1989 as the government’s way of ensuring that races don’t become segregated in our public housing estates. This might happen if, say, Tampines becomes a mecca for Muslim food.

So the Housing & Development Board (HDB) has in place a racial quota. The quota specifies the maximum number of units in any given HDB block that can be occupied by a certain race. A block with 100 units might have a racial quota of 76 Chinese, 19 Malay and 15 Indian/Others. Note that the number (110) is greater than the units available, which indicates a bit of leeway in the mix of races for each block.

Racial quota is strictly enforced, and affects BTO applicants during the flat selection process. For example, if your queue number is within the flat supply of your project, but the racial quota for your race has been filled before it’s your turn to choose your flat, your flat selection appointment with HDB will be cancelled immediately.

So even if there are empty flats in a particular block, you may not get to book a flat if the quota for your ethnicity has been reached.

Rest assured that this voided HDB BTO application will not be counted as a rejection on your part.

HDB BTO application balloting system

What’s this queue number thing, you may ask? HDB manages its application process through a computerised balloting system that randomly assigns applicants with a queue number. The applicants are then invited to select a flat in the order of the queue number.

As HDB issues queue numbers beyond the flat supply available to account for dropouts during the flat selection process, there are two situations to take note of:

- Your queue number is within the flat supply for your project. Congratulations! You’re assured of a flat if the racial quota for your race has not been filled. The lower your queue number, the greater the choice of units.

- Your queue number exceeds the flat supply for your project. To get the chance to pick a flat, you’ll have to count on there being enough dropouts. The racial quota still applies.

HDB gives priority to first-time applicants and applicants under certain priority schemes, offering them additional chances to score a low queue number in the balloting process. For instance, a first-timer couple applicant would receive two chances on the ballot compared to one for second-timers.

By the way, most BTO flats released are also reserved for first-timers. Here are the exact percentages, which differ for mature and non-mature estates.

Non-mature estates

3-room: First-timer applicants are allocated at least 85% of the flat supply, up from 70%. On the other hand, second-timer applicants are allocated the remaining 15%, down from 30%.

4-/ 5-room/ 3Gen: First-timer applicants are allocated at least 95% of the flat supply, up from 85%. In comparison, second-timer applicants are allocated the remaining 5%, down from 15%.

For BTO projects with shorter waiting time

4-/ 5-room/ 3Gen: First-timer applicants are allocated 95% of the flat supply, while second-timer applicants are allocated the remaining 5%.

If there’s a mix of BTO projects with normal and shorter waiting times in the same estate, the quota for 4-room and bigger flats will be computed based on the weighted average of the projects offered.

Mature estates

3- to 5-room: First-timer applicants are allocated at least 95% of the flat supply, while the remaining 5% is allocated to second-timer applicants.

Note that for both non-mature and mature estates, some flats are also set aside for quota-based priority schemes where HDB does not differentiate between first-timers and second-timers. One such scheme is the Third Child Priority Scheme.

So if there are fewer first-timers than the number of flats set aside for them, the excess flats will be allocated to second-timers. And regardless of priority schemes and applicant status (first-timer or second-timer), the selection queue positions of all shortlisted applicants are randomly balloted.

If you’re successful in the ballot and invited to apply for a flat (yay!), you might want to think twice before rejecting your invitation. There are consequences for not following through with an HDB BTO application.

For first-timer families, rejecting two chances to select a flat means your first-timer priority gets suspended for one year. If you reject two more chances to select a flat in that year, the suspension will be extended for another year.

For single first-timer applicants and second-timer families, the penalties of rejecting two chances to book a flat will result in a harsh one-year ban from participating in future BTO flat launches!

Read this: 5 scenarios that can disqualify you from getting HDB BTO first-timer applicant benefits.

Prime Location Public Housing (PLH) Model

The PLH model, introduced by HDB in October 2021, aims to curb the lottery effect of BTO flats by applying stricter conditions to new BTO flats in prime and central locations, such as the city centre and the Greater Southern Waterfront (GSW). These flats are priced with additional subsidies beyond the standard BTO assistance, making them more affordable despite their desirable locations.

However, to purchase a new PLH flat, buyers must meet more stringent eligibility criteria, including a stricter income ceiling currently set at S$14,000, and must be a Singaporean household with at least one Singapore Citizen (SC) and one Singapore Permanent Resident (SPR). The household must also have an eligible family nucleus, such as a married couple, and must not own or have any interest in private property, nor have disposed of any within the last 30 months.

The model also mandates a 10-year Minimum Occupation Period (MOP) instead of the usual five years, during which owners are prohibited from renting out the entire flat, even after fulfilling the MOP – only spare rooms may be rented out. Additionally, when the flat is resold on the secondary market, a portion of the resale price or valuation, whichever is higher, will be recovered by HDB to reclaim the extra subsidies provided.

These measures are designed to ensure that public housing remains affordable, accessible, and inclusive.

Sale of Balance Flats (SBF)

Sale of Balance Flats (SBF) launches allow prospective homebuyers to apply for

- balance flats from previous BTO sales launches,

- surplus Selective En bloc Redevelopment Scheme (SERS) replacement flats, and

- re-purchased flats

SBF sale exercises are also conducted through a balloting system similar to the one used for BTOs.

SBF sales exercises coincide with BTO launches in May and November, and applicants can only apply for one or the other, not both.

HDB Flat Eligibility (HFE) letter

The HDB Flat Eligibility (HFE) letter is crucial as it informs you of your eligibility to buy a new BTO or resale flat, receive CPF grants along with the respective amounts, and obtain an HDB housing loan, including the loan amount. For second-time buyers, HDB will also notify you of any resale levy payable if you’re purchasing a second subsidised flat.

You need to apply for the HFE letter at specific stages: if you’re buying a new flat, you must have a valid HFE letter when you apply for the flat from HDB. If you’re buying a resale flat, you need the HFE letter before obtaining an Option to Purchase (OTP) from the seller and submitting your resale application to HDB.

HDB anticipates longer processing times for the HFE letter during sales launch months (February, May, August, and November for BTO). Since the introduction of the HFE letter, some have reported longer waiting times, so it’s advisable to apply as soon as you decide to buy an HDB flat, whether BTO or resale, to avoid delays.

To ensure a smooth home-buying experience, it’s important to stay proactive and well-prepared when applying for the HFE letter. Apply early to avoid delays and keep your financial documents and personal information up-to-date, as these are necessary for the application process!

Read this: What is the HDB Flat Eligibility (HFE) letter and how to apply in 2024

Approval-in-Principle (AIP)

You will need an AIP if you intend to take a housing loan from a local bank. Sometimes, it’s called In-Principle Approval (IPA).

An AIP guarantees the bank that it will loan you an agreed sum of money, taking into account your income, debt servicing ratios and financial health. It doesn’t mean that you’ve secured the housing loan when the AIP is issued; the purpose is to help you determine what kind of home you can afford.

An AIP is usually valid for 30 days, depending on the bank’s policy.

Loan-to-Value (LTV) ratio

The LTV ratio of a property reflects the size of a home loan in proportion to its actual valuation.

Let’s say your home is worth S$500,000, and you’ve taken out a S$300,000 loan to finance its purchase. Your LTV would be 60% (S$300,000/S$500,000 x 100%).

Banks will usually be willing to loan up to 75% of the property’s value if it’s your first loan. The maximum LTV ratio that a bank is allowed to loan decreases by the number of existing housing loans a borrower has. For instance, if the borrower has another housing loan, the LTV for the second housing loan will be 45%.

Currently, the LTV for bank loans and HDB loans are both at 75%.

Total Debt Servicing Ratio (TDSR)

TDSR is a computation of a person’s total monthly debt obligations (such as car loans), as a percentage of their total monthly income.

Under the current rules, a borrower can only use 55% of their monthly income to pay off any monthly debt obligations, including home loans.

You can use 99.co’s TDSR calculator for easy calculations.

But in the case of HDB flats, the ratio to take note of is the MSR.

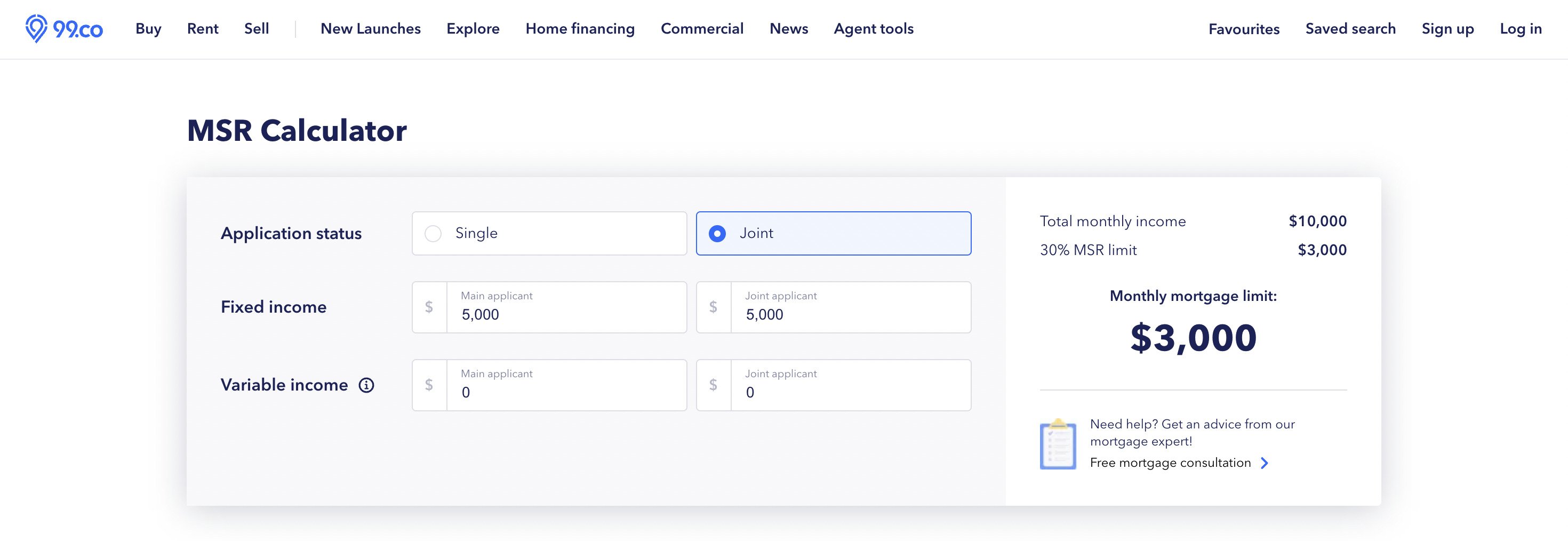

Mortgage Servicing Ratio (MSR)

MSR is a computation of a person’s monthly mortgage repayments as a percentage of their total monthly income.

Under the current rules, if the borrower is purchasing an HDB flat or Executive Condominium (EC) and taking a home loan, the MSR cannot exceed 30%.

You can use 99.co’s MSR calculator for easy calculations.

Option Fee

When you book a flat during the flat selection appointment at HDB, you’ll have to pay the option fee. The amount depends on the flat type you’re buying.

- 2-room Flexi: S$500

- 3-room: S$1,000

- 4-room and bigger: S$2,000

The option fee works as part of the downpayment for the flat. If you decide not to go through with the purchase, for instance, cancel your BTO application after booking the flat, your option fee will be forfeited.

Downpayment (for HDB BTO application)

The downpayment is the portion of the purchase price a buyer has to pay in cash or CPF. It cannot be paid as part of your home loan.

The minimum downpayment required depends on whether you’re taking an HDB loan or a bank loan.

For example, with a bank loan, the minimum downpayment is 25% (minimum 5% in cash, with the remainder with CPF and/or cash). On the other hand, for an HDB loan, the minimum downpayment is 20% (payable in cash and/or CPF).

Calculate your mortgage repayments with 99.co’s mortgage calculator.

Buyers eligible for the Staggered Downpayment Scheme can split their downpayment obligations over two payments (instead of one). The two payments occur at the second appointment (to sign the Agreement for Lease) and during key collection.

Stamp duty

Stamp duty is a lump sum of tax payable for purchasing or selling a property. The exact amount varies according to the price or value of the property, whichever is higher.

A Buyer’s Stamp Duty (BSD) must be paid for any property purchase, including a BTO flat. However, for BTO flats, the stamp duty will be based on the selling price.

|

Purchase price or market value of the property |

Stamp duty rates |

|

First S$180,000 |

1% |

|

Next S$180,000 |

2% |

|

Next S$640,000 |

3% |

|

Next S$500,000 |

4% |

|

Next S$1,500,000 |

5% |

|

Remaining amount |

6% |

If like me, math makes your head hurt, use 99.co’s stamp duty calculator to do some of the heavy lifting!

Conveyancing or legal fees

Conveyancing fees are the legal costs charged by HDB for preparing the paperwork for sale, and for the housing loan if you’re taking an HDB loan.

The conveyancing fees are calculated as follows:

| Purchase price of the property | Rates |

| First S$30,000 | S$0.90 per S$1,000 |

| Next S$30,000 | S$0.72 per S$1,000 |

| Remaining amount | S$0.60 per S$1,000 |

If you’re going with a bank loan, you would need to hire external lawyers to act for you in the purchase (your bank will help you with this). Instead of paying the conveyancing fees above, you’d just need to pay your solicitors their legal fees, which is, on average, about S$2,500 for a BTO purchase.

Read this: Everything you need to know about the HDB BTO payment timeline.

Estimated Completion Date (ECD)

The Estimated Completion Date (ECD) is the day the contractors finish construction of the property and surrender it to HDB.

HDB will usually provide buyers with an ECD, but the actual completion date of the property is typically about six to nine months earlier than what’s predicted. (As we’ve seen for the past two years, this is barring any disruptions that may lead to construction delays, such as labour shortages and supply chain issues caused by the pandemic.)

Delivery Possession Date

The delivery possession date is the date by which HDB is required under the Agreement for the Lease to deliver the keys and legal possession of the flats to the homeowners.

HDB Fire insurance

If you’re taking an HDB loan, you must take out a fire insurance policy with FWD, HDB’s appointed insurance agent. The insurance cost varies according to the flat type, and their rates can be found via HDB’s portal here.

Home Protection Scheme (HPS)

HPS is a mortgage-reducing insurance scheme offered by the CPF Board. It’s meant to pay out any outstanding home loan amount should the insured person suffer from a permanent disability or pass away before repaying the loan.

Coverage under HPS is required only where a buyer intends to use their CPF to service the monthly instalments on their home. The premium is paid annually using the buyer’s CPF savings or cash. The amount payable varies depending on factors such as your declared percentage of coverage, loan amount, age and gender.

Check out the CPF Board’s HPS Premium Calculator to get an estimate on the premium you’d have to pay.

Key collection

As the name suggests, the collection of keys refers to the appointment with HDB, where you finally collect the keys to your new home!

You will be required to bring originals of the following documents of everyone listed in the HDB BTO application:

- Identity cards

- Certificate of fire insurance

- Completed GIRO form (if you’re paying monthly loan instalments partially or fully in cash)

- Power of Attorney if you’re unable to attend the appointment personally (if you‘re overseas, the attorney representing you must bring one certified true copy by the solicitors and two photocopies)

With that, we wish you a smooth BTO journey!

Do you have any questions about other HDB BTO terms? Let us know in the comments section below!

If you found this article helpful, 99.co recommends BTO or resale HDB flat: First-timer dilemma and 99.co’s guides: BTO Application Process.

Frequently Asked Questions

How does the HDB BTO application balloting system work?

HDB manages its application process through a computerised balloting system randomly assigning applicants with a queue number. The applicants are then invited to select a flat according to the queue number received.

Commonly referred to as the “racial quota”, the Ethnic Integration Policy (EIP) is the government’s way of ensuring that race enclaves don’t develop in our public housing estates, leading to segregation.

An AIP guarantees the bank that it will loan you an agreed sum of money, taking into account your income, debt servicing ratios and financial health.

About 99.co

We are a property search engine with the overarching goal of building a more transparent and efficient property market. We are working towards that future by empowering people with the tools and information needed to find a place to live in the best way possible.

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

1. How does Govt grants come into this loan amount picture?

2. Setting asides CPF, Govt grants and Bank loan from HDB or pte Bank what proof of payment or document is needed to make up the balance amount needed? E.g. parents helping their kids to pay.