Thinking of upgrading from an HDB flat, but find that buying a condo is too expensive? Your best bet is to get an Executive Condo.

A hybrid of public and private housing, Executive Condominiums (EC) come with condo facilities, but are cheaper than condos as they’re subsidised. Just like HDB flats, you can take CPF Housing Grants to buy a new EC.

And the best part about getting a new Executive Condo? You don’t have to pay the Additional Buyer’s Stamp Duty (ABSD) upfront when you’re upgrading. The caveat is that you have to sell your flat within six months.

After 10 years, the EC becomes fully privatised like condos, allowing you to sell it to foreigners. However, under the latest policy revisions announced on 8 May 2026, upcoming ECs starting from the sites released under the 1H2026 GLS Programme will only achieve full privatisation after 15 years.

Since they’re considered public housing, new ECs have a few restrictions similar to HDB flats. This includes the Minimum Occupation Period (MOP), income ceiling of S$16,000, and Mortgage Servicing Ratio (MSR).

MSR restricts the monthly loan amount you can take for an HDB flat or a new EC. So you can only use up to 30% of your monthly income for your home loan.

At the same time, you can only take up a bank loan to pay for an EC, meaning you can only get 75% financing. So what’s the minimum income to afford an EC?

The estimated minimum monthly income you need to buy a new Executive Condo

You can calculate this by working backwards. Based on the price of the EC, you can find the maximum loan amount you can get. After that, calculate the monthly instalments using 99.co’s mortgage calculator to derive the minimum income you need to buy an EC.

For illustration purposes, we’ll use the average price of a three-bedroom EC unit, derived from three-bedroom unit transactions for new launch ECs in the first five months (up to 21 May) of 2023. These ECs include:

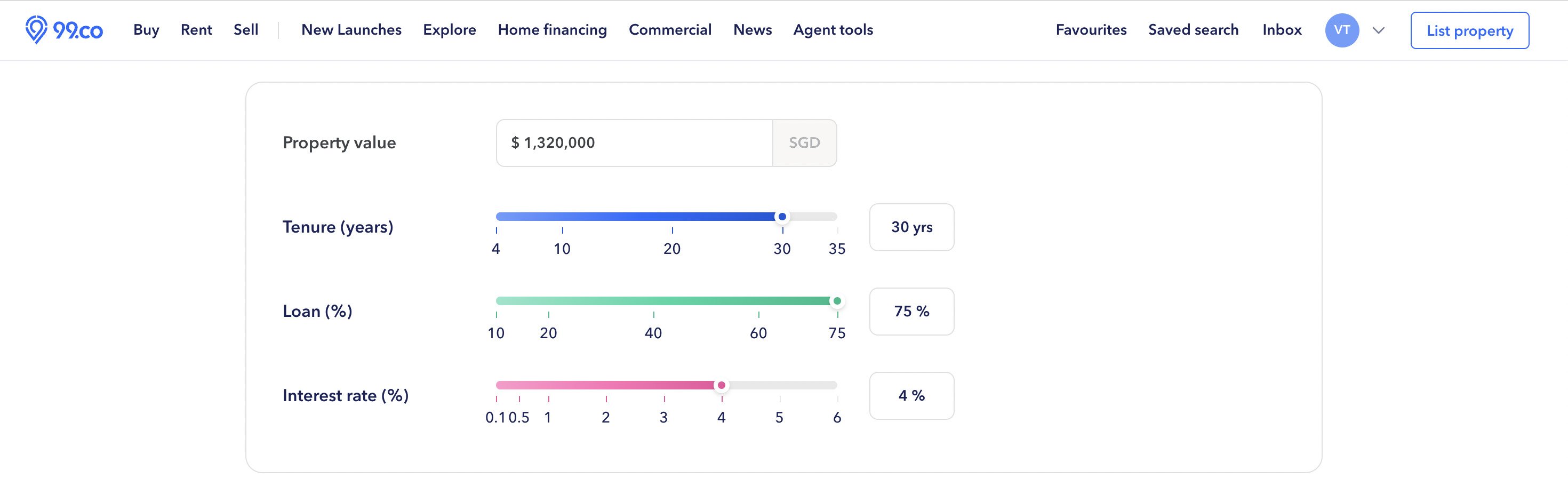

Estimates are based on the following assumptions:

- The full 75% financing is taken to maximise the loan-to-value (LTV) ratio

- The loan comes with a 30-year tenure

- A medium-term interest rate of 4%, in light of the September 2022 cooling measures, is applied to compute the 30% MSR and minimum gross monthly income needed

- There are no other housing loans to be paid

- CPF grants and savings are not taken into account

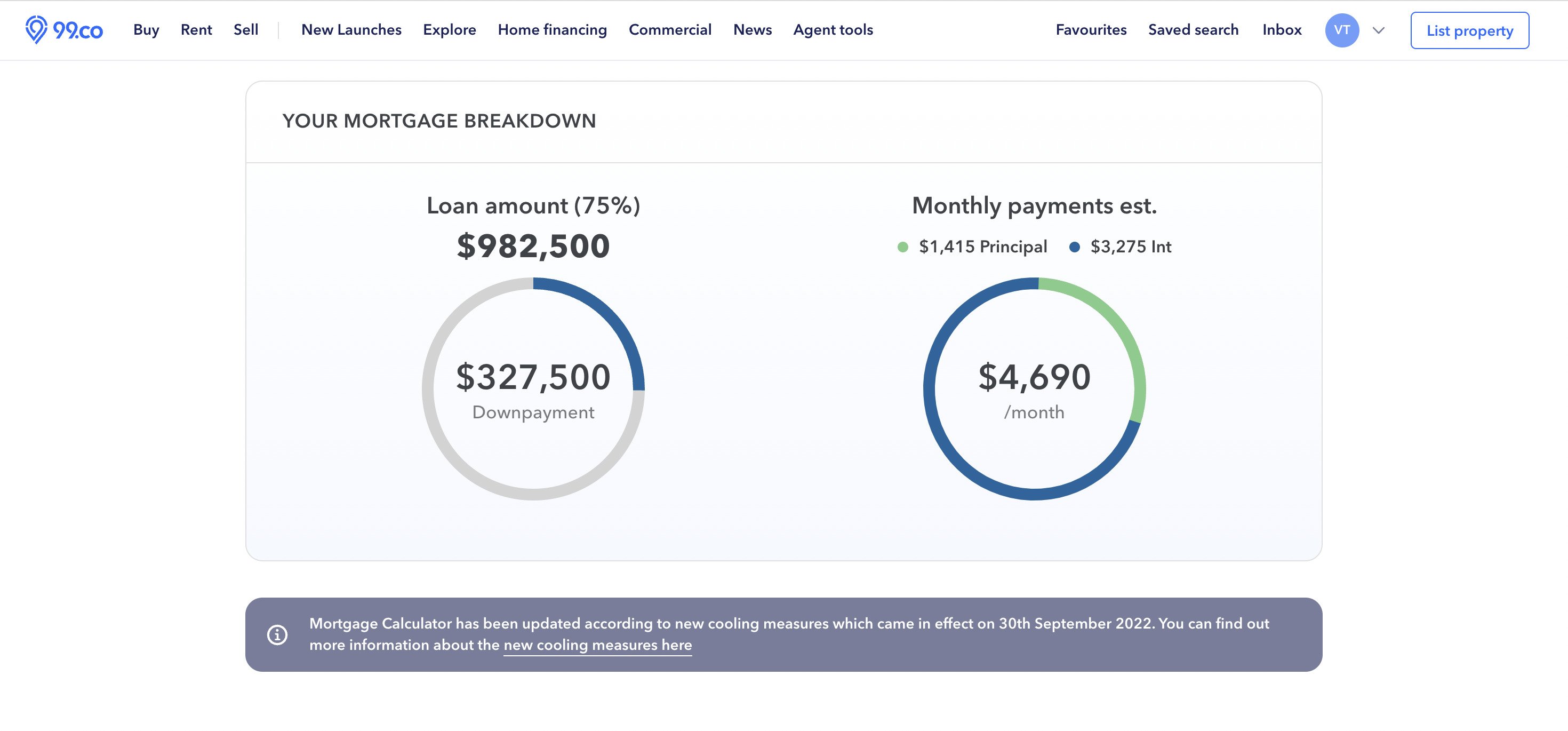

| Average price of a 3-bedroom new launch EC | Loan amount (75%) | Downpayment (25%) | Estimated monthly instalment (with 4% interest rate) | Estimated monthly household income to meet 30% MSR |

| S$1.31 million* | S$982,500 | S$327,500 | S$4,690 | S$15,633 |

*based on 99.co’s Researcher.

Disclaimer: Do note that these estimations are based on the average price, which may be higher or lower than the actual price of the EC. We recommend that you calculate based on the actual price to determine if it’s within your means.

Get in touch with 99.co’s mortgage broker to get the best rates!

(Curious about how much you need to earn to buy other types of properties? We’ve crunched the numbers on the estimated monthly income to afford an HDB resale flat or a condo.)

How about resale ECs?

We consider resale Executive Condos as those that have passed the MOP and entered the resale market, but they haven’t fully privatised yet. As mentioned earlier, these units can only be sold to Singaporeans and PRs, like resale HDB flats.

But unlike new ECs, resale ECs don’t have as many restrictions, such as the MOP and having to dispose of your existing flat. Find out more about the differences between new and resale ECs here.

More importantly, you’re not subjected to the 30% MSR requirement. Instead, you’ll have to meet the total debt servicing ratio (TDSR), which limits the total amount of loans you can service in a month. As of 16 December 2021, the TDSR is capped at 55%. So compared to the MSR, it gives you more affordability to buy a resale EC.

The estimated minimum monthly income you need to buy a resale Executive Condo

We calculate it the same way as the new launch EC, but based on the transactions of three-bedroom resale ECs in the first five months (up to 21 May) of 2023. So this would include ECs that have TOPed from 2014 to 2018, such as:

- 1 Canberra

- Arc At Tampines

- Austville Residences

- Bellewaters

- Bellewoods

- Belysa

- Blossom Residences

- Citylife @ Tampines

- Ecopolitan

- Forestville

- Heron Bay

- Lake Life

- Lush Acres

- Riverparc Residence

- Sea Horizon

- Skypark Residences

- The Amore

- The Canopy

- The Rainforest

- The Tampines Trilliant

- The Topiary

- Twin Fountains

- Twin Waterfalls

- Waterbay

- Watercolours

- Waterwoods

Estimates are based on similar assumptions:

- The full 75% financing is taken to maximise the LTV ratio

- The loan comes with a 30-year tenure

- A medium-term interest rate of 4%, in light of the September 2022 cooling measures, is applied to compute the 55% TDSR and minimum gross monthly income needed

- For illustration purposes, there are no other loans to service, including property loans, car loans, personal loans and student loans

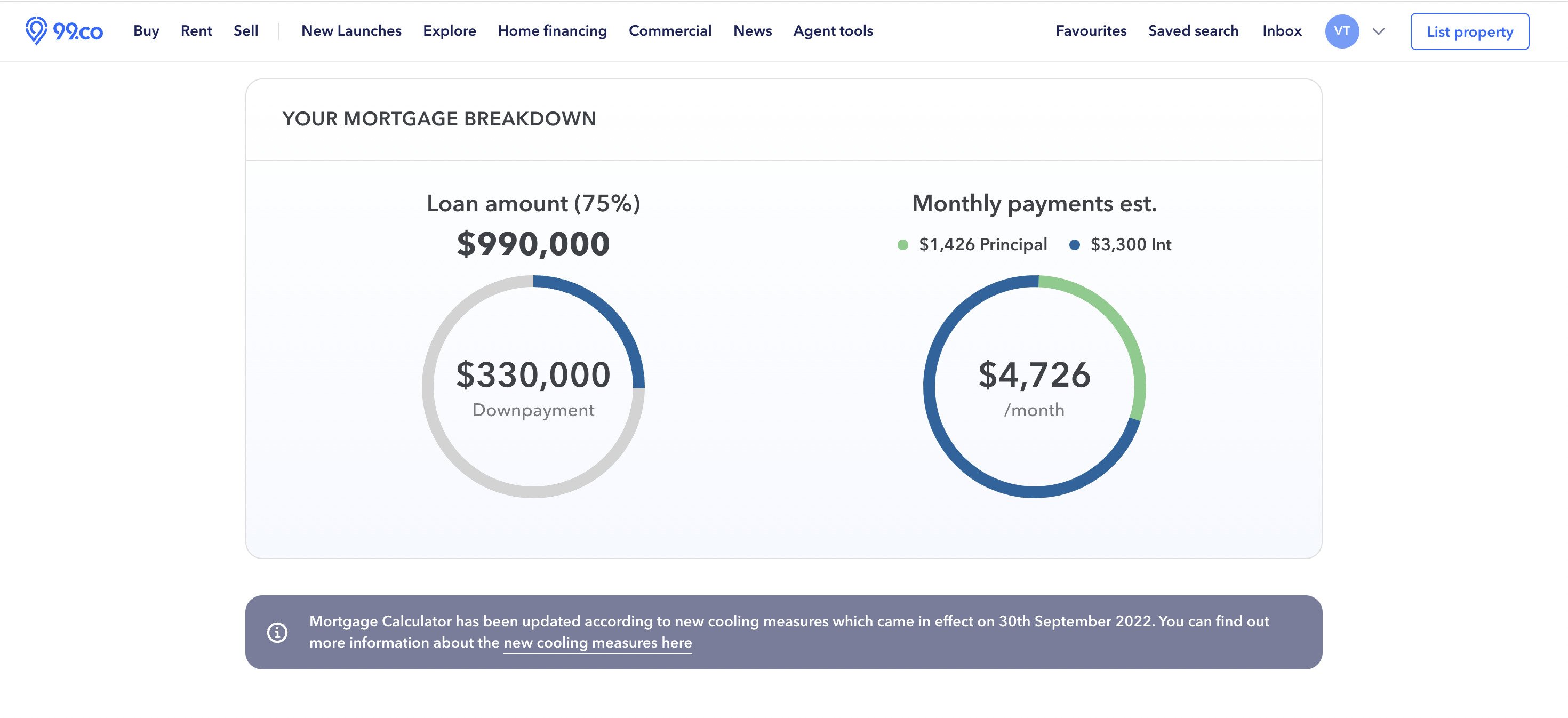

| Average price of a 3-bedroom resale EC | Loan amount (75%) | Downpayment (25%) | Estimated monthly instalment (with 4% interest rate) | Estimated monthly household income to meet 55% TDSR |

| S$1.32 million* | S$990,000 | S$330,000 | S$4,726 | S$8,593 |

*based on 99.co’s Researcher.

Disclaimer: Do note that these estimations are based on the average price, which may be higher or lower than the actual price of the EC. We recommend that you calculate based on the actual price to determine if it’s within your means.

Get in touch with 99.co’s mortgage broker to get the best rates!

Alternatively, you can find out more about how much loan you can get based on your monthly income using 99.co’s affordability calculator here.

Planning to sell your property to buy a new or resale EC? Let us help you get the right price by connecting you with a premier property agent.

If you find this article helpful, 99.co recommends Nearly all ECs resold in the past 15 years made a profit averaging S$300k and Resale ECs hitting MOP in 2023 (and should you sell right after MOP?).

Frequently asked questions

An EC is a public/private hybrid type of property, while a condo is private property. So a new EC tends to be cheaper, but comes with more restrictions such as a five-year Minimum Occupation Period (MOP) and an income ceiling of S$16,000. They’re also only sold to Singaporeans initially, with PRs being allowed to buy them after the MOP.

While Executive Condos are built by private developers and come with condo facilities, they’re considered public housing for the first 10 years. They’re considered private property after the 10th year mark.

Yes, under the Joint Singles Scheme. The scheme allows up to 4 single co-applicants to buy a new EC.

About Virginia Tanggono

Virginia covers the property news in Singapore, from record sales to profile stories on home ownership. In her free time, she occasionally searches for spoilers of movies and TV shows.

Looking to sell your property?

Whether your HDB apartment is reaching the end of its Minimum Occupation Period (MOP) or your condo has crossed its Seller Stamp Duty (SSD) window, it is always good to know how much you can potentially gain if you were to list and sell your property. Not only that, you’ll also need to know whether your gains would allow you to right-size to the dream home in the neighbourhood you and your family have been eyeing.

One easy way is to send us a request for a credible and trusted property consultant to reach out to you.

Alternatively, you can jump onto 99.co’s Property Value Tool to get an estimate for free.

If you’re looking for your dream home, be it as a first-time or seasoned homebuyer or seller – say, to upgrade or right-size – you will find it on Singapore’s fastest-growing property portal 99.co.

Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

Join our social media communities!

Facebook | Instagram | TikTok | Telegram | YouTube | Twitter

Leave a comment